By Gregory Mc Guire

We have all come to the understanding that Prime Minister Patrick Manning abhors gambling. But those familiar with Play Whe or its local predecessor Whe Whe , may wish to advise the Prime Minister that there are important lessons to learn from these games that may be useful in macro-economic policy formulation and management one is that you must learn to read the signs. In Play and Whe Whe , the gambler often hedges his bets.

While the dream or incident may imply that the mark is 13, the expert’s guidebook suggests that she places bets on 13, 31, and 4. In other words, look at all sides and diversifies the portfolio. As Government continues to trumpet the solid performance of the economy over the past five years, there is evidence to suggest that they may be reading the wrong signs and consequently the Prime Minister may be a bigger gambler than he wishes to admit.

While the dream or incident may imply that the mark is 13, the expert’s guidebook suggests that she places bets on 13, 31, and 4. In other words, look at all sides and diversifies the portfolio. As Government continues to trumpet the solid performance of the economy over the past five years, there is evidence to suggest that they may be reading the wrong signs and consequently the Prime Minister may be a bigger gambler than he wishes to admit.Two elements of the Government’s macro-economic management have become abundantly clear over the last month. First, only an accident can put the breaks on Government expenditure, as the incumbents push relentlessly forward towards the Vision 2020 goals. In both words and deed, the massage is clear, there are only 12 years left to 2020 and we must get the job done- inflation notwithstanding. Second, what the IMF defines as an exit strategy i.e. what will sustain this economy beyond oil and gas, is indeterminate at best. The big question is whether this strategy is sustainable?

One view is that the Government is so confident of its approach that the issue of an exit strategy does not arise. Such a view may be informed or misinformed by the popular notion that the economic fundamentals are strong and will endure. However, the success story told by the positive trends in macro-economic aggregates such as GDP, employment, and foreign exchange reserves is incomplete. In an economy such as ours, arguably the most important macro economic aggregate is the Balance of Payments. This is generally not an icon on the screen and therefore is hardly ever activated. Reading the signs in the Balance of Payments give a different picture of the economy and may suggest a reordering of macro-economic priorities.

The BOP is a record of all international transactions that are undertaken between residents of one country and the rest of the world over a specified period of time. So why is this so important? First , the BOP provides us with important information about whether or not this country is “paying its way” in the international economy. In other words do we earn enough money to pay for the good and services which we would like to have but which are not produced in T&T. Secondly, the BOP allows us to determine critically the sources and uses of foreign exchange. In other words how do we pay and on what do we spend. Both sets of information is critical to the formulation of macro-economic policy. In a country like T&T , the BOP is perhaps the best indicator of the extent of dependence of the economy on the hydrocarbon sector.

The BOP is a record of all international transactions that are undertaken between residents of one country and the rest of the world over a specified period of time. So why is this so important? First , the BOP provides us with important information about whether or not this country is “paying its way” in the international economy. In other words do we earn enough money to pay for the good and services which we would like to have but which are not produced in T&T. Secondly, the BOP allows us to determine critically the sources and uses of foreign exchange. In other words how do we pay and on what do we spend. Both sets of information is critical to the formulation of macro-economic policy. In a country like T&T , the BOP is perhaps the best indicator of the extent of dependence of the economy on the hydrocarbon sector.

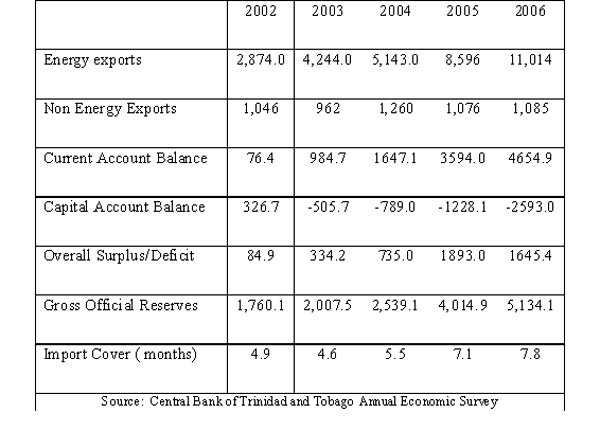

What are some of the key trends in the T&T Balance of Payments over the last five years? The Balance of Payments position of Trinidad and Tobago tell some interesting stories.( Table 1) First the good news. Led by increases in both prices and volume of energy sector exports, both Trade and Current Accounts have recorded positive and growing balances over the last five years. In contrast, the Current Account which records international financial transactions has recorded large and growing deficits since 2003.

Notwithstanding this the large current account surpluses has enabled T& T to generate overall surplus on the Balance of Payments and to build up its foreign exchange reserves. At the end of 2006, the reserves accumulated were sufficient for 7.8 months of imports. Bad news is often camouflaged by official statistics. Fortunately this is not the case here. Certain weaknesses are evident.

First, the energy sector now accounts for 90 % of total foreign exchange earnings. . What is worse is that non energy exports have declined in relative and absolute terms. Non energy exports peaked at US$ 1260 million in 2004 but has declined to US$1,085 .6 million in 2006. This means in effect that the economy is losing its capacity to generate foreign exchange outside of the energy sector, notwithstanding the boasts about T&T manufacturing sector, being a dominant force in Caricom. The implication is that a sudden decline in earnings for energy will throw this economy into an immediate tailspin. A second possible weakness is the heavy outflows of private capital observed on the Capital Account. Some of this is going towards private external investments which ought to lead to reverse flows of factor incomes in subsequent years. But there is growing suspicion that a portion may be capital flight.

When viewed from the Balance of Payments side, there can be no denying the fact that the economy is highly exposed to risk of decline in hydrocarbon earnings through temporary cyclical collapse in prices or a more structural and terminal depletion of reserves. The Government is not unaware of this and would argue that it has taken steps to diversify the economy. The most referenced strategies relate to the establishment of an international financing centre, tourism, and the identification of seven targeted non energy sectors.

While the Governments efforts in this regard are commendable each of area is fraught with challenges, which suggest that their results are at best long term.

Moreover in all areas Trinidad and Tobago will face significant international competition. In the case of the Financial Centre for example, Finance Minster Nunez Tesheria was first to admit that amendments to the Financial Institutions Act was a necessary precondition for success. Moreover, she advised that both Barbados and Jamaica are ahead o f us in this regard. With respect to the new targeted sectors the major problem seems to be a lack of interest on the part of investors. Strategic Plans have been developed for each sector and in some cases Government has established a state enterprise to seed investment in that particular area. When and whether these initiatives will yield results is left to be seen. On the question of tourism, all engaged in the sector would admit the Trinidad and Tobago is perhaps last out of the block. It faces a number of challenges including basics like limited room capacity, and a diffused focus. Again , Government has intervened by investing in new hotel rooms and seeking to promote T&T as a conference destination. These initiatives may or may not work. My concern is that their capacity to earn net foreign exchange is limited in both the short and long run.

If it is accepted that availability of foreign exchange is critical to our sustainability then greater priority must be placed on utilizing current surpluses to create financial wealth. This would require a higher level of savings into the Heritage and Stabilization Fund as well as a change in the philosophical approach to savings. Under the current arrangements savings into the Heritage and Stabilization Fund occurs as a residual after expenditure is taken care off. There is therefore no conscious fiscal rule or target , so savings will occur if and only if prices and revenue are favourable.

This contrast sharply with the approach of Chile – a county with per-capita income of US12, 000, compared with T&T $16,000. Chile supplies about 30 % of the world copper and is currently enjoying windfall earnings from high prices. In 2006, Chile established two Funds to harness its new found wealth.

According to the rules of accrual, the Government reserves 0.5% of GDP from its copper earnings into its pension fund, and 1% of GDP into its Economic and Social Stabilization Fund The result has been that within two short years Chile has accumulated some US$ 16 billion in these funds. The Funds are now at a level where interest earnings can contribute meaningfully to fund growth and or the sum of national foreign exchange inflows.

While tight fiscal rules governing the accrual and withdrawal of windfall revenues are the norm today in most countries, the Government of T&T, considers such rules to be ‘restricting its fiscal flexibility”. For example, last week’s request by Government for an additional $ 3 billion would have been a non starter in Norway or Chile. The Governments and people in these places understand that power that accumulated financial capital in both the short and long term. In the absence of a similar mindset in T&T, we would continue for a long time to live on the edge hoping and praying that oil and gas continue to meet and exceed our international commitments. Given the cyclical nature of commodity markets and the finite nature of these resources we are treading on dangerous ground.

{kind=link}

{kind=link}