Youngest

Demerara Bank Limited (DBL) is one of the youngest commercial banks in Guyana. Though born in January 1992, DBL did not obtain a licence to conduct banking services until 1994. Less than 10 years later, the Guyana Stock Exchange (GSE) was established, and DBL became a participant on the exchange. As we come to the end of examining the individual banks that are part of the GSE and the Lucas Stock Index (LSI), DBL stands out in more ways than one. At the end of its financial year in 2013, DBL had assets valuing $49.8 billion and a capital base of $6.5 billion. Important to any commercial bank is its deposit base. DBL had a deposit base of $41.5 billion that grew 18 per cent over 2012 and by 12 per cent per annum over the last three years. Today, DBL has a market capitalization of nearly $14 billion making it the third largest bank of the four that are part of the LSI and the focus of this concluding series. This market value is more than twice the size of its book value and compares favourably with the other three banks that were already discussed.

Indigenous bank

From its profile, DBL looks like any regular bank going about its daily business of attracting the excess liquidity of customers and turning it into revenues as best as it can. Yet, DBL has the most interesting story to tell about the commercial banks discussed in this series. Of course, DBL loves to describe itself as the only indigenous bank in the country. Given the history of the other banks and the disappearance of the Guyana National Co-operative Bank, one cannot dispute that claim. DBL’s story is not only about its origins, its name and its logo, all of which possess value for a nation that has shifted from its mercantilist vision of economic independence to a more liberalist one and is straying further from its motto of ‘One People, One Nation, One Destiny.’ Neither is the story about the handsome growth in profits and the return on equity that it generated for its shareholders. The story is about the business strategy of the bank and how it is growing its deposits and how it goes about making money in a market where the demand for loans of good quality is limited. The story is also about how attached Guyana has become to the Venezuelan market as a result of the rice-for-oil deal under the PetroCaribe facility and how that is likely to impact the business strategy of DBL in the long-run.

Old fashioned

To repeat the story of DBL’s 2013 performance as the company tells it in its annual report, it would be necessary to observe the bank’s use of the old-fashioned yet productive way of doing business. In an aggressive attempt to win deposits, DBL employed door-to-door soliciting of customers and lobbying of businesses and government departments. DBL attributes its growth in deposits to this version of the prospecting sales strategy that has helped it to increase savings deposits by more than 16 per cent. This deposit mobilization strategy was employed mainly by the branches of the bank that were outside of Georgetown. It is not clear how many accounts the bank possesses, but one has to assume that the growth could also mean that the bank has brought new customers into the banking environment.

Long-term maturities

An interesting component of the bank’s business strategy is the distribution of deposits between short-term and long-term maturities. While the other three banks in this series held in excess of 90 per cent of deposits with maturities of less than one year in some cases, DBL bucked the trend over the last four years and held an average of 25 per cent of deposits with maturities of more than one year. At one stage, DBL held as much as 39 per cent of its deposits in long-term maturities. It was the clearest attempt by any bank to use financial leverage to its fullest and as part of its long-term financing strategy.

An interesting component of the bank’s business strategy is the distribution of deposits between short-term and long-term maturities. While the other three banks in this series held in excess of 90 per cent of deposits with maturities of less than one year in some cases, DBL bucked the trend over the last four years and held an average of 25 per cent of deposits with maturities of more than one year. At one stage, DBL held as much as 39 per cent of its deposits in long-term maturities. It was the clearest attempt by any bank to use financial leverage to its fullest and as part of its long-term financing strategy.

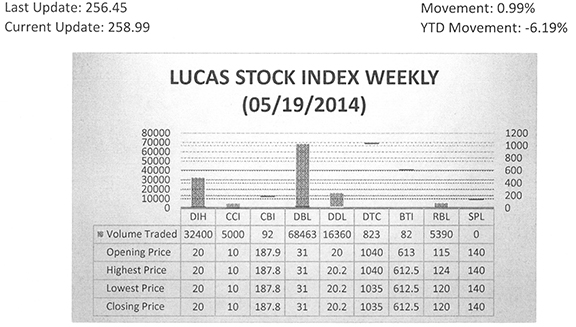

The Lucas Stock Index (LSI) rose 0.99 percent during the third period of trading in May 2014. The stocks of eight companies were traded with a total of 128,610 shares changing hands. There were two Climbers and three Tumblers. The value of the stocks of Demerara Distillers Limited rose 1 percent on the sale of 16,360 shares while the value of the stocks of Republic Bank Limited (RBL) rose 4.35 percent on the sale of 5,390 shares. The value of the stocks of Citizens Bank Inc fell 0.05 percent on the sale of 92 shares while the value of the stocks Demerara Tobacco Company (DTC) fell 0.48 percent on the sale of 823 shares. The value of the stocks of Guyana Bank for Trade and Industry (BTI) also declined 0.08 percent on the sale of 82 shares. In the meanwhile, the value of the stocks of Banks DIH (DIH), Caribbean Container Inc (CCI) and Demerara Bank Limited (DBL) remained unchanged on the sale of 32,400; 5,000 and 68,463 shares respectively.

Indeed, the longer term maturities actually provide DBL with flexibility in composing its income-generating portfolio. The $39 billion in assets that DBL ended up with at the end of 2013 does not follow the conservative profile of the banking industry in Guyana. Like all the other banks, the principal income-generating assets of DBL are the investments that it makes and the loans and advances that are created by customer demand. In putting the portfolio into perspective, two things are noticeable. One, for all practical purposes, DBL does not have short-term investments. Its principal short-term investments consist of Treasury Bills, short-term bank deposits and the interest accruing on the investments. Even though these investments are classified as available-for-sale, their liquidity risk is minimal and the likelihood of the value of the securities being altered by changes in the interest rate is very low. In essence, the investments could be seen as being equivalent to cash.

Investments

The second thing noticeable about DBL is that its advances are smaller than its investments. This is especially true about its long-term income-generating assets where long-term investments are greater than long-term loans and advances. In the case of all the other banks, long-term advances outstrip long-term investments. Based on the discussion of the credit quality of its financial assets found in its annual report, DBL reveals that the investments comprise corporate bonds. On closer examination then, the investments of DBL are really loans, except that the loans are made to foreign corporations through the issue of bonds by those corporations. Bonds are often seen as safe investments by jittery investors. The added benefit of holding bonds is that they provide a steady stream of income.

Despite the relative security of the bond, the trade-off between loans and investments for the security of steady returns from the bonds is real. The bank gives up the holding of collateral that would come with a domestic loan in favour of a foreign loan that comes without collateral. So, unlike the other commercial banks in Guyana, DBL has projected itself as a bold risk-taker where it is willing to earn higher returns by waiting a little longer to recover money that it has parted with without the guarantee of collateral. The more cynical might even go so far as to say that DBL trusts the foreign social and economic conditions more than it trusts the domestic economic conditions. That is not a far-fetched viewpoint since the Chief Executive Officer notes in the 2013 Annual Report “[t]here is an apparent slowdown in the economy on account of uncertain political environment and deteriorating law and order situation in Guyana.”

Clear conviction

With the clear conviction that there is trouble in the domestic economic space, the issue that comes to mind is how efficient the assets have been in bringing in the profits that DBL enjoys. Their deployment in both the domestic and foreign markets is expected to have differing impacts on the company. Collectively, the efficiency of the assets, as measured by asset turnover, has remained stable at six per cent per annum over the last three years. From this measure of the performance of the assets, one thing is clear: DBL has been able to maintain a consistent relationship between the financing provided by its customers and the utilization of the economic resources under its control. On average, the foreign investment has been more efficient than the local assets and has generated more revenue than the local investment. Over the last three years, foreign investment brought in more than eight cents on every dollar as against loans and advances which brought in an average of six cents on every dollar per annum.

The marginal revenues shed a different light on the contribution of the growing asset portfolio of the bank and call into question its sales optimization strategy. The issue arises because the extra revenues brought in by the employment of additional assets do not bear the same results as the asset turnover. Marginal revenues have declined from a high of 13 per cent or 13 cents on every additional dollar to four per cent or four cents on every additional dollar employed over the last three years. The movement is particularly noticeable on the foreign investment which marginal revenue moved from three per cent in 2011 to 19 per cent in 2012 and back down to less than two per cent in 2013.

Rethink

The highly variable nature of the marginal revenues might induce DBL to rethink its investment strategy. No one knows with certainty what the leaders of the bank would do, but even in a provocative geopolitical environment, one cannot help noticing the allure of the expanding revenues of rice farmers and millers as a result of the PetroCaribe arrangement. While the deal has brought a measure of stability to rice production and distribution, DBL remains apprehensive about the sustainability of the facility. Yet, DBL has committed itself to strengthening its support for agriculture. This commitment could come to fruition since the management of DBL remains firmly in control of the resources of the organization.