Types of investment

There are generally two types of investment: direct investment and portfolio investment. Direct investment involves starting a business where the investor deals directly with the customer. Whether the investor decides to set up a tray at the side of the road, open a store front at the bottom of the house in which he or she lives or rent space in one of those high rise complexes around town to carry on a trade or business, the investor has gotten involved in direct investment. In some instances, the investor might buy enough interest in an existing business to gain control or influence over future decisions of that business.

That too represents direct investment. Under those conditions, the investor is part owner of the business and any profits or losses that it makes are his or hers to enjoy or to bear. Not everyone is interested in direct investment and those persons look for other means by which to invest their money. The option available to them is called portfolio investment. The word portfolio is used because it implies that there can be different classes of assets which all could be stuffed, figuratively speaking, into one folder or portfolio. The focus of this article is on portfolio investment.

Classes of assets

Portfolio investment tends to involve three classes of assets. These assets are (1) capital assets; (2) store of value assets; and (3) consumable assets. When brought together, they help to provide balance to the investment strategy and a hedge against the risk that might be associated with it. A comparison of the three asset classes would reveal that the capital assets produce a steady stream of income while the other two do not. This distinction among the three asset classes is fundamental since capital assets impact the rate of wealth creation and their performance often reflects the economic development within a country.

Portfolio investment tends to involve three classes of assets. These assets are (1) capital assets; (2) store of value assets; and (3) consumable assets. When brought together, they help to provide balance to the investment strategy and a hedge against the risk that might be associated with it. A comparison of the three asset classes would reveal that the capital assets produce a steady stream of income while the other two do not. This distinction among the three asset classes is fundamental since capital assets impact the rate of wealth creation and their performance often reflects the economic development within a country.

The asset class of interest to this discussion is the capital assets.

Some items of capital assets are stocks, bonds, treasury bills, bankers’ acceptance, commercial paper, certificates of deposit, bills of exchange, and repurchase agreements (Repos). Treasury Bills, commercial paper, Bankers Acceptance, Bills of Exchange, Repos and CDs with short maturities are short-term assets that are sold and purchased in what is referred to as the money market. Things like stocks, Treasury Notes and Treasury Bonds are regarded as long-term assets and are traded in the capital market. The term capital market is used often to cover both the short-term and long-term financial markets.

Households

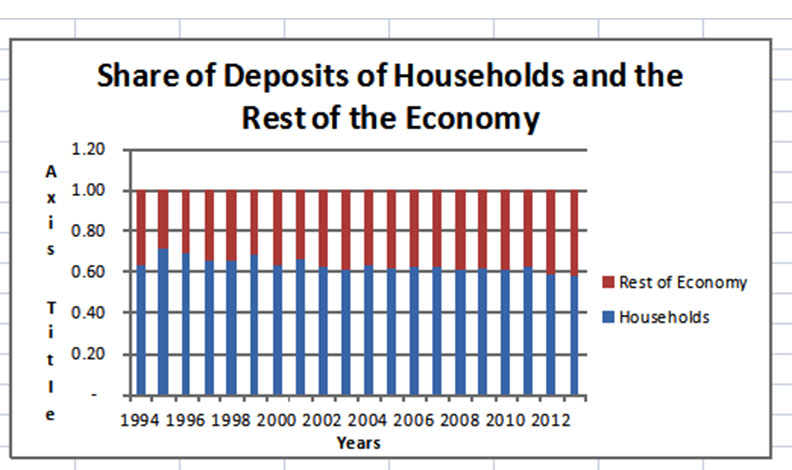

The money to invest in the aforementioned instruments comes primarily from households. Money which is saved becomes available for investment. This savings could be reflected in bank deposits, market capitalization of equity shares or in the value of other financial claims such as outstanding value of bonds, treasury bills, mutual funds and the like. The principal way in which Guyanese save is in the savings programmes of the commercial banks. The graph below shows the percentage share of deposits of households and the other economic agents of the economy that are in the commercial banks in Guyana. From 1994 to 2013, households accounted for an average of 63 per cent of all deposits in the banking system.

Figure 1

The opportunities to engage in portfolio investment come from private businesses and from government which borrow the money to start or expand businesses or to finance development projects. Consequently, there needs to be a very dynamic and growing private sector and a very active development programme of the government for investment opportunities. The Guyana economy has exhibited steady growth for the last six years. This growth has been accompanied by an average five percent growth in direct investments. But portfolio investment by households is virtually non-existent.

Indirect investors

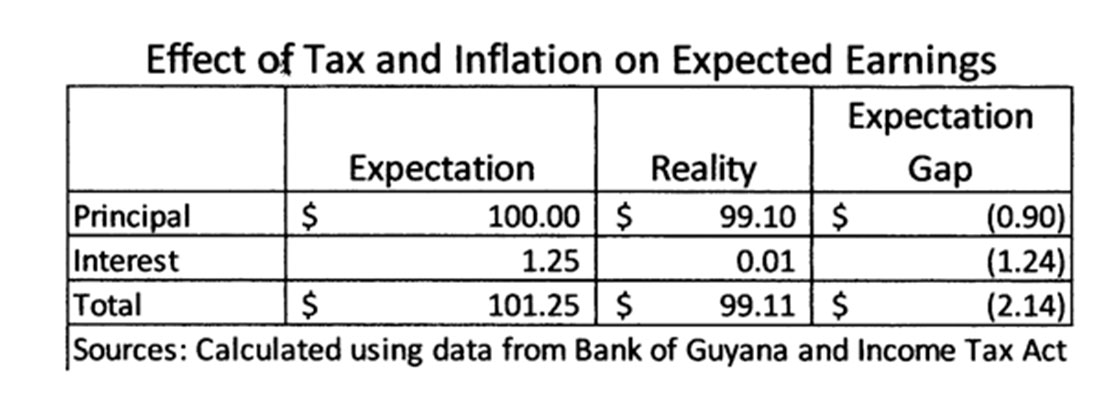

This is an interesting state of affairs considering what is happening to the money held by Guyanese who participate as indirect investors of the commercial banks. Guyanese receive a rate of interest of 1.25 per cent which as at September 2014 represented 13.64 per cent of the income earned by the commercial banks. In real terms, Guyanese might be taking one step forward and two steps backwards without portfolio investment as could be seen from the table below.

Table 1

The table reveals that at the end of one year, Guyanese lose 90 cents on every $100 in the bank as a result of inflation which sits at 0.9 per cent according to currently available data. Interest suffers from the effects of the withholding tax and inflation leaving Guyanese virtually giving up all the interest that they earned. It is not enough for Guyanese to have to rely on insurance policies and pension plans which are managed by third parties as well. If the situation does not change, people’s future will remain uncertain and the attempts to fill the income gap from criminal acts will continue.

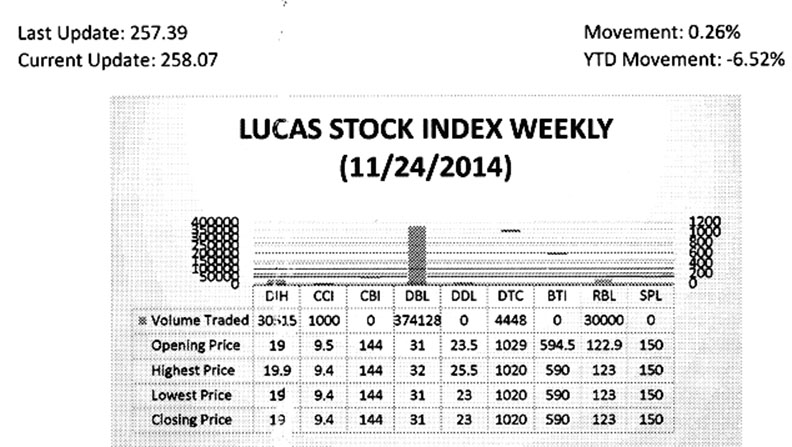

The Lucas Stock Index (LSI) rose 0.26 per cent in trading during the fourth period of November 2014. The stocks of five companies were traded with 440,091 shares changing hands. There were two Climbers and one Tumbler. The value of the stocks of Republic Bank Limited (RBL) rose 0.81 percent on the sale of 30,000 shares while the value of the stocks of Demerara Tobacco Company (DTC) rose 0.48 percent on the sale of 4,448 shares. The value of the stocks of Caribbean Container Incorporated (CCI) fell 1.05 percent on the sale of 1,000 shares. In the meanwhile, the value of the stocks of Banks DIH (DIH) and Demerara Bank Limited (DBL) remained unchanged on the sale of 30,515 and 374,128 shares respectively.

Opportunity for change

The opportunity for change comes with opportunities for portfolio investment. But this opportunity does not exist currently. With the exception of stocks, none of the capital assets are available on a secondary market in Guyana and the government has no programme to facilitate such saving. It is quite possible that trading of financial claims of the aforementioned types might be taking place in an unregulated over-the-counter market but that would not count since such trades lack transparency and objective market valuation. Also, the opportunity is not available to everyone because such trades tend to be very private and if it is taking place would be kept among a small group of investors. Whether that is true or not, there is clearly a need for greater portfolio investment in Guyana. Even the commercial banks are frustrated by the relatively limited investment opportunities in Guyana. According to data from the Bank of Guyana, the commercial banks were only able to use about 56 per cent of the deposits that they held as at September of this year.

Reason

Part of the reason lies in the economic structure of the country which is not opening enough space for direct investment and is not facilitating competition. The unhealthy political climate cannot be discounted from consideration too. The conditions are worse for portfolio investment. The institutional and legal framework to facilitate portfolio investment appears not to be in place. Treasury bills, bills of exchange and bankers’ acceptance are instruments that are available and could be traded on the money market. They however have no organized secondary market which could facilitate trade in such instruments.