Dear Editor,

After reading and re-reading Mr Anand Goolsarran’s carefully crafted letter to SN, Sunday, July 22, one feels compelled to make some observations, even though they relate to what may be regarded as (minor) details.

The actual records will reveal the following:

i) Ms Geetanjali Singh’s actual qualifications include the ACCA and Master’s Degree in Public Policy and Management.

ii) She rejoined the Office of the Auditor General in 2002. At 2005 her position was Assistant Auditor General.

iii) In the year 2005 the respective incumbents were as follows: Auditor General (ag) – Balraj Balram; Deputy Auditor General (ag) – Deodat Sharma.

The first demitted office. His replacement was Mr Sharma and Ms Donna Ellis was appointed to act in the latter’s position.

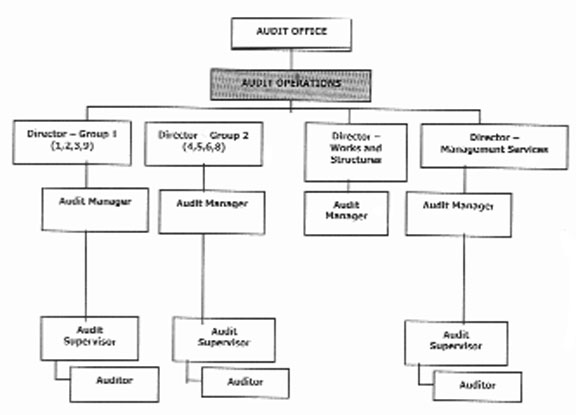

2005 was the year arrangements were made to reorganise the Audit Office, following its transition from a regular budget agency to a constitutional entity reporting to Parliament via the Public Accounts Committee. The new organisation structure was formally approved by Parliament. The posts of Senior Deputy, Deputy and Assistant Auditor General were deleted from the structure.

The reorganisation structure included the following specific auditing components:

Mr Goolsarran may not have been aware that the new structure which was instituted included the deliberate assignment of specific groups of auditees to the respective Directors (3), to each of whom an Audit Manager reported. (So it could not have been any recent accommodation of the Auditor General (ag)). From 2006 therefore the regulatory framework provided for the senior management team of directors to collate reports and formulate related opinions. Accordingly the latter could not be attributed to any one official, although the Auditor General (ag) would have to take final responsibility therefor.

Incidentally at no time did Ms Singh occupy the position of Deputy Auditor General. In the new dispensation she was one of the Audit Managers (ag).

Further, none of the commentaries so far have asserted their acquaintance with the actual Conflict of Interest Code which is part of the Regulations to the Act, or else they would have recognised the real potential of all the auditing teams being vulnerable.

The question being posed is, if as currently constituted Ms Singh’s portfolio does not include auditees who report to the Ministry of Finance, is there an explicit (and exclusive) conflict of interest?

In this connection it seemed to have been overlooked that by law the Audit Office itself is subject to audit.

A final question relating to a comment that Ms Singh was one of two qualified audit/accounting officials, the other being the Auditor General (ag): Does Mr Goolsarran consider a UG degree in Accountancy a professional qualification, taking into account international standards with which the discipline is required to comply? If yes, then it should be noted that two other (now) Audit Managers have the same qualification as their boss.

So far as the Auditor General (ag) is concerned, however, there are certainly substantive issues of ethical standards, independence and competence. Witness the non-submission of relevant reports on critical national projects retrospective to several years, and to which attention has repeatedly been drawn.

As observed by Mr Goolsarran, the urge should be for his replacement.

Yours faithfully,

E B John