True and accurate

The condition of the manufacturing sector offers a glimpse of what is wrong with the economic conduct and policy of the current administration. In 2006, the year that was considered the most relevant for rebasing the gross domestic product (GDP), the manufacturing sector’s contribution to the national economy was eight per cent. The importance of the rebasing exercise, according to the Bureau of Statistics, was that it enabled Guyana to “capture the real picture of the economy” by updating changes in price and changes in production and consumption patterns. This means that the situation of the manufacturing sector as gleaned from the national accounts of today could be considered as a true and accurate reflection of its current condition. Placing faith in the data presented in the 2011 budget, the manufacturing sector is now contributing seven per cent to the GDP of Guyana. Even under the old GDP series, manufacturing has moved from contributing nine per cent to GDP to seven per cent. With this information, it is now safe to say that the manufacturing sector is stuck in reverse gear.

Disbelief

Despite this reality, the administration has boldly predicted that the manufacturing sector will expand output by 7.7 per cent in 2011. With complaints of neglect emerging from some quarters of the manufacturing sector, Guyanese must be wondering if the high expectations of the administration are not misplaced. This view of the administration’s optimism is validated by the realization that it is pinning its hopes on the beleaguered sugar industry to reach the level of growth that it is predicting. Somehow, the administration thinks that the sugar industry with its labour, management and production problems would beat all odds and generate a 35 per cent increase in output in 2011. If you blinked your eyes in disbelief, it is only because you read that number correctly. Without any solid evidence to support this growth outlook, these lofty expectations of the administration could best be described as economic posturing.

Despite this reality, the administration has boldly predicted that the manufacturing sector will expand output by 7.7 per cent in 2011. With complaints of neglect emerging from some quarters of the manufacturing sector, Guyanese must be wondering if the high expectations of the administration are not misplaced. This view of the administration’s optimism is validated by the realization that it is pinning its hopes on the beleaguered sugar industry to reach the level of growth that it is predicting. Somehow, the administration thinks that the sugar industry with its labour, management and production problems would beat all odds and generate a 35 per cent increase in output in 2011. If you blinked your eyes in disbelief, it is only because you read that number correctly. Without any solid evidence to support this growth outlook, these lofty expectations of the administration could best be described as economic posturing.

Frustration

With G$4.3 billion to be thrown at the sugar industry this year, the frustration that is coming from small manufacturers is well understood. Sugar might be a special culprit but the manufacturing sector as a whole is in danger of stagnating and is in need of a coherent policy to rescue it from its submerged position in the Guyanese economy. According to the disclosures in the budget, output in the manufacturing sector grew by less than half of one per cent last year.

Unprepared

The seemingly unprepared condition of the sector to play its catalytic role is of concern because the manufacturing sector is critical to the sustained diversification and competitiveness of Guyana. It increases opportunities for domestic and foreign investment in Guyana. It provides stability to the agricultural sector. The expansion in investment brings jobs, an increase in output and opportunities for expanding exports. With competition, supplies increase, the variety of products expands and prices fall, all of which are of interest and importance to Guyanese consumers. So, the condition of the manufacturing sector in Guyana has real consequences for employment and the quality of life. These goals were deemed sufficiently important by the international community that the Inter-American Develop-ment Bank (IDB) gave the administration about US$27 million a few years ago to help Guyana diversify its economy and to increase its competitiveness.

Cozy

This link between performance and spending would not be an issue if the IDB money was not so specifically targeted. It also raises questions as to whether this project should not have been managed by an independent group with less ties to the political establishment in the country. Instead, the money for competition and diversification is being managed jointly by the administration and the private sector through the National Competitiveness Council. The irony of this arrangement is that the Council is supposed to act as an advisor to the administration. Instead, it has become an instrument of the administration with the majority of its members coming from the administration, and with the Council being chaired by the President. This cozy relationship could only be helpful to some in the manufacturing sector and not to all.

Power players

The manufacturing sector has a set of large, mature companies that dominate it and which might be satisfied with the way things are. Despite the slow growth of the manufacturing sector, the gross revenues for this sector went up by 32 per cent from where they were in 2006. At the same time, output increased by only 3 per cent. Many of these companies are power players in the economy who wield exceptional clout on their own. Some of them are major employers, some are major exporters and some are major shareholders of large banking institutions in the country. Some have subsidiaries at home and investments abroad. Some of the major manufacturers are members of the Guyana Stock Exchange.

At the same time, there are smaller growth oriented companies which have less influence and need much more robust support from the administration and do not seem to be getting enough of it in a coherent fashion. A hodge-podge of financing activities without opportunities to lower cost, obtain a stable supply of inputs and increase productivity might be stripping smaller companies of the energy to move forward.

Wrong company

In addition, the smaller operators in the sector might just be keeping the wrong company. They ought to be working with the Small Business Administration (SBA) to gain advantage. That entity is also represented on the National Competitiveness Council and should be benefitting from the IDB money. Functioning in that grouping could help increase the leverage and impact of the SBA in discussions about the sector. Moreover, they should be working assiduously to see that the Small Business Act of 2003 was fully implemented, including the establishment of the small business fund that would be dedicated to their interests. By redirecting their efforts towards the SBA, smaller manufacturers might give themselves a better chance at success in influencing policy and in getting ahead.

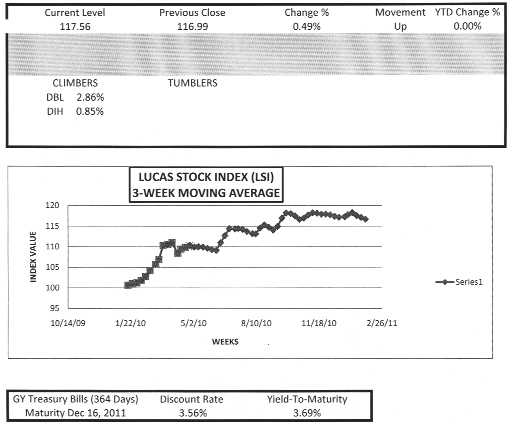

LUCAS STOCK INDEX

At the end of trading in January 2011, the Lucas Stock Index (LSI) is about where it was at the end of 2010. The index continued its slow but steady climb and added another half of one per cent to dig itself out of negative territory. Even though more stocks were traded this week, only two of them Banks DIH (DIH) and Demerara Bank Limited (DBL) recorded positive changes. The rest of the traded stocks showed no change from their last trade price. These included the stocks of Caribbean Container Incorporated (CCI), Demerara Distillers Limited (DDL), Guyana Bank for Trade and Industry (BTI) and Republic Bank Limited (RBL). Despite the sustained positive movement of the index, it continues to lag behind the yield on the risk-free Treasuries that will mature in December 2011.