As expected, the section of the Budget Speech from which this is taken takes up the largest part of a very long speech.

In introducing the 2013 budget the Minister committed the government to continuing the policy environment which prevailed in 2012. He identified as the policy agenda that the Government ‘…will continue to be guided by the seven prerequisites outlined last year, namely, a strong democracy, reliable and efficient institutions of state, long term macroeconomic stability, economic diversification and growth, expanded physical infrastructure, high quality social services, and environmental responsibility and sustainability’.

The following principal issues were announced:

The Government is committed to continue the LCDS of which the Amaila Falls Hydropower Project was described as a flagship.

Ensuring the viability and profitability of the rice and sugar sectors remains policy priorities.

The Government is considering necessary policy and institutional frameworks for the petroleum sector.

Legislation will be introduced for amendments to the Anti-Money Laundering Act; a revised Insurance Act; a new Pensions Act; and reviewing legislation governing credit unions, with the aim of bringing them also within the supervisory perimeter of the Bank of Guyana. Licensing and establishment of a credit bureau is noted as imminent.

The National Competiveness Council will spearhead the work to implement an action plan to address ten policy areas of the business environment out of sixty issues which have been identified.

Every Budget Agency will be mandated to improve processing times for delivery of services to the public and to institute more client friendly systems.

Strengthening the internal audit capability within central government and ensuring greater oversight for actions taken when recommendations are made for improvement.

Targets

Overall real growth is projected at 5.3% in 2013 with the non-sugar economy and the sugar economy projected to grow by 5% and 10.1% respectively.

Over the five year period following 2007, there has been negligible performance in the primary industry groups Agriculture, Fishing and Forestry; Mining and Quarrying; and Manufacturing) with their contribution to GDP falling from 67.23% to 58.72%. This declining performance is predicted to continue in 2013 with contribution to GDP budgeted at 57.24%.

The primary industry groups are addressed separately below. In the other sectors, Finance and Insurance Activity recorded the highest average growth of 11.31% to 2012. Growth in 2013 is expected to be 12%. The Construction sector recorded 0.78% average growth for the five years to 2012. The sector contracted by 11.0% in 2012 but is expected to grow by 10.0% in 2013. Growth in 2011 was 2.8%. Information and Communication increased from 1.5% in 2011 to 4.2% in 2012. The average growth for the five years to 2011 was 9.82 compared to 5.1 to 2012.This sector is expected to grow by 4.5% in 2013.

Agriculture, Fishing and Forestry

“Other Crops” remains number one at 24% of total output of this industry group while Sugar and Rice represented 19% and 14% respectively in 2012.

The Agriculture, fishing and forestry sector improved in 2012 recording a 3.7% growth in comparison with 2.7% in 2011. Growth of 3.7% is projected for 2013. The average growth for the five years to 2012 was 1.37%. Rice is also leading in this industry with average contribution to GDP of 7.14% followed by livestock with 6.34%. Livestock had a strong performance in 2012 of 14.4% compared to 5.8% in 2011. Average growth in 2013 is projected at 4.0%.

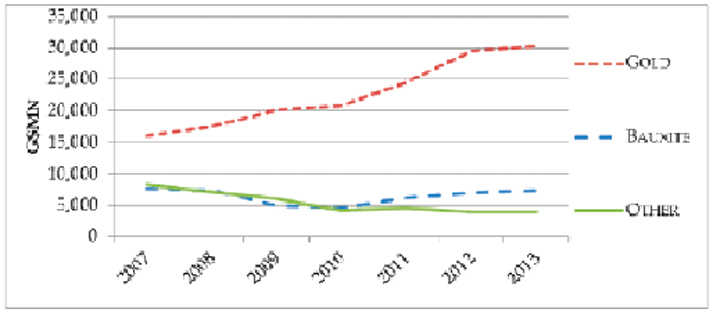

Mining and Quarrying

Source: Estimates of the Public Sector

Gold is budgeted to grow by 2.6% in 2013. Gold was expected to grow by 2.9% in the 2012 budget but revised growth in 2012 was 20.8%. The Bauxite sector is expected to grow by 6.5% in 2013. The sector was expected to contract by 0.2% in 2012 but revised growth was actually 12.5%.

Manufacturing

A 3% growth is projected for 2013 in the Manufacturing sector (other than sugar and rice).

Monetary Policy & Inflation

The Minister noted that monetary policy will continue to be aimed at price and exchange rate stability, and expansion in credit to the private sector.

The rate of inflation (Urban Consumer Price Index – Georgetown) for 2013 is projected at 4.3% compared with an actual of 3.5% in 2012. Food inflation in 2012 was 9.5%. Prices for Transport and communication fell in 2012 and recorded deflation in prices of 0.8% compared to inflation of 10.2% in 2011. Medical and Personal Care inflation in 2012 was 10.3%. Over the two years 2011 and 2012, food inflation was 5.98%.

Balance of Payments

The Minister projects a surplus of US$57.6Mn on the overall balance of payments compared with US$12.4Mn in 2012. On the trade side, merchandise exports are projected to increase by 6.93% to US$1,492.4Mn while merchandise imports are projected to increase by 8.98% to US$2,155.3Mn. With net imports of services at US$239.4Mn, and private transfers of US$450.4Mn, a net deficit of US$451.9Mn is projected on the current account.

The capital account is projected to have a surplus of US$509.5Mn in 2013 (US$428.5Mn in 2012). In this account, a net inflow of US$525.7.8Mn is expected from medium and long term capital while a net outflow of US$40.3Mn is expected on short term capital.

Ram & McRae’s comments

i Four sub-sectors are projected to record double-digit growth in 2013. Three of these are sugar – field and factory, construction and financial and insurance activities. Despite the threats and challenges which plague the Skeldon Factory and the labour force availability at the Demerara estates the Government seems wedded to an unrealistic notion that no structural changes are required to make the corporation viable.

ii The Minister’s projections seem to take for granted that the oil and the rice agreements that Guyana has with Venezuela will continue without modification in 2013. This assumption is probably realistic in the short term.

iii Instead of announcing how much will be spent on the National Health Strategic Plan 2008-2012 it would have been more helpful if the Minister indicated whether the National Assembly would be told of the achievements of the Plan.

iv The Minister did not indicate a policy of job creation or whether the Government will act on the Public Procurement Commission and legislation addressing corruption including whistleblowing protection.

v In view of the stated reasons for the exclusion of Guyanese from employment on the Kingston Marriott, the Minister was expected to announce how the Government intends to accelerate training to bring the Guyana labour force up to international standards.

vi Much of the content of this section of the Minister’s presentation was either irrelevant or meaningless and should be dispensed with. The Minister did not even attempt to link his speech with key sections of the Estimates to enable his colleagues to follow what he is talking about.

vii In view of the significant revenues of the state which accrued to entities like NICIL, Guyana Forestry Commission, GGMC and the Guyana Gold Board it would seem that the Minister of Finance has a duty to present to the National Assembly full and relevant details affecting each of them. Indeed, it is our view that the surpluses after expenses should be paid into the Consolidated Fund as “moneys belonging to Guyana”.