Introduction

Describing its 2012 performance as riding on the back of a growing economy, the Guyana Bank for Trade and Industry Limited (GBTI) will be holding its Annual General Meeting for 2012 at its Kingston Office on Monday June 10 at 6 pm. Most of the numbers continue a very favourable trend and shareholders would no doubt be happy with the 25th anniversary report although this event has not earned any mention in the 90-page report.

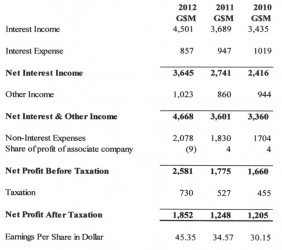

Total assets increased by 17% in 2012 over 2011 while total loans and advances for the year increased by 47%. On the other side of the balance sheet, total shareholders’ funds increased by 20% while deposits increased by 16%. Net income before taxes increased over 2011 by 22% while after tax income has increased by 31%. The comparable percentage for 2011 over 2010 was 15% in each case.

Total assets increased by 17% in 2012 over 2011 while total loans and advances for the year increased by 47%. On the other side of the balance sheet, total shareholders’ funds increased by 20% while deposits increased by 16%. Net income before taxes increased over 2011 by 22% while after tax income has increased by 31%. The comparable percentage for 2011 over 2010 was 15% in each case.

Income statement

Impressive as these figures are, a closer look suggests that a significant contributor to the bank’s performance is a simple strategy of controlling the rate of interest it pays on depositors’ funds. A winning strategy of any business is to control one’s expenditure and the bank has managed to do this exceptionally well by controlling the level of interest it pays on depositors’ funds. While over the period 2010 to 2012 deposits increased by 44%, the interest paid on those deposits declined by 16%. GBTI has consistently benefited from a huge pool of non-interest bearing demand deposits. At December 21, 2012 such deposits amounted to $19,825 million, representing 26% of total deposits, while at December 31, 2011 they amounted to $17,180 million, also 26% of total deposits. As a consequence the average rate of interest paid on deposits in 2012 was 1.2% compared with 1.6% in 2011.

Impressive as these figures are, a closer look suggests that a significant contributor to the bank’s performance is a simple strategy of controlling the rate of interest it pays on depositors’ funds. A winning strategy of any business is to control one’s expenditure and the bank has managed to do this exceptionally well by controlling the level of interest it pays on depositors’ funds. While over the period 2010 to 2012 deposits increased by 44%, the interest paid on those deposits declined by 16%. GBTI has consistently benefited from a huge pool of non-interest bearing demand deposits. At December 21, 2012 such deposits amounted to $19,825 million, representing 26% of total deposits, while at December 31, 2011 they amounted to $17,180 million, also 26% of total deposits. As a consequence the average rate of interest paid on deposits in 2012 was 1.2% compared with 1.6% in 2011.

This is in sharp contrast with the interest the bank charged for loans and advances. In both 2012 and 2011 the average interest rate earned on loans was 12%. The interest spread, measured crudely between the interest charged and the interest paid has therefore remained in double digits, no doubt a banker’s dream. It gets better since the bank also has significant earnings from Commissions and foreign exchange trading and gains. For several years, the income from these sources consistently exceeds employment costs – the bank’s next highest recurrent cost.

Taxation

Ignoring the deferred tax credit of $72 million (this is a timing difference, meaning that it will be payable some time later), leaves a corporation tax charge for the year of $801 million, an effective rate of 31%, compared with a nominal rate of 40%. The difference is mainly due to the substantial amount of income earned in 2012 ($390 million) that is exempt from corporation tax under a very generous tax regime designed to assist various social and other interest groups.

Balance sheet

Growth has been equally pronounced in the balance sheet with deposits increasing by close to 90% since 2008 while loans and advances have increased by 174% over the same period. As a result the loans to deposit ratio, an indicator of how the proceeds of the deposits are employed in interest-earning assets, has improved from 31% in 2008 to 46% in 2012, likely to be the highest ratio ever recorded by the bank.

Growth has been equally pronounced in the balance sheet with deposits increasing by close to 90% since 2008 while loans and advances have increased by 174% over the same period. As a result the loans to deposit ratio, an indicator of how the proceeds of the deposits are employed in interest-earning assets, has improved from 31% in 2008 to 46% in 2012, likely to be the highest ratio ever recorded by the bank.

One glitch in an otherwise well-presented and informative annual report is with respect to the distribution of loans as at December 31, 2012. There are two separate charts ‒ one on page 14 and another on page 17 ‒ with the same caption but containing significantly conflicting percentages. Accordingly it is not possible for any meaningful informed comment on the composition of this very important element of the bank’s operations.

Loans and advances which at the end of the year accounted for 40.3% of the bank’s total assets accounted for 64% of income earned during the year. On the other hand, investment securities comprising mainly Government of Guyana Treasury Bills ($9,548 million), Foreign Government securities ($6,141 million and Corporate Bonds ($4,294 million) and representing 24% of assets accounted for 15.6% of the bank’s income for the year.

Despite the significant increase on its loan portfolio the bank still had at cash resources of $23,070 million which includes $8,987 million in central bank reserve requirement and another $4,436 million surplus to such reserve requirement.

The net increase in shareholders’ funds referred to in the opening paragraph was made up of the net income for the year together with a gain arising on the revaluation gain on the investment portfolio and the share of comprehensive income of an associate company, less dividends of $520 million paid in 2012 in respect of 2011.

Dividends

Dividends paid and proposed for 2012 is $16 per share, a 45% increase over the $11 per share paid in 2011. Of the $16, an interim dividend of $5 per share was paid during 2012 leaving a further $11 per share to be paid, once approved by the shareholders. The full amount of $640 million will represent a pay-out of 35% of profits for the year but a mere fraction of the approximately $6.5 billion of the accumulated distributable profits.

Conclusion

The bank continues to show faith in bricks and mortar banking with branches in Lethem and Port Kaituma, a pioneer approach in Guyana even as it embraces electronic banking. The bank’s website offers its customers and the public information on the financial performance of the bank, through a series of quarterly financial indicators. This is a welcome development and the bank should honour its commitment to update the page soon after the end of every financial quarter. The most recent data are on quarter 2 of 2012.

These are halcyon days for the banking sector whose members outperform the rest of the economy, with the exception of gold mining companies. But there are challenges ahead: anti-money laundering legislation and the application of the US Foreign Account Tax Compliance Act of the USA are two challenges identified in the CEO’s report. As HSBC, the international bank recently saw, penalties can be severe – it was fined US$1.9 billion by the US regulator ‒ if anti-money laundering legislation is strictly applied. There may be other challenges as well, including changes in domestic tax rules and their application and the rice element of the PetroCaribe Agreement with Venezuela which is faced with shortages of basic items like toilet paper.

As the bank celebrates its 25th anniversary it may just wish to leave thoughts about those until after the shareholders’ meeting on June 10.