Slow Fiah, Mo Fiah and the Guyanese Growth Stagnation

Introduction

In my third column (SN July 22, 2009) I noted that Guyana’s GDP grew at a paltry average rate of 0.86% since 1998. There are many excuses that have been proffered over the years for this performance. For example, the global financial crisis was recently proposed by several letter writers even though the sub-prime crisis broke in 2007 and did not start to adversely impact on the Caribbean until 2008. World prices and adverse global shocks are often proposed as excuses. Yet another popular apology is the external debt that is said to have prevented the government from pursuing an economic strategy that could have placed the economy on a stronger footing. The latter argument holds that this debt was so burdensome that it affected the government’s thinking so much so that it could not pursue other developmental strategies concomitantly with the debt relief agenda, which by the way had a global impetus led by the non-governmental organizations (NGOs).

Of course, a now popular alibi is the political protests and violence that emanated from certain elements in the opposition. It is now clear from the revelations in New York that the violence did not only originate from opposition elements, but also a phantom squad whose leader alleged that he helped the government fight off the opposition fighters. I will use the term “slow fiah, mo fiah” of President Hoyte to represent the latter variable – the violence that emanated from the “Taliban” and the phantom. The impact of the other explanation on Guyana’s economic growth will be examined in subsequent columns; while this column will be used to examine whether “slow fiah, mo fiah” really had a major adverse impact on the mediocre economic growth performance.

Why is economic growth important?

Economic growth is important for the sustained creation of wealth. By economic growth I mean the percentage change of Guyana’s real GDP over time. Indeed, there is no guarantee that the gains of economic growth would be shared equitably or fairly. However, try sharing a stagnant roti to a growing family! Sooner or later each member of that family will get poorer even though the father eats the bigger share of the roti. Similarly, without economic growth Guyana would not be able to pay public servants better wages. Teachers, police officers, nurses, university lecturers would not obtain better wages over time.

The same is true for private sector employees at DDL, Banks DIH, Neal and Massy, etc. If wages increase in a stagnant economy eventually prices will start to increase. For those who are unemployed or underemployed, economic growth is essential for creating the jobs. Growth is essential for maintaining the new schools, hospitals, convention centre, stadium that were built by grants and soft loans from abroad. Moreover, growth is essential to keep the flow of investment going to create the next round of growth. In general therefore economies that stagnate will have miserable citizens who have to flee to little Caribbean islands to find jobs and to be mistreated.

Some readers would have figured out by now that my columns do not advocate one or two year positive growth from a long and sustained period of poor growth. The reader should know that growth can come from a low base or poor performance over a sustained period of time – example the 1998 to 2006 period in Guyana; 2007 and 2008 witnessed an increase in growth partly because Guyana was emerging from a long period of economic stagnation (the same can be said about the 1991 to 1994 period). My columns, on the other hand, advocate growth from structural transformation. The latter means the production of goods and services that satisfy the following conditions: (i) are income elastic (meaning the rest of the world will buy more of it as their income rise); (ii) price inelastic (meaning the rest of the world cannot really do without our goods and services or there are not that many substitutes); and (iii) goods and services that are not susceptible to early diminishing returns (meaning the productivity of the sector is not declining). Those who work in diminishing returns sectors, example sugar production, would experience wage squeeze. I hope sugar workers get the gist of the latter point.

Private investments

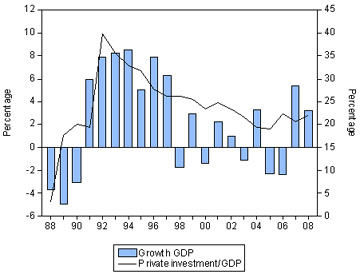

A lot has been said that the private sector is the engine of growth. The government, the IMF and the World Bank have all alluded to the importance of private investments for economic growth. I agree. President Jagdeo has even talked about his NEPS – the New and Emerging Private Sector. Therefore, what is the percentage of private investment relative to GDP? It is easy to track this number as the Bank of Guyana records it in its Annual Reports. Figure 1 presents the percentage of private investment in Guyana relative to GDP – henceforth this ratio will be called the private investment rate (PIR). The PIR is shown in the dark line in figure 1 on the right axis.

Since many have said PIR is the engine of growth, I have also included the percentage rate of growth of real GDP (left axis). The chart shows a clear trend – high PIR is associated with higher GDP growth. The PIR reached its peak of 39.8% under Hoyte in 1992. That same year economic growth reached a spectacular 7.9%. In 1993 the PIR was a healthy 35.8% and GDP growth was a hot 8.2%. It is clear from figure 1 that Mr. Hoyte was beginning to do something good and the economy was experiencing a return from the dismal years. The PIR was again a healthy 33% (even though it started to decline) in 1994 and growth was a fast paced 8%.

However, something started to occur to the PIR from 1994. The rate started to decline and so too did GDP growth. The chart suggests that the sizzling rate of 39.8% in 1992 was never again repeated for the next sixteen years. What does this have to do with our independent variable slow fiah, mo fiah? The point is slow fiah, mo fiah did not commence until 1998 but the PIR was already decreasing four years before 1998. Therefore, there have to be some other explanations for the lacklustre growth of the private sector and not only the political variable.

However, let us focus some more on the political variable for now. By the jailbreak of 2002, the PIR plummeted to 23% and economic growth in that year was a lukewarm 1.05%. As the New York trials revealed, the phantoms (the other side of the mayhem) started operations in 2003. The PIR and GDP growth were 21.5% and minus 1%, respectively, in 2003. There was a slight increase in the PIR from 2006 partly due to the rise in spending for cricket world cup. As we can see economic growth turned positive from 2007.

Figure 1, Private investment rate and GDP growth – 1988 to 2008.

Foreign direct investments (FDIs)

Figure 2 shows the level of net FDIs that flowed into Guyana from 1988 to 2008. These numbers were taken from the Bank of Guyana’s Annual Reports. It is clear that there was a first major peak of US$138 million in FDI for 1992. Subsequently, the rate diminished precipitously and stayed flat during the Jagan years from 1993 to 1997. Note that this drop in FDIs could account for the declines in the PIR. Could it be Dr. Jagan’s Leninist orientations that led to distrust for foreign investors and the subsequent decline? In any case, it would seem as though the lack of a clear economic vision of a role for foreign investors was missing during this period.

Figure 2, Foreign direct investments – 1988 to 2008 (US$ million)

Starting in 2005 the Jagdeo Administration seemed to have changed course as the data shows that the largest inflow of foreign investments occurred from 2005. However, in spite of these inflows the PIR is still lower than the early 1990s. This is an interesting development that deserves further analysis. Why have these large unprecedented inflows of FDIs under the Jagdeo regime not contributed to the increase in the PIR and faster GDP growth? Could it be that the local private sector is decimated from the political problem and the underground economic activities (such as smuggling) that the inflow of foreign investments is not enough to raise PIR?

One potential explanation has to do with the way the FDI numbers are calculated. For instance, re-investments by incumbent foreign firms to provide for depreciation of machinery, buildings, etc are counted as FDIs; therefore, when Barama spends on new machines or vehicles in 2008 that become part of FDI even though that company was established in Guyana since 1991. The point is if a large part of the spending is of this nature then FDIs are just maintaining current production and not adding to new production – the key for positive economic growth. However, the latter cannot be the only reason why the numbers are so high by historical levels.

Conclusion

The key point of this article is slow fiah, mo fiah could not be the only reason for the dramatic slow down in Guyana’s economic growth between 1998 and 2006. We saw that the private investment rate (PIR) began to decline during the years of relative tranquillity and peace in Guyana. As figure 1 indicates, the PIR started to decline from the time the new PPP government came to power. While the political problems certainly impacted adversely later, the seeds for mediocre growth were already sown before 1998.

Moreover, the data show a significant increase in FDIs from 2005 yet the PIR remained relatively flat. The latter is a conundrum that could be explained by the negative total factor productivity growth some researchers have found for Guyana. I will soon write a column to outline what are some of the social and political conditions that could cause the negative productivity growth in Guyana. ts to: tarronkhemraj@gmail.com