Dear Editor,

It has been reported that the Chairman of GuySuCo, Dr Clive Thomas, is proposing a solution to the crisis in the sugar industry. His proposal (KN article of August1) is as follows: “… we can save the industry from further problems if we scale down production. Sugar would be profitable if we focus on the domestic market as well as the Caribbean. We have some protection in the Caribbean due to Caricom. We also have some protection within the European market but that is only up to 2017. I hope the commission agrees with my position. I don’t see a difference with regard to it.”

While I agree most of the time with Professor Thomas’s work and findings, I do not agree with his recommendations on the way forward for GuySuCo. Specifically, targeting the domestic and Caribbean markets due to Caricom preferences is not a feasible strategy, largely because consumers will be forced to buy a basic commodity produced by an inefficient and high cost GuySuCo. The question, therefore, is: Why ask consumers in Guyana and the Caribbean to pay 40 US cents for sugar that they can purchase for 11 cents? This expensive product would be hard to sell to Caribbean consumers and Caribbean political leaders, while the black market for sugar in Guyana will become a new pathway for spawning corruption since enforcement to stop sugar smuggling would be difficult. Clearly, the previous experience in smuggling should not be forgotten as it resulted in many distortions in the social and economic life of Guyanese when in the past wheaten flour was the smuggled commodity. Sugar under these conditions will be no different than flour, where sugar prices in neighbouring countries would be significantly lower than in Guyana, and trade and arbitrage opportunities with some risk would be operable. Consequently, it would be cheaper to import sugar than to produce sugar under this inefficient technology that could potentially spawn social and economic dislocations.

While I agree most of the time with Professor Thomas’s work and findings, I do not agree with his recommendations on the way forward for GuySuCo. Specifically, targeting the domestic and Caribbean markets due to Caricom preferences is not a feasible strategy, largely because consumers will be forced to buy a basic commodity produced by an inefficient and high cost GuySuCo. The question, therefore, is: Why ask consumers in Guyana and the Caribbean to pay 40 US cents for sugar that they can purchase for 11 cents? This expensive product would be hard to sell to Caribbean consumers and Caribbean political leaders, while the black market for sugar in Guyana will become a new pathway for spawning corruption since enforcement to stop sugar smuggling would be difficult. Clearly, the previous experience in smuggling should not be forgotten as it resulted in many distortions in the social and economic life of Guyanese when in the past wheaten flour was the smuggled commodity. Sugar under these conditions will be no different than flour, where sugar prices in neighbouring countries would be significantly lower than in Guyana, and trade and arbitrage opportunities with some risk would be operable. Consequently, it would be cheaper to import sugar than to produce sugar under this inefficient technology that could potentially spawn social and economic dislocations.

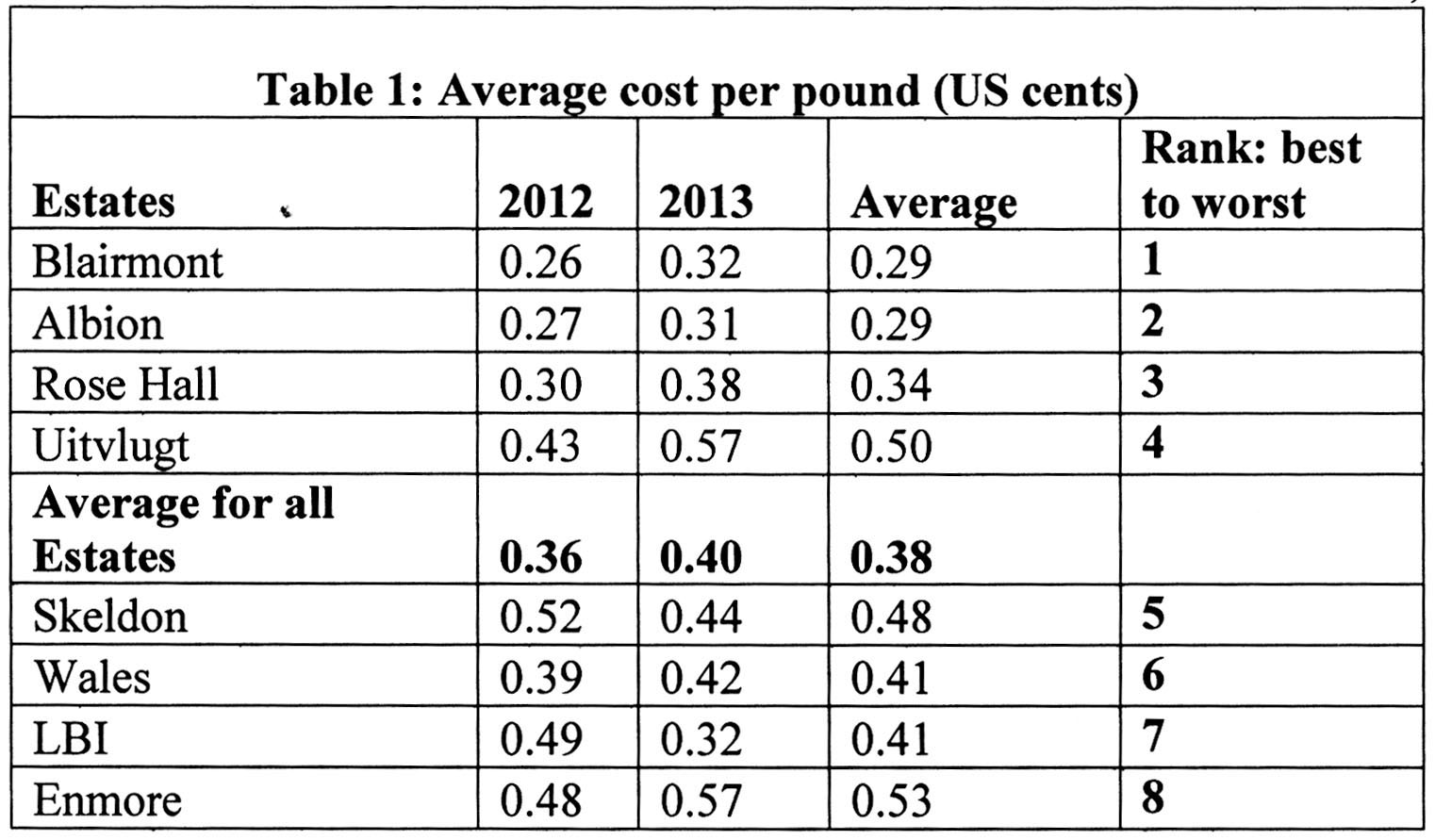

In sugar production, the most critical technology problem is the low yield of sugar cane per acre which cannot be significantly increased without serious changes in the agronomic, optimal ratoon practices, and factory efficiencies in GuySuCo. This agriculture problem will take several years to solve and no serious improvement in yields through enhanced productivity can be expected in the short term. When the on-farm production (sugar cane per acre) and factory processing (sugar cane to sugar) are combined, the average cost per pound has been estimated at US 40 cents per pound. In this regard, evidence suggests that estates with the least cost per pound of sugar in 2012 are Blairmont and Albion, estimated at 26 and 27 US cents, respectively, while the high cost producers are LBI and Skeldon at 48 and 52 US cents, respectively (Table 1).

In sugar production, the most critical technology problem is the low yield of sugar cane per acre which cannot be significantly increased without serious changes in the agronomic, optimal ratoon practices, and factory efficiencies in GuySuCo. This agriculture problem will take several years to solve and no serious improvement in yields through enhanced productivity can be expected in the short term. When the on-farm production (sugar cane per acre) and factory processing (sugar cane to sugar) are combined, the average cost per pound has been estimated at US 40 cents per pound. In this regard, evidence suggests that estates with the least cost per pound of sugar in 2012 are Blairmont and Albion, estimated at 26 and 27 US cents, respectively, while the high cost producers are LBI and Skeldon at 48 and 52 US cents, respectively (Table 1).

Comparing the cost between 2012 and 2013, the data confirm that costs are increasing over time for all estates, except Skeldon, which is not accurate, given the more recent information on the non-performance of the new Chinese factory. What also can be gleaned from Table 1 is the wide variability in costs, which ranges from 26 cents in Blairmont in 2012 to more than twice that amount at Enmore in 2013 at 57 cents. This is indeed a serious problem showing the inconsistency in the technology across the estates that generate costs that are way above the average world price of 11 US cents per pound, with our best estates, Blairmont and Albion, still not being competitive performers at world standards. The main implication that can be drawn from this analysis is that the sugar industry is not profitable, and unless significant changes are made across the industry to reverse these losses, taxpayers will forever be saddled with massive transfer to an activity that misuses scarce resources that can be better deployed elsewhere.

In particular, using an average European Union (EU) price of US 16 cents per pound and an average cost of US 40 cents per pound, this implies that whenever a pound of sugar is sold, GuySuCo will absorb a loss of 24 US cents per pound and GuySuCo will not be able to pay all its bills, unless significant transfers of taxpayer dollars are promptly disbursed from the Ministry of Finance; or arrangements are hurriedly made to sell the assets of GuySuCo in a fire sale. The last experience of this disaster was the sale of the cogeneration plant at Skeldon and sale of lands at giveaway prices. This has been the pattern for the last few years, aimed at relaxing cash-flow problems, minimizing industrial and union unrest, and curtailing government embarrassment, especially at election time.

Additionally, with no serious work being undertaken on agronomy concerns, along with a likely downsized research component, there will not be a technological breakthrough in the near term; even as financial and economic viability objectives by management are continuously overshadowed by excessive wage demands by aggressive unions that intimidate the government with industrial unrest and political abandonment at election time.

Because GuySuCo has no control over the selling price in the world markets, cutting the average variable cost of production by increasing yields is the only path that can lead to the profitability of GuySuCo. So the question is how much should the cut in average cost per pound be in order for GuySuCo to become financially viable? The answer: Imposing a cost cut of 60 per cent on an average cost of 40 US cents implies that the average variable cost of production and the world price would be the same at US16 cents; and any cut in cost above 60 per cent will signal the decision to begin economic production, where a zero profit level can then be established for a given level of fixed costs in GuySuCo. It should be noted, however, that cutting costs to the level suggested would involve mainly cutting employment/labour costs, since labour costs are more than 60 percent of total cost and other cost cutting in other areas would be insignificant in enhancing profitability. Evidence suggests, however, that downsizing labour will be a huge political problem that will not be an easy sell for the political leadership, since this has been the bind in the past where wage incentive payments are made, even when GuySuCo has been making losses. Alternatively, only new high yielding varieties, along with an optimal ratoon and fallow crop system that facilitate improved labour and capital productivity across GuySuCo, will make the difference in lowering costs to an average cost per pound of US$0.06. This will establish a breakeven level of output that is reasonable and attainable. Currently, none of the estates are within reach of this target.

So what is the way forward for GuySuCo? In response to this question, the answer covers a range of issues as follows:

Update Table 1 (2014-2015) and rank the estates to ascertain the most efficient ones; make a decision to keep the three least cost estates to form a new company; diversify the others into other activities (see below).

In order to clean up the GuySuCo balance sheet, government has to take over the debt of GuySuCo (G$58 billion and counting); and provide new capital for a new sugar company that only includes the three top estates. The new capital in a new company will have to be geared to satisfying working capital needs, fixed investment, marketing and research. The new technology must consider generating energy from sugar-cane waste; producing ethanol; selling top grade molasses for the health food markets internationally; making alcohol from sugar for export; and the use of the canals in the flood-fallow acreage to experiment with fish production and plants such as water lilies for export/energy (?). Consideration for foreign investors must be explored. If the new company is not economically viable in 5-8 years, the decision must be made to close operations as continuing this sugar operation will require subsidies from the treasury.

The workforce will have to be downsized to match the new company needs, while the government will have to consider severance pay for the workers sent home. Part of the severance pay could be in the form of land given from the estates or elsewhere or it could be in cash payments over time.

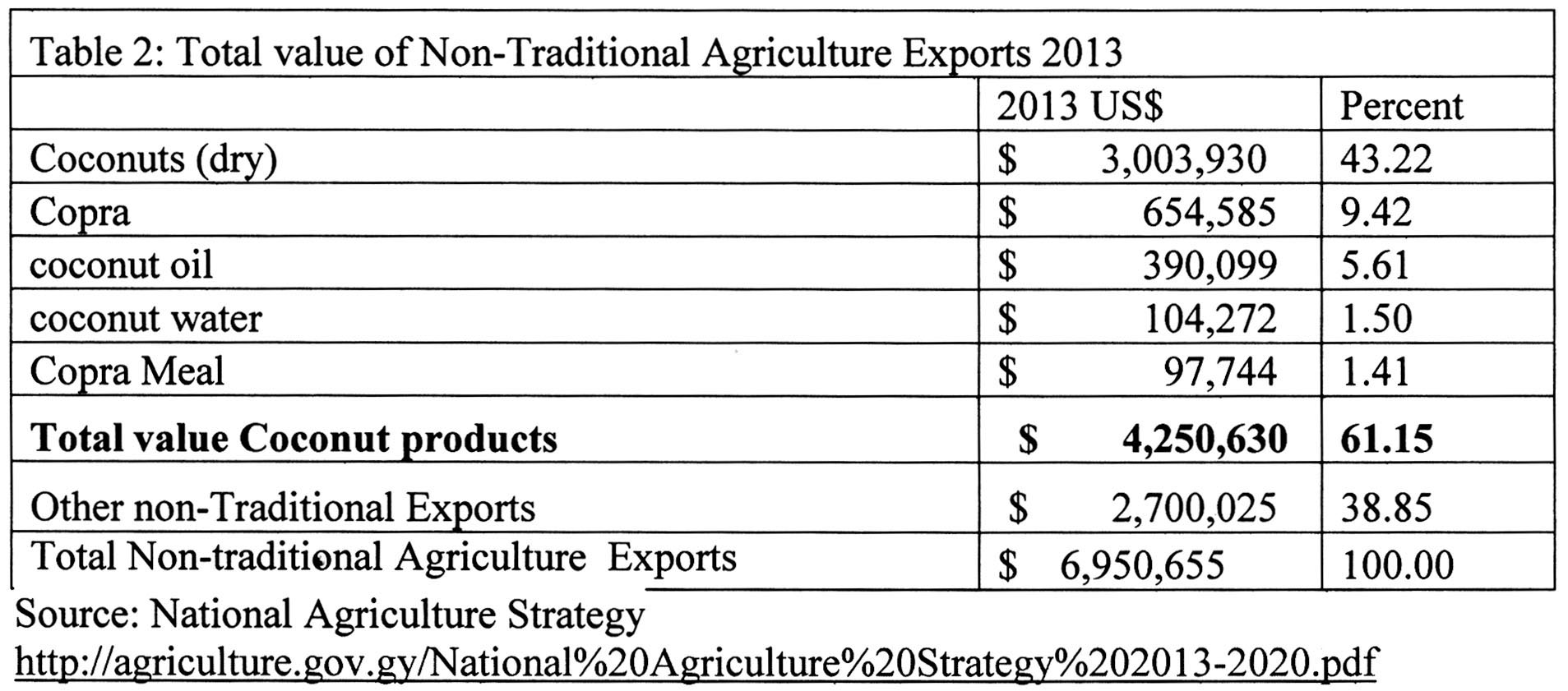

On one estate, a feasibility study should be conducted to examine coconut production on a large scale. There should be processing of the coconuts to produce a wide range of consumer and other products for exports. There may be a need to have imported expertise and investors (Brazil, India, Malaysia, and Mexico, others). Interestingly, Guyana export data for non-traditional export crops show that coconuts in all forms earned US$4.3 million out of total non-traditional exports of US6.95 million, accounting for 61 per cent of total non-traditional exports (Table 2). Coconuts are being used in a growing list of products that include food, skin, hair, and jewellery products, among others (see http://coconutboard.nic.in/dynamic/dirinfo/frmlistproducts.aspx?id=listprod)

On one estate in Demerara, there is need for a large dairy project; a feasibility study should be arranged. The demand for milk and milk products is significant in the domestic market. Imports are significant and can be replaced by local production. The potential for spin-off industries is significant. There is a need for expertise and investors.

On one estate, there should be a feasibility study to explore fresh fruits and vegetables (pineapples, peppers, among others) production. The interesting feature here is that due to changing health concerns and changing dietary needs, worldwide, fruits and vegetables are in high demand and are being placed on menus and are being consumed in increasing volumes at breakfast, lunch and dinner tables more than sugar, which has seen declining importance in consumer consumption and spending.

Seek funding to conduct a large scale fish and shrimp farming feasibility study on one of the estates; this project must consider exporting the product. There is a need for investors. The benefits per acre would more than likely be larger than what is earned from sugar or rice. Fish farming has been recently suggested by Mr Tony Vieira and should be explored.

Sugar cane and sugar production have been associated with Guyana for a very long time, the history of which has not been complimentary for a number of obvious reasons that need not be repeated here. More recently, the loss of preferential markets, increasing losses and government subsidies to keep the business open, declining world market prices due to expanding cane-sugar substitutes, and changing consumer tastes have made this industry financially unsustainable for a marginal producer such as Guyana. More destabilizing is the notion that Guyana is a price taker in world markets, where its production and exports account for less than one per cent of world trade, but in the past contributed significantly to foreign exchange earnings. This contribution to foreign exchange earnings is not likely to return and since the functioning of GuySuCo is not likely to change in a positive way under existing technology, policy-makers must make the decision to downsize and diversify out of sugar-cane production, for sugar-cane lands in Guyana must be used for more profitable activities.

Yours faithfully,

C Kenrick Hunte