Head Down

The Guyana economy has entered the last quarter of 2014 and the local stock market continues to languish below its closing value of December 2013. The stock exchange reports market capitalization (cap) or the weighted price of the stocks of all companies in the exchange at the end of every month. And, as at the end of September, the market value of the companies on the exchange was reported to be G$155 billion. At that level, the market value of the stocks traded on the Guyana Stock Exchange (GSE) was down about four percent from the G$161 billion at which it was at the end of December last year. It means that the exchange headed into the last trading quarter with its head down and repeated the experience of other years when the index found itself starting the final quarter of the year below investors’ expectations. When measured against gross domestic ![]() product (GDP) of 2013, the current value of the companies in the exchange represents about 20 percent of the output of goods and services. As could be expected, this market-based measure of stock performance mimics the behaviour of the underlying stocks and is down slightly from the 21 percent share with which it ended 2013.

product (GDP) of 2013, the current value of the companies in the exchange represents about 20 percent of the output of goods and services. As could be expected, this market-based measure of stock performance mimics the behaviour of the underlying stocks and is down slightly from the 21 percent share with which it ended 2013.

Immeasurable Help

Very few people think highly of the GSE because of the small number of companies on the exchange and the limited trading activity that takes place each week after more than 10 years in operation. Despite its weaknesses, having the data of the stock exchange is of immeasurable help in understanding the structure and behaviour of the Guyana economy. The information which could be extracted from the exchange enables one to circumvent the control of information by the government and gain valuable insights into the behaviour of the Guyana economy. As such, the stock exchange makes it possible to see evidence of realistic trends in the Guyana economy long before government disclosures and better than the historical data of government can do.

Market Cap to GDP

The metric that serves this purpose is the ratio of market cap to gross domestic product (GDP). With the use of this ratio, it is possible to garner a wealth of information about the business sector and show the aggregate level of activity of the firms that are publicly traded in the economy. It exposes the way Guyanese prefer to do business in the country. The importance of the market cap to GDP ratio lies in what it says also about the development of the equity market in Guyana and, when observed over time, provides clues to changes in the economy as a whole.

The ratio of market cap to GDP is captured in the graph below. The relationship between these two variables indicates that the level of activity of the companies participating in the stock exchange grew from 15 to over 20 percent over the last 10 years. If one was to view GDP as total earnings (output of all entities times price) and the market cap as the weighted price of the shares, then the market cap to GDP ratio is equivalent to a price-earnings ratio for the entire country. For the publicly-traded companies, the P-E ratio is below one. This observation suggests that the stocks on the GSE are undervalued.

Some Caution

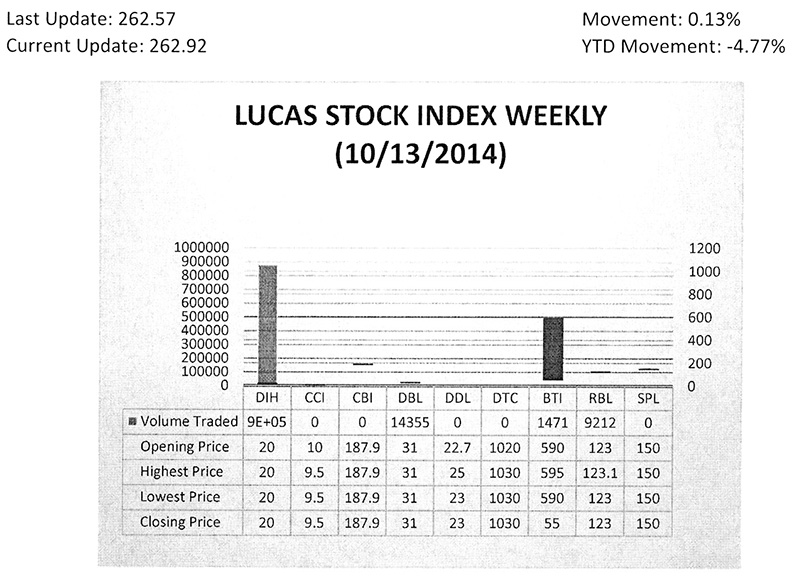

The Lucas Stock Index (LSI) rose 0.13 percent in trading during the second period of October 2014. The stocks of four companies were traded with 902,382 shares changing hands. There was one Climber and no Tumblers. The value of the stocks of Guyana Bank for Trade and Industry (BTI) rose 0.85 percent on the trade of 1,471 shares. In the meanwhile, the value of the shares of Banks DIH (DIH), Demerara Bank Limited (DBL) and Republic Bank Limited remained unchanged on the sale of 877,344; 14,355 and 9,212 shares respectively.

One has got to take that conclusion with some caution. A check of the Lucas Stock Index (LSI) reveals that half of the stocks are from the manufacturing sector and the other half is from the financial services sector. A narrower focus of the relationship between market value and sectoral GDP helps to provide a clearer valuation picture of stocks in the manufacturing and financial services sectors. The valuation of the manufacturing companies to manufacturing’s share of GDP therefore reveals a different story. When market cap is measured against sectoral GDP, the manufacturing companies in the index are valued at more than twice the market’s average. However, at 105 percent of the sector’s contribution to GDP, the stocks of the manufacturing sector appear to have the appropriate valuation. When one considers that rice and sugar make up about 40 percent of the manufacturing sector, the valuation changes radically, and leads one to believe that the stocks of the manufacturing sector could be overvalued when the government’s contribution is omitted from GDP. The financial institutions in the index are three times larger than their sectoral GDP. At 227 percent above sectoral GDP, the stocks of the financial companies in the index appear to be significantly overvalued.

Disturbances

The graph above also points out what happens to the economic contribution of these companies when there are disturbances to the economy. With their contribution above the trend line in 2004 and 2005, it appears that the output of these companies was insulated from the adverse effects of the floods of 2005. Their slippage below the line from 2006 to 2011 could be a combination of the delayed effects of the floods, the rebasing of the economy which increased the number of measured sectors, high oil prices and the rising influence of the mining sector on account of the prolonged boom in gold prices. It also indicated that the publicly-traded companies were not significant drivers of the economy. At an average contribution of 12 percent from 2006 to 2011, the other economic sectors of the economy were contributing 88 percent of output. Those were the years when commodity prices showed an upward trend with gold prices in particular soaring to near record levels. They were also good years for the construction and the wholesale and retail industries.

But the contribution of publicly-traded companies returned above the trend line in 2012 and moved much higher in 2013 signifying that the factors that were driving the rest of the economy have begun to cool off. So despite the record declaration of gold in 2013, its contribution to the economy relative to other economic activities was beginning to wane. With publicly-traded companies contributing 21 percent of output in 2013, it means that the rest of the economic agents are contributing a much lower share-79 percent-to GDP.

Feebleness of

Small Businesses

The distribution of the economic output observed above reflects also that the Guyana economy is badly in need of restructuring. Considering that the companies in the Lucas Stock Index account for 97 percent of the value of the stock market, it means that the nine companies in the index are responsible for about 21 percent of the level of economic activity in Guyana. Professor Clive Thomas in a 13 July 2014 article in Stabroek News estimated that government activity accounts for about 66 percent of domestic economic activity. This leaves foreign investors, privately-held businesses and small and medium sized enterprises contributing a mere 13 percent to the economy. This additional observation dispels the notion that foreign investment currently plays a major role in the Guyana economy and underscores the feebleness of the small business sector.

Preference of Guyanese

Another benefit derived from utilizing the market cap to GDP ratio is that it reveals the preference that Guyanese have for the unincorporated or privately-held legal business form. The legal, financial and reporting obligations of a publicly-traded company might be discouraging Guyanese from bringing other companies onto the stock market. Guyanese it would seem prefer to operate in private markets than in the publicly listed markets. Further, only two participants in the market are foreign owned, suggesting that foreign companies are not attracted to the local stock market.

In addition, the current trend in the stock market signals a continued preference by stock market participants for internal equity financing to external equity financing and bank lending. Other investors are not taking advantage of the stock market to raise equity capital either. As such, the decline in value in October further suggests that people continue to look elsewhere to obtain money to invest in their businesses.