Where the mind is without fear and the head is held high;…

Where words come from the depth of truth;

Where knowledge is free;…

Where the mind is led forward by thee into ever-widening thought and action –

Into that heaven of freedom, my Father, let my country awake.

Taken from Gitanjali by Rabindranath Tagore

Introduction

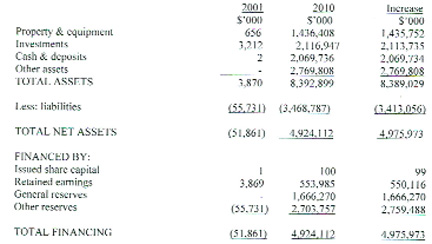

In last week’s column, we looked at the auditing arrangements for NICIL, the accounting implications of the vesting of State assets as well as their disposals, and the accountability for the proceeds. We noted there was a lack of compliance with the Companies Act in relation to annual financial reporting and audit since the audits for 2001 to 2010 were finalized within a little over one month in late 2012. A “clean bill of health” was also given to NICIL’s accounts. I acknowledge a mistake I made by including the 2001 audit report which I discovered was issued earlier than 2012. However, this did not change the complexion of my analysis.

When the assets vested in NICIL are disposed of, a windfall gain is achieved since NICIL acquired them from the Government free of cost. This apart, the vesting of assets for the purpose of selling them is not in keeping with the relevant section of the Public Corporations Act that was applied to vest assets in NICIL. (That section deals with the vesting of assets in a new corporation to assist it with its start-up operations.) The proceeds should therefore have been paid over to the Consolidated Fund, net of expenses.