Mr Jagdeo has been blamed recently by government officials and supporters alike for instigating a capital strike. The argument goes that Mr Jagdeo has immense powers in the private sector such that his business associates and friends have curtailed their investment since the new government came into power in 2015. No doubt the former President has many friends among the investor class. He spent years moulding his new private sector that sometimes crowded out parts of the older one. Indeed, these columns and my academic research have labelled his regime as an elected oligarchy.

This is not meant to diminish his economic accomplishments. There were. But these have to be seen within a broader picture of human development. I will certainly address Jagdeoian economic policy in a coming essay. As these essays have outlined numerous times, a private-public  approach – such as the Jagdeoian way – has to be based on credibility and legality so as to minimize the perception of corruption in a much divided society. It is for these reasons we cannot lift the Singaporean, Taiwanese or South Korean experiences (but we can seek insights from them) and plant them right into Guyana. Guyanese industrial policies have to be underpinned by a reorganized meritocratic and independent state bureaucracy and major constitutional change, since private incentives and markets alone cannot get the job done. Otherwise, at best we will rotate elected oligarchies once there continues to be free and fair elections.

approach – such as the Jagdeoian way – has to be based on credibility and legality so as to minimize the perception of corruption in a much divided society. It is for these reasons we cannot lift the Singaporean, Taiwanese or South Korean experiences (but we can seek insights from them) and plant them right into Guyana. Guyanese industrial policies have to be underpinned by a reorganized meritocratic and independent state bureaucracy and major constitutional change, since private incentives and markets alone cannot get the job done. Otherwise, at best we will rotate elected oligarchies once there continues to be free and fair elections.

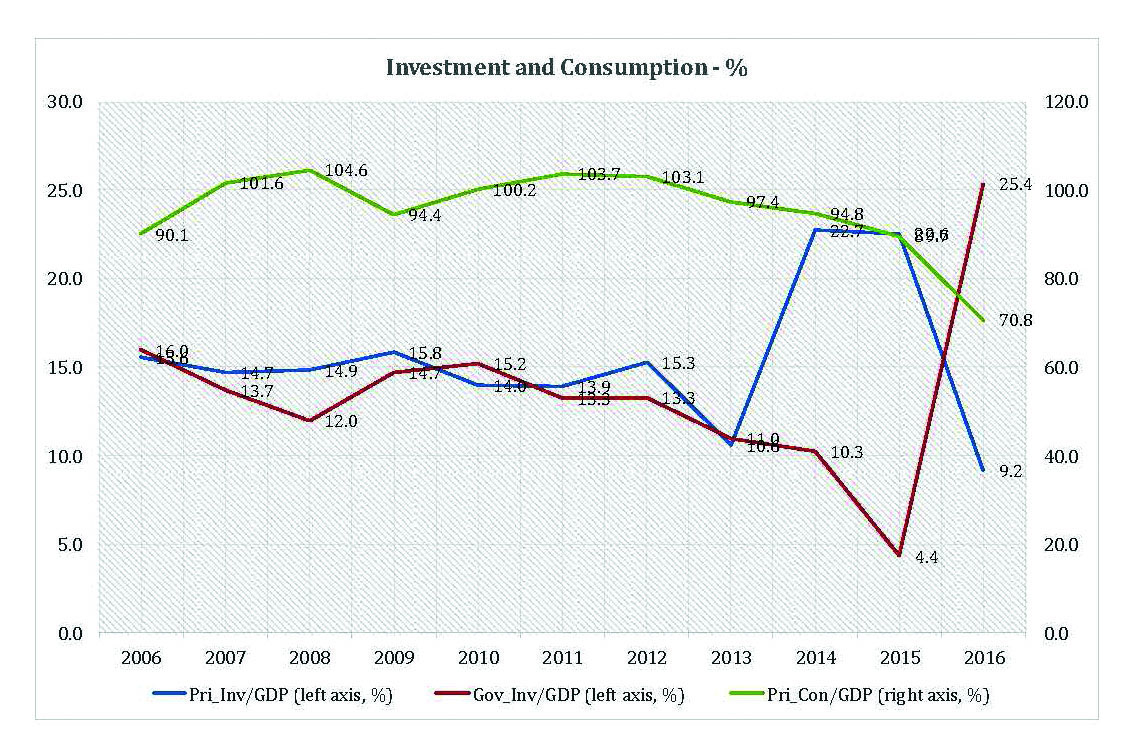

Can we find suggestive trends that rule out the possibility that the former President instigated a capital strike? We have to take a look at the trends in private investment, private consumption and government capital investment. We cannot just look at billions of Guyana dollar of these three variables since their increase over time would include inflation. Therefore, we will express everything as a percent of GDP, so as to expunge the inflationary effect.

The chart shows that private investment as a percent of GDP collapsed in 2016 to 9.2% from 22.6% in 2015. That is a precipitous decline in private investment that some may present as evidence of the capital strike (the Jagdeo shock). From 2006 to 2013, private investment was pretty flat averaging 14.3% over this period. However, it jumped in 2014 and 2015 to 22.6% owing to mining and extraction investments. Therefore, the 9.2% in 2016 falls about five percentage points below the long-term average from 2006 to 2013. Is Mr Jagdeo responsible for this five percentage point decline?

Businesses, however, respond to aggregate consumer demand (household demand). The trend of total consumer demand in the Guyanese economy over 2006 to 2016 is illustrated by the green line, which is graphed on the right axis and labeled Pri_Con/GDP. Over the said period, household consumption reached a peak of 103.7% of GDP in 2011. This represents consumption of both imported and Guyanese made goods and services. Consumption fell marginally to 103.1% in 2012, but subsequently declined significantly to reach 70.8% of GDP in 2016. We can see once more that the years 2011 and 2012 come into play as in the last two columns. Households started to curtail consumption since during the PPP time. Therefore, it should be no surprise that by 2015 and 2016 businesses would start cutting investments. A series of political shocks after the 2011 General election most likely accounted for this precipitous decline in household consumption. The political situation prompted severe pessimism throughout the economy, affecting both consumers and investors.

We can see once more that the years 2011 and 2012 come into play as in the last two columns. Households started to curtail consumption since during the PPP time. Therefore, it should be no surprise that by 2015 and 2016 businesses would start cutting investments. A series of political shocks after the 2011 General election most likely accounted for this precipitous decline in household consumption. The political situation prompted severe pessimism throughout the economy, affecting both consumers and investors.

The consumption decline should not be seen as a minor economic event. It is the main force behind the pessimism pervading the society these days. Let us look at another country for context. At present consumption as a percent of GDP in the United States stands at around 66%. If consumption in America fell as dramatic as it did in Guyana, that country would be in an economic depression (not recession). However, the mechanics of the Guyanese economy are different since Guyana imports most of what it consumes, so we can still have tepid GDP growth in spite of the consumption collapse.

On top of the dramatic decline of consumption, government started to curtail its capital spending from 2011. Government investment (the red line; left axis) on capital projects was 15.2% in 2010, but declined almost monotonically from 2011 until 2015. In 2015, government investment or capital spending was only 4.4% of GDP. This decline largely reflected the parliamentary fights over budget spending, hence the political shock. The APNU + AFC government boosted capital spending to a projected 25.4% in 2016, a quite dramatic turnaround. Therefore, we can expect money to start circulating again over the next 18 months, barring a major unforeseen negative event.

These trends suggest that political uncertainty (or several political shocks) is the primary determinant of the pessimism driving private investment and household consumption. Political conflict over the budget accounts for the steep decline in capital spending. The malaise in the economy and the foreign exchange market has nothing to do with a Jagdeoian capital strike, even if he might have said the wrong thing at some point. The entire political class has to be blamed for the sufferings of simple people who have to bear the higher price from devaluation. The political class continues to put off fundamental reforms, preferring instead the preservation of party interests.

But why should there be a foreign exchange problem? The contraction of government and private spending should improve the current account of the balance of payments, which in turn should put less pressure on the Guyana dollar. Indeed, we saw in part 2 of this series that the current account improved significantly from 2012.

Therefore, why should there be pressure on the Guyana dollar? When investors and consumers are pessimistic they will look for safe assets instead of investing long-term and consuming beyond basic requirements. Foreign exchange is an apt safe asset. If an exporter is earning foreign currencies he might choose to park them overseas and wait and see how the politics play out. If a family gets some cash remittances they could sell to a cambio or their well-off neighbour who prefers to hold on to the hard currency. The owners of hard currencies will be persuaded to release them into the market only if someone pays a much higher curb rate.

In the next column, I will look at the capital account of the balance of payments to get more insights into what is going on. Up until this point, I would say the political karmas are playing out in 2016 and 2017. It has nothing to do with a Jagdeo-specific shock or the curtailment of drugs money.

Comments: tkhemraj@ncf.edu