Introduction

Introduction

In his press briefing on Friday, October 22, 2010, President Jagdeo said that he does not see the Value Added Tax as a burden and therefore there is no need to revise it with a view to lowering the rate. He sought to divert calls for a reduction in the rate of VAT by spinning the consistent increases in the VAT collection as a result of widening the tax net and because of the better performance of the economy over the years. This to me demonstrates how little respect Jagdeo has for the nation and its intelligence.

At one level Jagdeo is right, that he personally does not see VAT as a burden. Indeed he would have been just as right had he said he sees no tax as a burden. And for one very simple reason. He pays no tax in Guyana. Under section 13 of the Income Tax Act, his official emoluments are exempt from income tax. And section 6 of the Property Tax specifically makes that act inapplicable to the President while section 5 of the Capital Gains Tax says that if Property Tax does not apply, then neither does Capital Gains Tax.

Presidential tax planning

Because rental income is not official emoluments it was not tax efficient for President Jagdeo to lease his Pradoville One house, since the net rental would have attracted income tax at the rate of 33⅓%. So what did the President do? Instead, he reportedly sold the property for $120M that no more than two years earlier he had valued in a division of property matter with Ms Varshnie Singh at $10 million. On that transaction alone President Jagdeo saved in Capital Gains Tax approximately $22 million! If the property had been rented over a period of time to earn the same $120 million, then assuming that the maintenance costs were borne by the tenant, he would have had to pay $40 million in taxes.

In other words, the sale by President Jagdeo of his property, the land for which he received at a subsidised value from the state, has cost the tax system between $22 million and $40 million! See why everyone wants to be a president? And on a salary of $1.5 million per month, the state forgoes income tax of close to $10M each year.

In fairness to President Jagdeo, he did not write the tax laws of which he is now the major beneficiary. That was done by Mr Forbes Burnham, whom many describe in unprintable language. Despite their socialist claims, neither of the Jagans thought of repealing this generous piece of legislation. But what Mr Jagdeo has done is made what was a temporary, ex officio benefit into a life-long benefit. Below are the benefits under the former presidents legislation he signed.

Presidential burden

For the rest of his life, President Jagdeo – and all future presidents as well – will enjoy, at the expense of the state, a free and unlimited supply of water, electricity and telephone services to his Guyana home; unspecified numbers of clerical and technical staff, gardener, maid and personal staff; fully paid medical attendance and treatment for himself and family, without limitation; full-time personal security and services of the Presidential Guard Service; unspecified number of vehicles to be provided, all expenses and costs paid by the state; two first-class return airfares provided on the same basis as that granted to serving members of the judiciary.

Most of these benefits would be considered taxable for the rest of the Guyanese. But not for the President. And if you think this is bad, consider that under this act, he will never again have to pay capital gains tax or property tax in Guyana, not ever! The one good thing is that this legislation exists in an act which any later Parliament can amend or repeal. It is worth speculating whether Mr Jagdeo could take the country to court if the Parliament were to repeal this immoral and colossally expensive act. In fact, that is itself a burden.

Clearly then the President does not have to bother personally about the impact of taxes or even VAT. While Mr Jagdeo is a consumer and would therefore suffer VAT on some purchases, unlike other ordinary Guyanese, his take-home pay and his gross pay are about the same. For the average Joe, VAT at 16% would have to be paid out of income already taxed at 33⅓%.

Selling VAT

Not being subject to the country’s wide, deep and draconian menu of taxes, the President may have honestly felt that the VAT is no burden. But let us remember that for practical purposes, he is also the country’s economist-in-chief, is a big spender and knows something about money and the nation’s finances. He played a big role in selling VAT to the nation, the architect-in-chief of a VAT system introduced under his watch four years ago. Yes, we may have adjusted and adapted to VAT and its sister, Excise Tax, but let us not forget that they only came into existence on January 1, 2007.

Having pronounced on the non-burden of VAT, the President then makes what he considers a natural progression in his line of reasoning: there is no need to revise it to lower it. But here he is being disingenuous. He and his Finance Minister have been reminded about his own sweeping, unqualified and oft-repeated commitment to VAT being “revenue-neutral.” So memory lapse is not an excuse. The nation has helped to remind him even as the people plead for relief.

But it did not need an economist to know that VAT was almost instantaneously a burden. Ram & McRae had said in its Budget Focus 2008 that “at some point the law and the tax can become excessively burdensome.” The accounting firm added that “if this point had not been reached, we certainly are very close.”

Remembering GUYEXPO

There was however no need to consider what others said or felt. Just consider what the President and his Finance Minister have said and how they have danced in delicate step on the question of VAT. The President needs no reminder of his speech at the opening of GUYEXPO 2006 during which he repeated his government’s commitment to the revenue-neutrality of VAT when he announced: “We said from the very beginning that VAT should be revenue-neutral, we are not looking to increase the collection of taxes, increase taxes or the revenue base with the introduction of this tax.”

Or that on its introduction, the government was adamant that the rate of 16% was arrived at after careful consideration and that any concession to the pleas of the trade union movement, consumer groups and civil society would undermine the Value Added Tax. Finance Minister Dr Ashni Singh insisted in his mid-year report of 2007 that the tax was revenue neutral. In fact, if we go back some months before the presentation of that report, Dr Singh, rapidly demonstrating all the schemes and skills of a politician, and disparaging the members of the opposition for suggesting that there would be a windfall, made it pellucidly clear how the government had computed “revenue neutrality.”

On page 206 of the Hansard records of the February 15, 2007 sitting of the National Assembly dealing with VAT he said, “If we turn to table VI of the Estimates, we see that the actual collections from the taxes that were abolished with the introduction of VAT, generated a total revenue of $24.3B last year, and so if the actual col1ections for these taxes were $24.3B for last year, and the projected collection for VAT is $24.8B, I have great difficulty in understanding where, Mde Speaker, is the windfall? These are facts of the matter.”

Well, if revenue neutrality was the goal and commitment, Jagdeo and Singh have gouged the people of this country more than fifty billion dollars.

Dancing with the facts

Dr Singh had to slither a bit when the results for full-year 2007 became public. It showed that VAT and Excise Tax had exceeded budget by $12.6 billion, or 49%. In fact for VAT alone the excess was a staggering 76% but since the two taxes were linked by the government in its revenue neutral commitment, the correct measure was the 49% excess in the combined rate.

By then of course, both the President and the Minister of Finance were aware that the rate of 16% was in fact the result of a mistake which his government had discovered very soon after VAT’s introduction. But instead of correcting the mistake, the government, under pressure to modify the rate, extended a deceptive compromise by agreeing to monitor implementation and make adjustments as necessary to bring relief.

Pity the Poor

For consumers, this was no theoretical matter. VAT is a tax on them. If the tax is not properly formulated, it is a hugely regressive system of taxation because it is imposed on expenditure. The poor do not earn enough to save; they are more affected by VAT than those who earn enough to save. Let us forget for a while that the business class has also exploited the VAT and are the biggest VAT cheats. I have in my possession a single invoice issued earlier this year by a Berbice businessman that was not only in breach of the VAT Act but cheats the revenue of close to $100,000! And that is one invoice for one businessman on one customer.

Sorry about the digression. By the time of VAT’s introduction, the government had removed the lower rate of 20% for the first band of taxable income. The wretched poor and not so poor therefore found themselves in the same tax bracket as the better off folks, paying the same rate of personal tax on income – 33⅓% – and out of the balance were then forced to pay the incorrect, immoral rate of 16% on the VAT-able items of goods and services they consume, including the meal at the corner restaurant.

With all the cheats and cheating, VAT even with poor administration is a huge tax gatherer. And the IMF and the government tried their best and placed considerable resources in ensuring that the poor did not get away. Pity that the same effort was not placed against the VAT cheats that dominate our commercial centres and rural areas. VAT has continued to be a major revenue source and even in 2010 when we expect the economy to grow by less than 3%, VAT takings over the first half of 2009 were 9%. Despite this, the Minister expects the full year increase to be only 5%!

Table

Central Government

Abstract Revenue by Head

G$ Millions

Source: National Estimates and Mid-year Report 2010

Conclusion

When the first year results of VAT became known, Ram & McRae confidently and generously said in its Focus on Budget 2008 after the size of the windfall became known that “it would now be immoral for the Government to renege on its commitment to adjust the rate of the tax to make it revenue-neutral.”

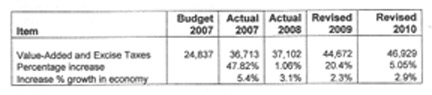

Since the year of VAT’s introduction, the economy has grown by 5.4%, 3.1% and 2.3% and for this year it is projected to grow by 2.9%. Compare that with the growth of VAT collection for the same years: 47.82%, 1.06%, 20.4% and close to 6%. But if you take what he said at GUYEXPO 2006, those things had nothing to do with revenue neutrality.

Once again President Jagdeo and Dr Singh have been caught out. I am not sure they care, however, well looked after as they are and with the peoples’ taxes available to silence critics and buy support. My own view is that VAT should be made into an election issue. I am prepared to consider casting my vote for a party that commits itself to correcting the dishonesty that has characterised VAT.