The previous column critically analysed the cost components of the production sharing agreement with ExxonMobil. We noted that the legal aspects did not cover all the possible cost scenarios, which is crucial for PSA-type contracts. In keeping with the theme of this series of essays, I argue the legal protection against cost uncertainty does not exist because the APNU+AFC government thought a contract was purely legal exercise. It is clear to me that the government negotiators did not appreciate how unit cost may vary over time and over barrels produced.

The previous column critically analysed the cost components of the production sharing agreement with ExxonMobil. We noted that the legal aspects did not cover all the possible cost scenarios, which is crucial for PSA-type contracts. In keeping with the theme of this series of essays, I argue the legal protection against cost uncertainty does not exist because the APNU+AFC government thought a contract was purely legal exercise. It is clear to me that the government negotiators did not appreciate how unit cost may vary over time and over barrels produced.

Minister Gaskin compared the expected oil revenues with existing commodity exports, particularly gold. He presented a wide range of possibilities, some of which were compared with exports from the gold sector. He argued that oil revenues around US$300 million a year is no chicken feed money.

I think the judgement of whether the contract delivers chicken feed money depends on the demand for the projected revenues. Almost all of Guyana’s existing infrastructure has to be rebuilt. Building roads and other infrastructure along the coastal plain is very expensive and often results in cost overruns. Climate change will make it necessary to move inland, hence new infrastructure. The infrastructure at the University of Guyana will need a complete do over if it is to become a serious regional university generating its own revenues. New housing schemes will have to be properly developed before humans are allowed to move in and there will need to be a reassessment of all the canals that were filled over in the past 70 years. From Ruimveldt to the Harbour Bridge, I can think of eight canals, some stretching deep into the backlands that were filled up. That is only one small area. Of course, the tinkered 1980 Burnham Constitution incentivises and institutionalises a certain amount of patronage waste that will occur. It is a Guyanese law of motion that is almost as certain as those of physics.

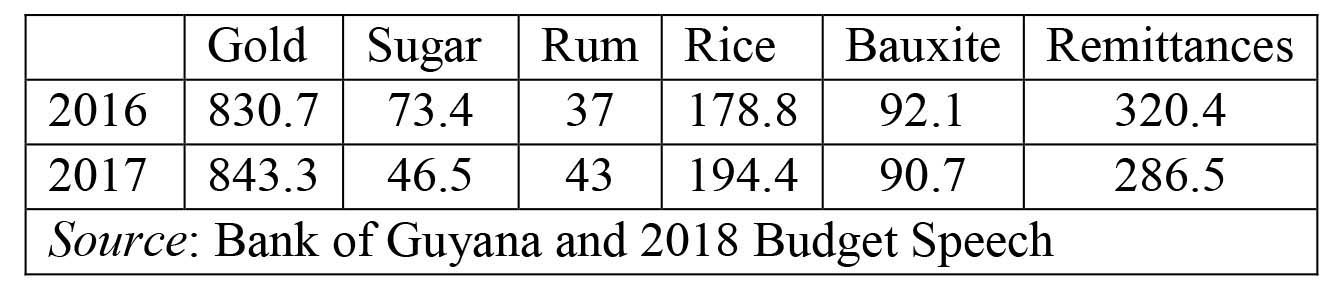

For context, therefore, let us take a look at the main export earners in 2016 and 2017, as well as remittances. Remittances are not exports; they are gifts in cash and kind. As we can see from Table 1, Gold exports – those of which we know – amount to over US$800 million in both 2016 and 2017. It is very likely that with the smuggled component, gold exports amount to over US$1 billion. Rice exports are closing in on US$200 million and bauxite is suggesting a downward trajectory. While sugar is on its steep decline, rum exports continue to expand. Outside of gold, remittances still represent the second largest source of foreign exchange for Guyana. Unlike gold, remittances represent foreign exchange and gifts that actually enter Guyana.

Table 1 Main exports and remittances – US$ millions

How much in terms of oil revenues would central government receive? This largely depends on the market price prevailing in any given year, the average or unit cost of production and the number of barrels produced. These three variables have to enter into the equation taking into consideration the features of the contract, which include the 2% royalty and the 50-50 per cent profit share. We are not sure how cost will vary over time and over barrels produced. This is also related to the important matter of ring fencing in which the cost of one block cannot be transferred over to another.

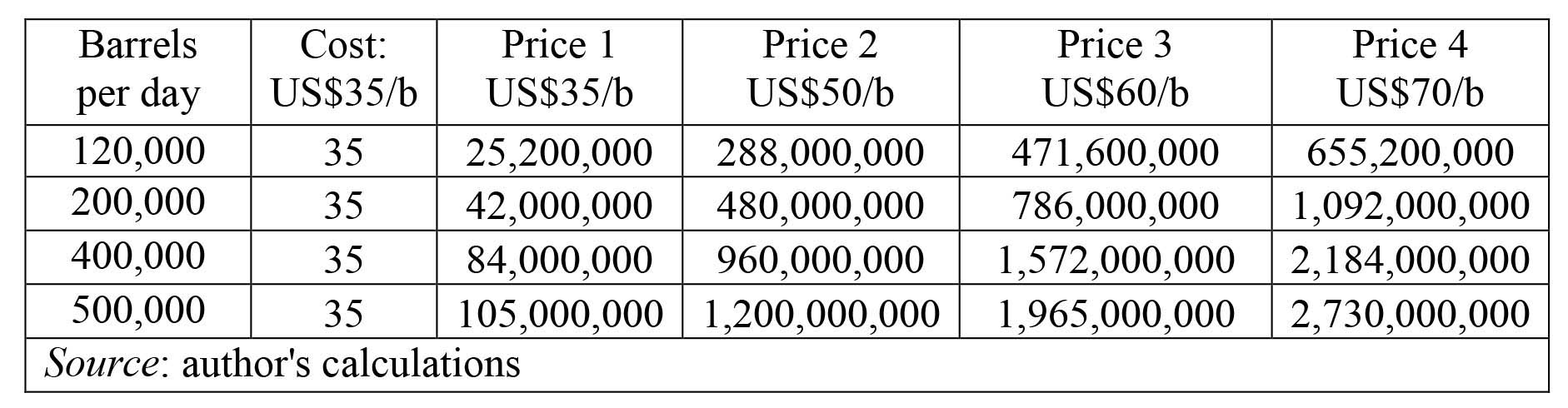

Nevertheless, we have to heap all the cost components into one number: an estimate of US$35 per barrel. This cost includes operating, exploration, development, decommissioning and others. Economic theory tells us that as production level increases unit cost should decline. Finance theory tells us that an investor would like to recoup capital expenses as soon as possible during the lifetime of the project. The contract does not account for these conceptual understandings; therefore, we have to just use one crude estimate of US$35 per barrel. It should be noted that the IMF report for the Minister of Finance uses a significantly lower average cost of just under US$21 per barrel. In a coming essay, we would look at expected revenues taking into account the lower IMF cost estimate. This column is already getting overloaded with information, so I will use the US$35 per barrel.

I think the US$35 could be more realistic since in the early years of the project the cost should be higher. I looked at the scenarios when market price is US$35 per barrel, US$50 per barrel, US$60 per barrel and US$70 per barrel. The probability exists that in any given year the price could be any range given above or otherwise. The production levels are 120,000 barrels, 200,000 barrels, 400,000 barrels and 500,000 barrels per day.

The possible revenues going to central government are presented in Table 2. If the price falls to US$35 per barrel, then Guyana earns the

royalty alone. The country will earn US$25.2 million at 120,000 barrels per day and US$105 million at top capacity (at least for now; Guyana could be producing over a million barrels by 2030). This is not a lot of money compared with the demand for revenues. The top end estimate does not exceed rice or remittances when the market price falls to US$35 per barrel. I guess this is better than nothing, but it might be more in the corner of chicken feed money given needs.

Table 2 Possible revenues flowing to central government – US$

However, once the price hits US$50 per barrel and production exceeds 200,000 barrels only gold will provide more revenue. One can see this as a lot of money. However, part of this new revenue will have to make up for lost revenues previously earned by sugar and bauxite, two industries in a long-term decline. The same US$50 per barrel and production of 500,000 barrels per day will bring in a whopping non-chicken feed amount of money of approximately US$1.2 billion in that year. This is about 1/3 of Guyana’s GDP. It is a lot of money and hopefully it will do a lot of good. I am pessimistic given the present political structure and class in Guyana. But I sincerely hope I am wrong.

Notable in Table 2 are the wide variations in revenue when price changes from US$35 to US$70 per barrel for any given level of production. At 120,000 barrels the revenue can be as little chicken feed money as US$25.2 million to medium chicken feed money of around US$655.2 million per year. At the top end production of 500,000, revenue could be chicken feed US$105 million or a spectacular non-chicken feed amount of US$2.73 billion.

The latter scenario shows why it was crucial for the contract to have some proportional increase in government revenues once price exceeds US$60 per barrel. In that way, higher revenue in good times can fund acute shortfall in bad times.

In closing, these numbers emphasise how important macroeconomic management as well as smart industrial policies will become after 2020.

Comments: tkhemraj@ncf.edu