Introduction

The conglomerate, Demerara Distillers Limited, which has as its flagship the world famous El Dorado rum, will be holding its annual general meeting next Friday April 26 when the directors will report on the performance and state of affairs of the parent company and its ten subsidiaries and one joint venture. One of those subsidiaries, Breitenstein Holdings BV, a Netherlands company has two distribution companies in the Netherlands and four in the United Kingdom. The joint venture is listed as a Manufacturing and Distribution company in Hyderabad, India. At least two of the subsidiaries – Distillers Gas Company (sic) and Demerara Contractors and Engineers Limited – seem to have disappeared from the radar, the first mentioned as dormant in a note to the financial statements and the second receiving no mention in any of the documents making up the Annual Report. Included in the financial statements of the group as Associate Companies are Diamond Fire and General Insurance Inc. and National Rums of Jamaica Limited, 19.5% and 33.33% of whose shareholding respectively is owned by the group.

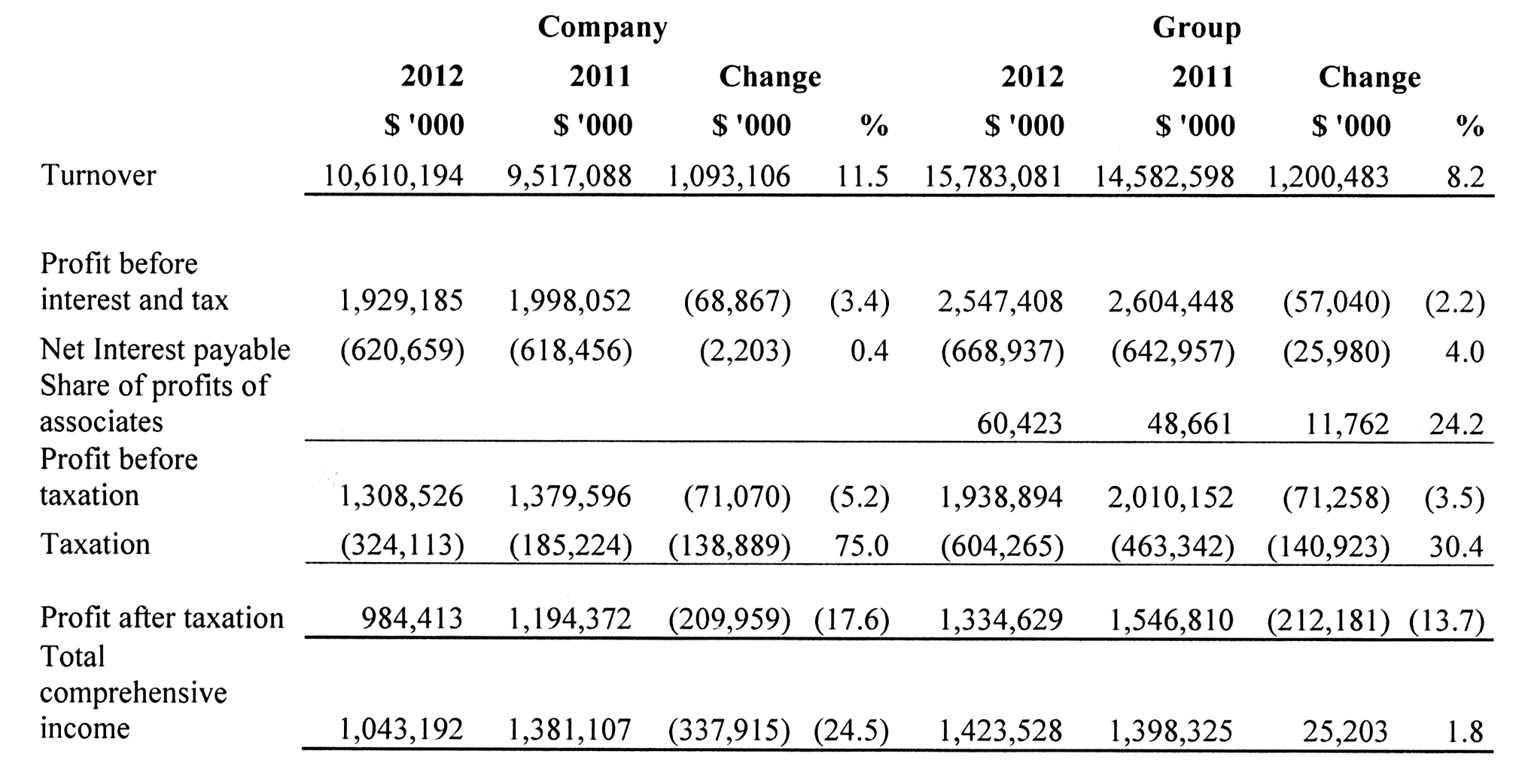

The Guyana Stock Exchange, itself stunted by conflicts of interest and a tolerance of a culture of weak governance among the handful of public companies, has been far from impressed with the group, attributing to it one of the lowest Price Earnings (P/E) Ratio. The consolidated financial statements show that turnover of the company has risen by 11.5% but that there were declines in profit before interest and taxes (5.2%), profit after taxes (17.6%) and total comprehensive income by nearly 25%. The combined performance of the subsidiaries was flat. Turnover (sales) increased from $5,065 million to $5,173 million, or by 2.1%, less than the rate of inflation. Profit before tax of the subsidiaries remained the same but after tax profits fell from $352.4 million to $350.2 million, a decline of 2.1%.

The Guyana Stock Exchange, itself stunted by conflicts of interest and a tolerance of a culture of weak governance among the handful of public companies, has been far from impressed with the group, attributing to it one of the lowest Price Earnings (P/E) Ratio. The consolidated financial statements show that turnover of the company has risen by 11.5% but that there were declines in profit before interest and taxes (5.2%), profit after taxes (17.6%) and total comprehensive income by nearly 25%. The combined performance of the subsidiaries was flat. Turnover (sales) increased from $5,065 million to $5,173 million, or by 2.1%, less than the rate of inflation. Profit before tax of the subsidiaries remained the same but after tax profits fell from $352.4 million to $350.2 million, a decline of 2.1%.

A significant contributor to the change was explained in the Chairman’s Report as due to a “deferred tax charge of $230 million as against $65 million in 2011.” No explanation was given for this increase, nor do the financial statements give any hint, particularly since there was no significant acquisition in fixed assets, a major factor in making a provision for deferred taxes, as the tax allowance is very often significantly higher than accounting depreciation in the first year.

A significant contributor to the change was explained in the Chairman’s Report as due to a “deferred tax charge of $230 million as against $65 million in 2011.” No explanation was given for this increase, nor do the financial statements give any hint, particularly since there was no significant acquisition in fixed assets, a major factor in making a provision for deferred taxes, as the tax allowance is very often significantly higher than accounting depreciation in the first year.

The important stock market consideration, Earnings Per Share (EPS) of the company fell from $1.55 per share to $1.28 per share dragging down that of the group’s EPS from $2.01 to $1.74 per share. However, with the way Guyana’s media overacts to absolute numbers, the market price for the shares has not been adversely affected. Or perhaps the market is responding to an increase in the dividends per share from $0.48 per share to $0.52 per share. Incidentally, someone in the company should tell the Company Secretary that Guyana abolished cents as a unit of currency in 1998!

Task for forensic analysts

I have tried to disaggregate for purposes of analysis the annual report and the financial statements in what is a task best left to forensic analysts. Note 22 to the financial statements suggests that the turnover of the Guyana subsidiaries – Topco, Distillers Gas Company, Distribution Services, Demerara Contractors and Demerara Shipping – declined in 2012. As noted above the company’s sales increased by $1,093.1 million, sales from Guyana locations increased by $595.4 million. If indeed the turnover by the Guyana subsidiaries fell by $497.7 million, no one will bother to discuss this situation.

So staying with the segment reporting the statements disclose that Guyana company sales increased by 5.1% but its margin measured by profit before tax divided by sales declined from 15.4% to 14.3%; sales by the European subsidiaries increased by 21% but margins fell from 7.6% to 4.9%; for the USA sales increased by 17.8% but the margin declined from 8.8% to 7.7%; for Canada the increase in sales was 6.7% but the margin increased from 27.1% to 38.9%; St Kitts sales increased by 48.0% and its margin increased from 23.9% to 26.1%. India is more than an enigma: value of sales was $16.2 million but its losses amounted to $31.1 million.

Many auditors, but are there enough audits?

I will return to India momentarily but let me note one qualification about the group and its subsidiaries which is probably unique among Guyanese companies and the Caribbean. The group companies are audited by three separate audit firms – TSD Lal & Co., PKF Barcellos and Company and Jack A Alli, Sons and Company. Additionally the Chairman of the parent’s Audit Committee Mr Harry Parmessar is the head of still another audit firm while a fifth firm Nizam Ali & Company audits Demerara Bank Limited, an entity listed in ‘Note 23 – Related party transactions and other disclosures.’ That takes some explaining but is not necessarily an issue. What is significant is that some jurisdictions, including those in which DDL’s subsidiaries operate, do not require certain categories of companies to have independent auditors. So I wrote Mr Parmessar asking him to let me know the appointed external auditors of each company in the DDL Group – both local and overseas. I also enquired about the value of the related parties’ transactions of those entities which are not audited. I received what has come to be known as the Brassington response: silence.

Without such basic information, and with confusing if not conflicting numbers in the various reports in the same document, no serious analysis can be done that would provide adequate comfort on the financial statements of the company’s subsidiaries which may or may not be audited, whether they are in India, Canada or Europe. On the issue of auditors of subsidiaries, the Companies Act simply requires the holding company (the parent), if required to do so by its auditors, to take such reasonable steps as are open to it to obtain from the subsidiary such information and explanation the auditors may reasonably require for the purposes of their duties as auditors of the holding company.

Indian odyssey

Let us now return to India where the company has had a joint venture operation Demerara Distillers Limited – Hyderabad for close to two decades. That JV was a misfortune from day one when DDL sought to set up in a dry state – one that forbids the production of alcohol. It has hardly got any better. The directors in the 2011 annual report gave some hope to shareholders that they recognised the scale of the India problem and would be “re-evaluating its India strategy against a background of significant [unspecified] legislation and other changes affecting the business.” The report announced that a decision on the way forward would be made in 2012.

That makes the omission of any decision about India in either the Chairman’s report or the Report of the Directors quite puzzling, particularly in the light of the poor or no performance of the Joint Venture, which was advertised in the 2003 Chairman’s Report as the gateway to the “South Asian markets.” This much seems clear: DDL’s investment in the JV is $267.8 million. The company’s share of the JV’s assets is $674 million but the revenue generated by those assets attributable to the group is $16.2 million while the group’s share of losses is $31.2 million. Caution is advised since Note 21 shows the share of income attributable to the group as $4.3 million and losses of $24.8 million.

But here is what is troubling. The group’s share of liabilities of the Joint Venture is $535.6 million, a major exposure with potentially costly consequences. If, as seems desirable, the JV is brought to an end, the fact that it has not been operating will affect the price which any buyer will pay, whether in a voluntary sale or in a liquidation. The directors, among whom are four professional accountants and an attorney-at-law, can no longer afford to dither. They need to face the Indian winter.

Poor investments

But India is not the only serious failure the group has had to face. It entered in and gave up the medical transcription service (Decipher International Inc); it went into the internet business (Solutions 2000 Inc) in a conflict of interest arrangement and that too it gave up. Trinidad appears to have been another failure while locally the gas company and the construction company appear dormant. What is less explicable is Topco, the fruit and juice company in which several hundred million dollars were invested in 2003 but which is almost as well known for its sponsorship of chess as for its products. The company reported a $16.4 million profit in 2012, an identical mirror of the loss it reported in 2011. Since the large investment, the company has made a cumulative loss of $17.2 million. Even if the profit in 2012 signals a change in the fortunes of the company, the time for satisfying any reasonable test of a payback period has long passed.

The direct financial cost of these failures may have seemed modest but given the nature of management that it is the problem companies, departments and projects that take up management time, it might have been a good lesson for the group to follow the basic rule of management: stick to your core competencies and your strengths.

Balance sheet

The balance sheets of the company and its combined subsidiaries continue to be satisfactory but some items stand out. At December 31, 2012, net inventory, which includes stock held for resale and “spares, containers and goods-in-transit,” an unlikely and unhelpful combination, is now $8,864 million, for the first time exceeding the book value of property, plant and equipment. At the same date, cash and bank balances amounted to $80.5 million which could mean that the company would have to increase its borrowings to pay the $308 million dividends which the directors are recommending.

Current liabilities including trade and other payables have increased over the previous twelve months by $1,275 million to $6,750 million. Major contributors to the increases were $400.6 million in overdraft and $906 million in payables, partly offset by a reduction of $182 million in the current portion of interest bearing borrowings.

The balance sheets show increasingly significant amounts of taxes recoverable, almost entirely by the parent company. The amount recoverable by the company amounted to $557.3 million, an increase of $146.8 million while for the group the amount recoverable was $661.6 million, up by $142 million. On the other hand the company’s tax liability shown as nil in 2011 is now $146.1 million in 2012.

Too much alcohol, too little taxes

The Cash Flow statement shows the company’s tax payments in 2012 of a mere $93.8 million. Unfortunately accountants around the world have used their influence and their financial clout to dilute to the point of meaninglessness disclosures on segment reporting so that it is not possible to get any idea of the revenues derived entirely from alcohol. We have sought out figures from the National Estimates and find the numbers staggering. These show that the value of alcohol consumed in Guyana, not including all the smuggled high value products sold at some of the exclusive night spots, amount to over twenty billion dollars! Put another way the consumption of alcohol per person in Guyana over the age of 18 is close to $50,000 per year!

Regrettably DDL which takes pride in its corporate social responsibility, is a major beneficiary of alcohol abuse in Guyana, an abuse that accounts for Monday being a no-work day for many of GuySuCo’s employees and in the construction industry. I am aware that alcohol gives pleasure and makes some contribution to the economy. But one need not be a Quaker to recognise that there is a darker side to it. Alcohol is a substance that affects both the body and the brain, it can contribute to, among other things, acute toxic effects, alcohol dependence, liver cirrhosis, cancers and contributes to overweight and obesity. But alcohol also affects families, is responsible for a high percentage of domestic and other violence and contributes in no small measure to the high incidence of traffic accidents and fatalities.

Apparently oblivious of the role of their company in all of this, the directors have not identified among their corporate social responsibility initiatives to “[enhance] the lives of their employees, consumers and citizens at large any project or programme to address alcohol abuse in Guyana.” That would not be hypocritical – it would be responsible.

Conclusion

Shareholders should not be too happy with the performance of the company and the group, which probably has its root in governance. There is need for a rethink of its various models and strategies and whether it is not time to abandon the combined role of executive President and Chairman, despite the absence of clear succession planning. And the Government needs to consider whether, as in the case of the tobacco industry, it can be perceived as favouring tax revenues over the health of its people and its economy. However difficult it may consider the task, the option should be obvious. No company that is in such a business should be enjoying the lower of the two corporate tax rates, and its products should be subject to higher taxes and stronger enforcement.

In the interest of disclosure, I should state that I am a small shareholder in DDL. I have asked two brokers to help me dispose of my shares.