The previous two columns outlined some of the crucial issues surrounding the financial crisis in the United States. We noted that as asset prices plummeted, liabilities did not adjust downward, thereby plunging the financial system into aliquidity crisis that required the Federal Reserve (America’s central bank) to intervene. The Federal Government also intervened with the Troubled Asset Relief Program (TARP).

A similar situation occurred in the Caribbean with respect to CL Financial – the Trinidad and Tobago conglomerate that includes CLICO – which was exposed to the US through its investments there.

As a result, the Central Bank of Trinidad and Tobago in January 2009 was forced to bail out CL Financial. The Guyana branch of CLICO was also caught up in the global financial crisis because of that institution’s investments in the US. CL Financial and the Guyana CLICO faced a classic liquidity run given large withdrawals.

As a result, the Central Bank of Trinidad and Tobago in January 2009 was forced to bail out CL Financial. The Guyana branch of CLICO was also caught up in the global financial crisis because of that institution’s investments in the US. CL Financial and the Guyana CLICO faced a classic liquidity run given large withdrawals.

In spite of the CLICO meltdown, Guyana was spared a system-wide financial crisis. Government Ministers have been quick to point out this fact. They adduced this outcome to the government’s prudent macroeconomic policy. Indeed there have been improvements in several key macroeconomic indicators in recent years. For instance, the overall fiscal deficit (when external grants are included) has narrowed in recent years. On the balance of payments, the current account deficit is still over 10% (negative) of GDP although it has also narrowed in recent years. However, none of these key macroeconomic indicators accounts for the relative financial stability.

Instead this stability comes from the investment pattern of Guyanese banks and the nature of capital inflows (non-income monies that flow into Guyana). Let us first examine the investment pattern of Guyanese banks. Table 1 below presents the percentage of total assets accounted for by each class of asset over the years 2000 to 2009. The main assets are foreign assets, credit/lending to government, credit/lending to private sector, and reserves (required + excess) and deposits at the Bank of Guyana. The numbers reported are percentages. From the table it is obvious that most assets are in domestic currency (Guyana dollar) and foreign assets (foreign securities and currency) account for a smaller share up to the point of the occurrence of the global crisis in 2007.

In spite of the global crisis, foreign assets actually increased. One would expect that the foreign exposure would decline as Guyanese asset investors shun the foreign class of assets. Furthermore, if Guyanese banks had invested in volatile American financial assets, there would have been a decline in the percentage of this asset as market prices crashed in the US and Europe.

Further research is needed to gauge the exact composition of foreign assets of commercial banks. One hopes that an enterprising researcher from UG would take up this task. Does this asset class, foreign assets, include derivatives and asset-backed securities? Is it mainly US Treasury bills? Is it mainly deposits in foreign counterpart banks? Or is it mainly foreign currencies? Given the data reported in table 1, it is doubtful that Guyanese banks invested in speculative and volatile foreign assets, the kind that brought the United States to its knees.

Table 1. Asset composition of commercial banks (percentages)

An obvious question remains: does this investment pattern reflect prudent government management of the economy? Has the government placed restrictions on the type of foreign assets and securities in which our banks can invest? If this can be established then government policy would have been successful here. What we do know, however, is Guyana liberalized the capital account of the balance of payments, allowing for the free inflow and outflow of hard currencies.

This was part of the policy prescriptions from the Economic Recovery Programme implemented by President Hoyte. Therefore, nothing is available publicly to indicate the government’s prudent management of capital flows.

In the series of Development Watch columns in which I examined the reasons for the exchange rate stability after 2004, I argued that the rate stability reflects the market power of the commercial bank traders, which dominate the trading of hard currencies (90% of all trades in the reported data).

The market power is validated by increasing concentration in the Guyana foreign exchange market. Measures of concentration have confirmed this fact. Therefore, if the Bank of Guyana uses moral suasion when targeting the exchange rate, then the central bank would have been successful in steering the economy away from a bumpy path in times of global crisis. The high concentration of the market means that the central bank only needs to target the rate set by the main commercial bank traders.

Table 1 shows that the commercial banks invest mainly in domestic assets. Therefore, it is not in their interest to see a rapid depreciation of the Guyana dollar. If anything, they would prefer an appreciation. But that comes with its own problems as exports become less competitive. A depreciation of the rate would result in inflation as importers mark up retail prices over the rising import price.

This is particularly true as Guyana imports most of what it consumes. Inflation would be very harmful to banks as their assets are mainly in Guyana dollars. Therefore, we have another reason why the dominant commercial bank traders would prefer to see a stable exchange rate, even in times of global crisis.

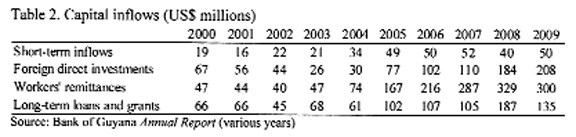

Table 2 also gives some clues as to why there was not a systemic meltdown of the financial system. The table shows the type of non-income foreign monies (capital inflows) that flow into Guyana from 2000 to 2009. Most of the funds are non-volatile inflows that cannot be reversed overnight.

The only category that would be susceptible to sudden flight and reversal is short-term inflows (mainly foreign deposits). Indeed, there was a steep drop from US$52 million in 2007 to US$40 million in 2008. This number rebounded to US$50 million in 2009. In spite of the erratic nature of the short-term flows there was no serious threat to the exchange rate or the banking system.

The first counterbalance to the sudden drop in short-term inflows would be the steady and persistent upward trend in remittances. The data show that throughout the crisis remittances have increased. This is not surprising because one published peer-reviewed academic study suggested that Guyanese abroad send money home because of altruistic motives. This implies that even in recession Guyanese in the Diaspora would still maintain the cash and gifts in kind sent to families and friends at home.

Foreign direct investments (FDI) are also not susceptible to sudden reversal. Foreign investors who built buildings and plants in Guyana cannot pack up and leave in times of sudden panic. Exit could take months. Long-term loans and grants also possess this feature. Therefore, even though Guyana has liberalized the capital account allowing for free inflows and outflows, circumstances have conspired to have only stable inflows of foreign funds.

One of this would be the lack of development of capital markets.

The stock market does not attract foreign short-term capital as those in Asia at the time of the Asian Financial Crisis.

There is no active trading of bonds or commercial papers in Guyana. These markets would tend to be much more reactive to foreign panic. However, a bank-dominated financial system could be more suitable for long-term stabilization; particularly if they are oligopolistic banks.

Table 2. Capital inflows (US$ millions)

Source: Bank of Guyana Annual Report (various years)

In conclusion, Guyana was able to dodge the crisis because of the nature and structure of capital inflows and the financial system. Using moral suasion, the Bank of Guyana could have played a role in the stabilization of the exchange rate.

Please send comments and criticisms to: [email protected]