Introduction

Introduction

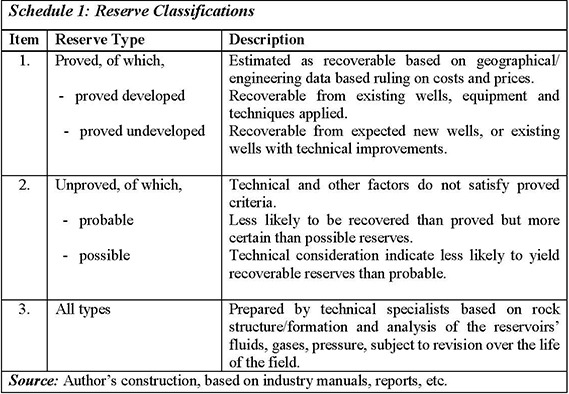

Last week’s column addressed two of five topics singled out earlier for comment in order to highlight their significance from an economic perspective; namely 1) Government take/developmental benefits/economic profit; and 2) accounting for costs. Today I focus on two others namely: the measurement of hydrocarbons resources & reserves; and, tax compliance. Next week I shall provide wrap-up comments on the petroleum project’s life cycle. I start today’s, offering a concluding comment on last week’s discussion of topic 1), omitted because of lack of space.

Government take

Recent estimation of Government take for 19 countries (averaged over the period 2009-2014) is shown in Table 1. The information reveals significant variability. As previously explained, Government take is a vital fiscal metric, but is not accorded great priority by private investors. Private investors concentrate instead on net present value (NPV), internal rate of return (IRR) and the profit ratio (PR). Such private profitability measures are expressed at discounted or undiscounted values.

There is regular misuse of this measure in the local media. Therefore, it should be advised that when governments discount these values, they are using a social discount rate (which is a subjective metric) while when firms do so they use a market (objective) discount rate. The former rate is routinely higher than the latter. Table 1 shows the information mentioned above.