Introduction

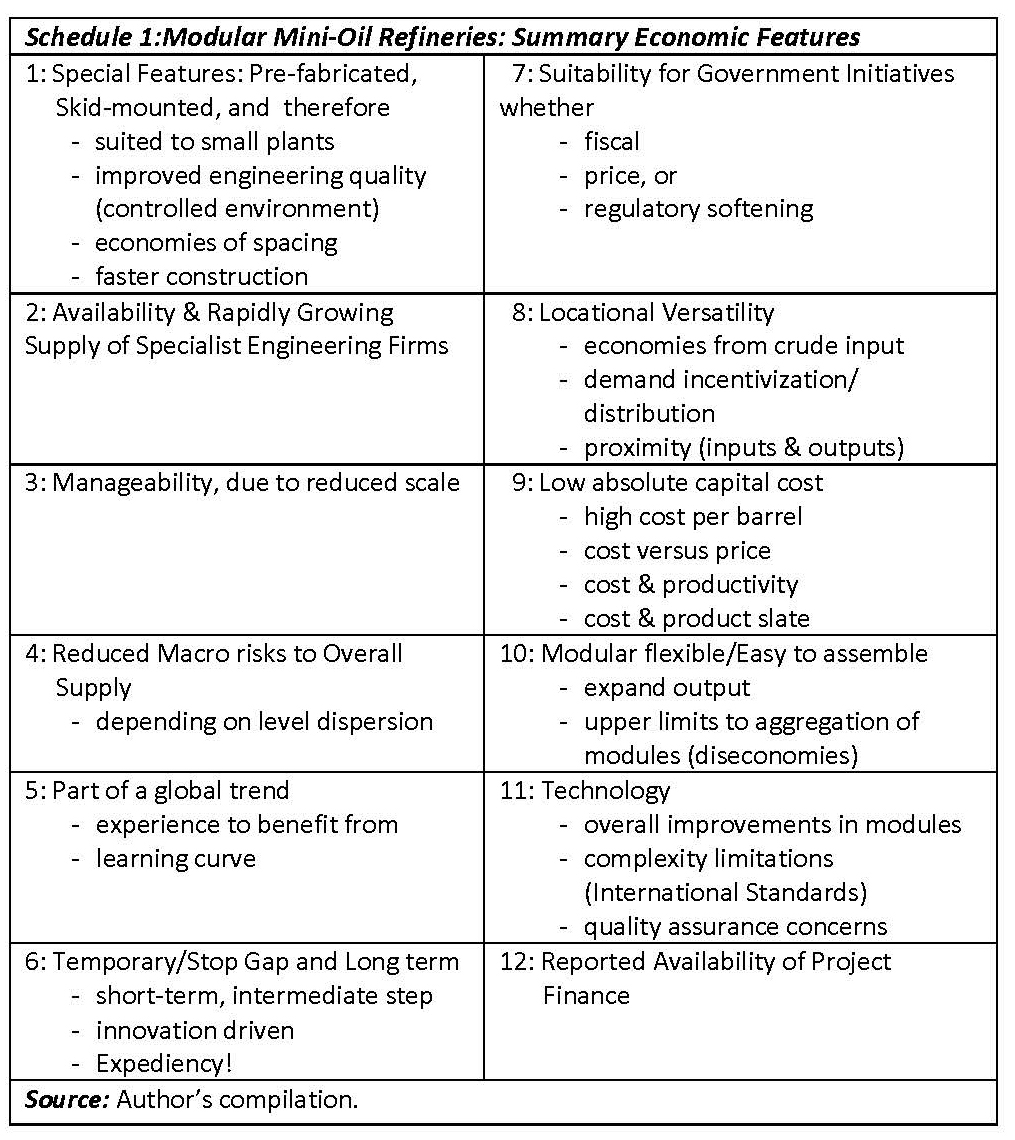

Today’s column revisits my previous estimate of the likely crude oil price at the time Guyana’s first oil is anticipated to be fully on-stream (2025). Next week I will revisit similarly my earlier assessment of Guyana’s petroleum discovery. Before attending to these tasks, I present the promised Schedule, Modular Mini-Oil Refineries: Summary Economic Features, which summarizes the 12 economic features of mini-oil refineries highlighted in the two previous columns.

Today’s column revisits my previous estimate of the likely crude oil price at the time Guyana’s first oil is anticipated to be fully on-stream (2025). Next week I will revisit similarly my earlier assessment of Guyana’s petroleum discovery. Before attending to these tasks, I present the promised Schedule, Modular Mini-Oil Refineries: Summary Economic Features, which summarizes the 12 economic features of mini-oil refineries highlighted in the two previous columns.

Cost

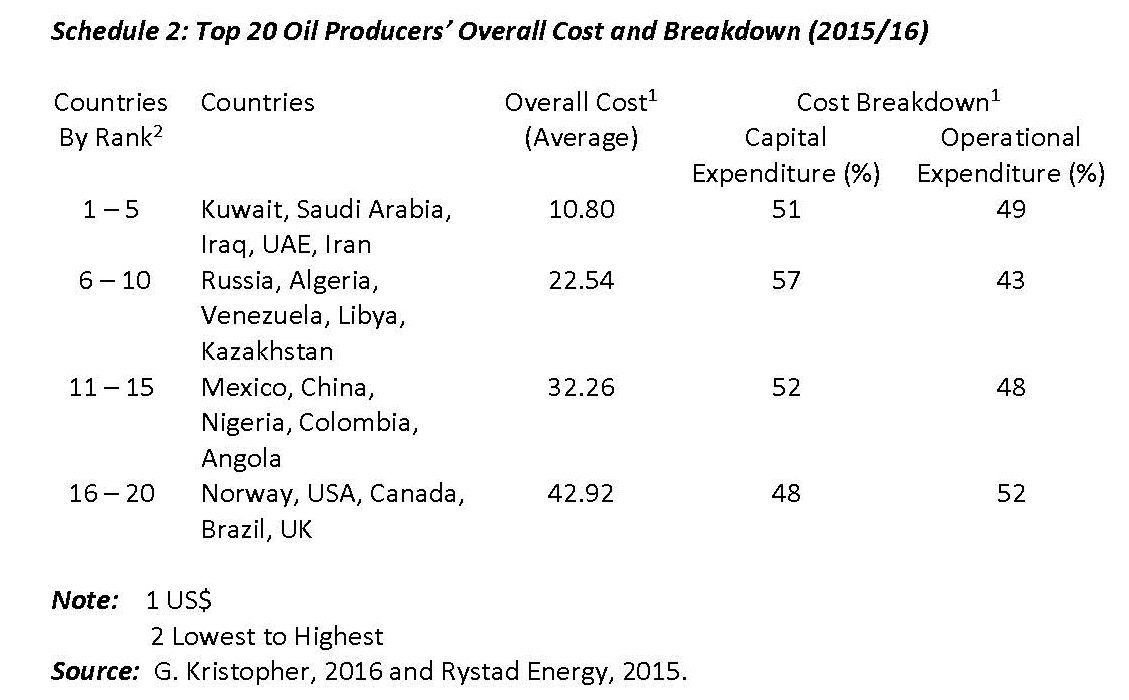

In an earlier column, October 23, 2016, I had predicted the likely cost-price relation for crude oil in 2025, the year Guyana is anticipated to commercially transform its petroleum discovery. Presently, however, exploration is ongoing, so the exercise remains indicative. The wider though, the positive difference between the overall unit cost of producing oil and gas and their market prices, the greater is the potential benefit for Guyana. Schedule 2 reproduces previous estimates of the overall unit cost of oil production for the top 20 producing nations.

Guyana’s petroleum project, however, confronts significant cost challenges, including 1) logistical, based on its offshore location and lack of installed infrastructure; 2) workforce health and safety; 3) environmental risks; (oil spills and other accidents) and 4) process management of petroleum reserves. Offshore production utilizes facilities/techniques, which raise unit costs: expensive drilling platforms and submersibles exploring deep-water environments; production platforms designed for removing petroleum out-of-the ground, and to market. Such operations entail rising costs as they require specialized workers and difficult process management.

Given these circumstances there exists as yet no firm basis for determining production costs for the Guyana “discovery”, with reasonable certainty. The indicative cost details offered above therefore remains the best guidance that can be achieved sensibly.

Indicative price

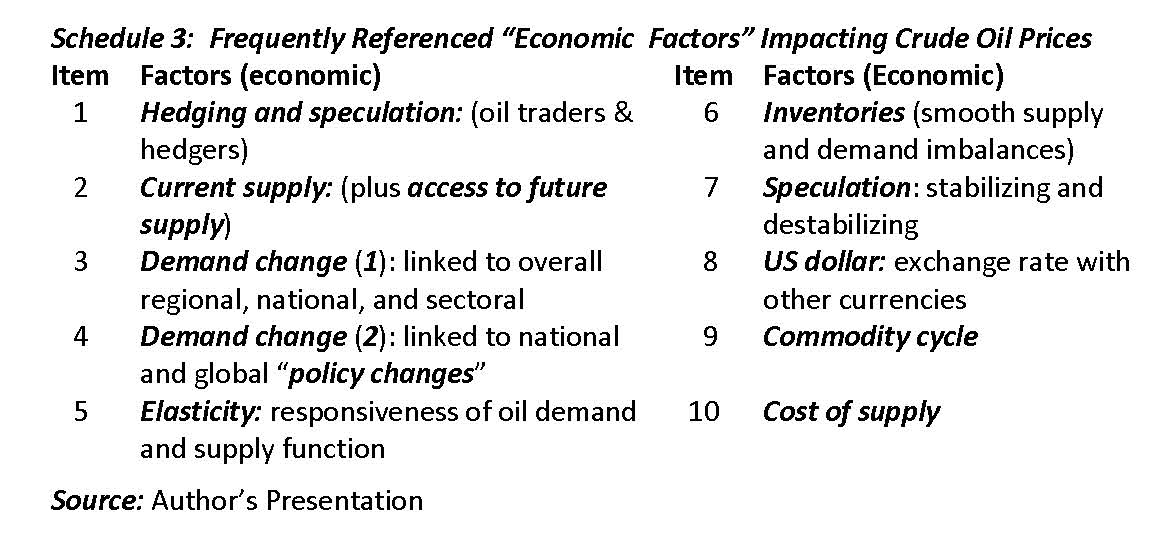

As regards price, economists’ model price behaviour as a function of the quantity demanded and supplied. Demand largely depends on 1) purchasing power (in turn dependent on incomes, wealth, and so on); 2) consumer preferences (for example, oil versus other energy products); 3) prices of close substitutes; 4) expectations; and 5) the number of potential consumers. Relatedly, quantities supplied are primarily dependent on 1) their production costs; 2) access to reserves; (oil deposits!); 3) expectations; and 4) total supply. Economists expect these demand and supply forces to configure all markets and their prices, including crude oil. However, as previously indicated, crude oil is traded in highly complex markets. Indeed, so complex are those, even these formidable forces do not satisfy.

Schedule 3 lists ten commonly referenced economic factors impacting oil prices:

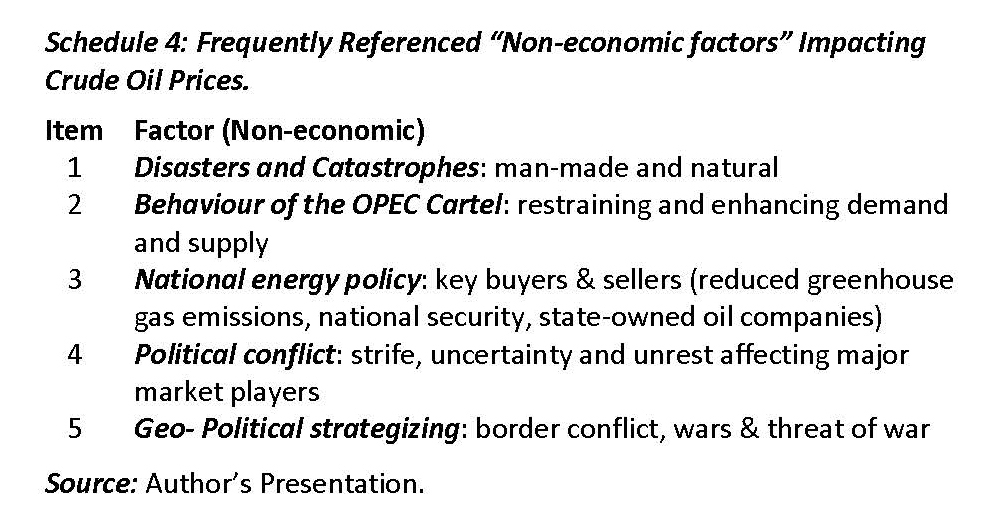

Non-economic factors

As indicated, oil prices are also heavily impacted by non-economic factors. Schedule 4 highlights five of these:

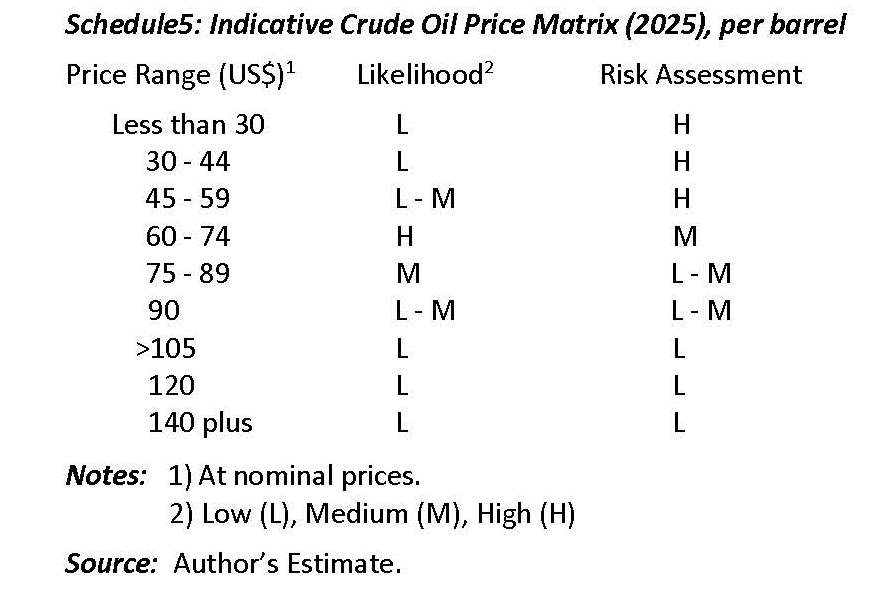

Indicative price holds

I had constructed a matrix in the earlier referenced column, October 23, 2016 (see Schedule 5). This indicates the target crude oil price range that I estimate will prevail in 2025. I hold on to that estimate, nearly a year later.

The price range in the Schedule is provided in units of US$15. The likelihood of each listed price range is rated on a scale from low to high, (as shown in the notes) The Schedule also indicates the level of assumed risks confronting the commercial viability and sustainability of Guyana’s oil and gas industry over different price ranges.

Next week’s column will briefly comment on this indicative price and then turn to updating my assessment of the petroleum discovery.