Column 43 dealt mainly with Associated Gas and my plan was to deal with non-associated gas this week. However, the availability of the annual returns and financial statements of Hess Guyana Exploration Limited necessitates that attention turns to the famous US$460 million as pre-contract costs.

Column 43 dealt mainly with Associated Gas and my plan was to deal with non-associated gas this week. However, the availability of the annual returns and financial statements of Hess Guyana Exploration Limited necessitates that attention turns to the famous US$460 million as pre-contract costs.

Readers of this column will be aware that the column has repeatedly lamented the failure of Hess, the holder of a 30% interest in the Stabroek Block, to meet its legal obligations to Guyana to file annual returns together with audited financial statements of the branch. Some attempt to meet that obligation has recently been made with returns for 2014 to 2016 now submitted and placed on file. However, that company’s file at the Commercial Registry shows that the annual return for the year 2015 filed on March 22, 2018 did not contain any financial statements for 2015. This is a critical year since expenditure on recoverable pre-contract cost was divided into two periods – up to December 31, 2015 and from January 1, 2016 to the effective date of the Petroleum Agreement. The amount up to December 2015 was fixed at US$460,237,918 while the amount for the period January 2016 to the effective date of the Agreement was to be agreed on or before April 30, 2017.

I have chosen not to treat the absence of 2015 financial statements as particularly significant or fatal since the 2016 financial statements contain comparative numbers for the preceding year (2015) and there was no indication of any restatement of the 2015. Accordingly, it is fair to assume that the comparative figures shown in the 2016 financial statements for 2015 accurately reflect what would have been contained in the 2015 audited financial statements.

Checking the numbers

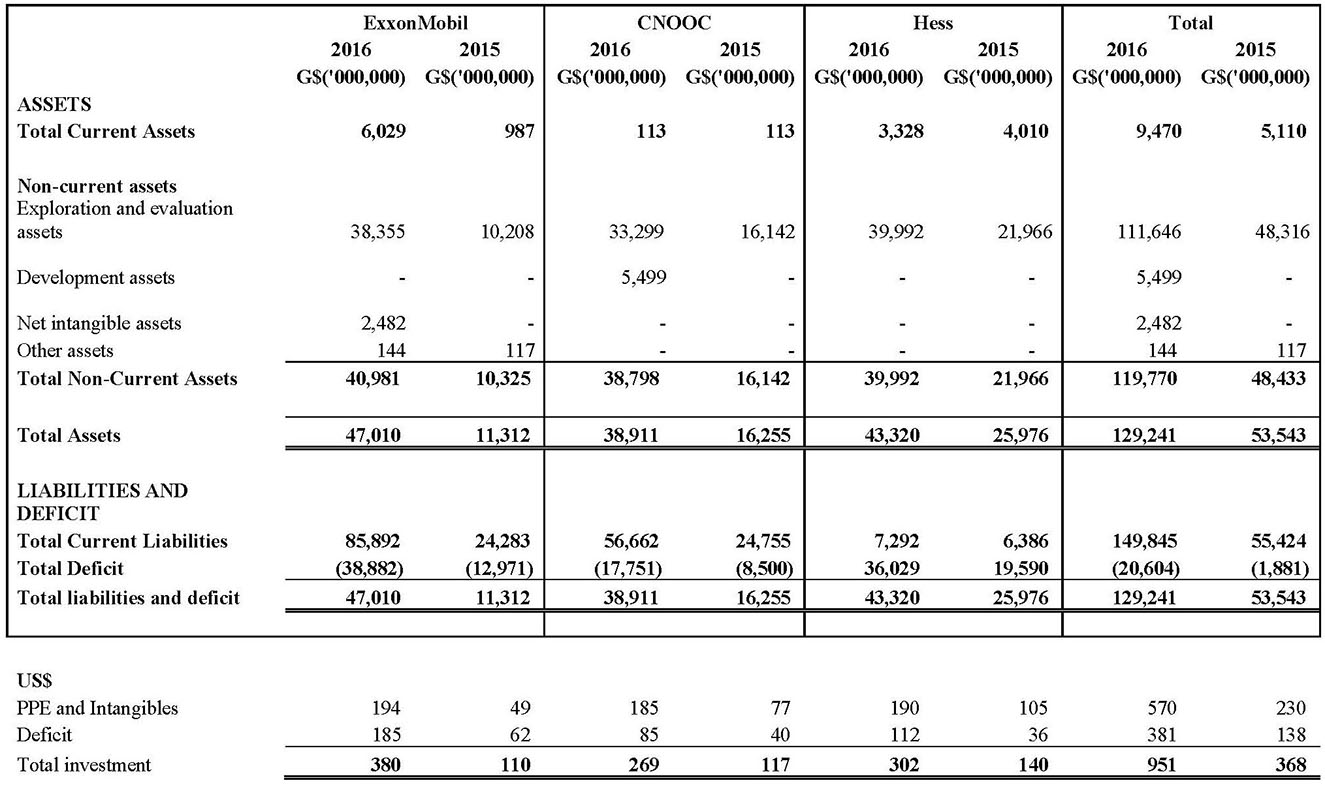

The availability of the Hess’ 2015 numbers now makes it possible for us to assess the correctness of the amount of US$460,237,918 being claimed by the three companies as pre-contract costs incurred under the Petroleum Agreement which Esso had signed with then President Janet Jagan way back in 1999. The Table below has been constructed from the audited financial statements of the three companies, or to give them their technical label, external companies. It shows that even allowing for all expenses and expenditure by the three companies, the total falls well short of the US$460,237,918 claimed by them.

Unless Esso, Hess and CNOOC/Nexen can come up with answers and explanations to what appears to be a very significant difference between the amount claimed and what the financial statements at a gross level reveal, they will encourage suspicion of grave impropriety in overstating their claim. It is clearly in their joint and several interest that they provide full, complete and credible explanations supported by authentic documentation capable of withstanding a rigorous audit and that they agree voluntarily to submit themselves to such an audit. I will raise those questions next week after first holding our government accountable.

Holding Government accountable

Not only do they have lots of questions to answer but so too do Minister Raphael Trotman whose signature appears on the Agreement, and the parade of senior government ministers including Foreign Affairs Minister Carl Greenidge, the Cabinet and President Granger all of whom claimed ownership of the Agreement.

My questions to President Granger, Minister Trotman, Minister Greenidge and the rest of the Cabinet.

1. Whose idea was it to place a major matter involving nearly one hundred billion Guyana Dollars in an Annex rather than in the body of the Agreement?

2. Was Annex C which contained the figure available and read simultaneously with the Main Agreement by the President, Ministers Trotman and Greenidge and the rest of the Cabinet?

3. Was the figure US$460,237,918 set out in the Annex supported by detailed statements by each of the three companies?

4. Was any verification exercise done of the pre-contract expenses figures and information provided? If so, by whom?

5. Was the Audit Office asked to verify the figure?

6. Who checked to verify that the sum claimed was consistent with the rest of Annex C, in terms of categories, allowed and not allowed etc.?

7. If there was no verification at that stage, why was provision not made for such verification at a later date?

The numbers gap

What the Table shows is that at the very least, the claim of US$460 million is overstated by approximately US$92 million. I say at least because not all expenditure is recoverable as pre-contract costs. For example, Esso had close to US$5 million in current assets, mainly in inventory, which will be expensed as they are placed into use and consumed. Only at that point should they be expensed as contract cost. Therefore the amount should not be included as pre-contract cost.

Changing relationships

But a further problem arises when one looks at the bigger picture of the relationship and its history among the partners. Readers will recall that Column 38 drew attention to the 2016 financial statements of Esso which reported that in 2014 it had entered into farm-out arrangements with Hess and CNOOC/Nexen and that Government approval was still pending, i.e. two years later. Such a statement made little sense because just prior to the end of the first half of 2016, Esso, Hess and CNOOC had become co-contractors under the new Agreement signed secretly by Trotman and concealed for close to eighteen months. Readers will recall that public and still partial release of the Agreement was practically forced on the Government following the confirmation of a signing bonus to be paid to the Government of Guyana.

CNOOC reporting of the relationship was quite confusing, if not misleading, disclosing both a working interest and joint arrangements, terms that have different meanings in the petroleum sector. What is more significant however is that CNOOC’s financial statements reveal that it acquired its working interest from ExxonMobil, which I have been at pains to point out is a completely separate entity from Esso Exploration and Production Guyana Limited. The financial statements now filed by Hess report that Hess acquired a “participating interest in the Stabroek Block” while the company’s ultimate parent company reported to its international stockholders that it had acquired a “working interest”, which is another term for farm-out. To add further to the complexity, in 2008, Esso had entered into an Assignment Agreement and a Farm-out Agreement with Shell which would have also had financial implications.

Questions

1. Would Esso account to the people of Guyana for this nearly US$92 million difference?

2. Was any money paid by Shell, Hess and CNOOC for the interest they acquired? If yes, how much and how is the money accounted for in the books of all the parties?

3. Is CNOOC’s statement that it acquired its interest from ExxonMobil correct? If yes, how much money, if any, was paid?

4. Did Esso as the Operator and largest interest holder verify all the pre-contract costs of the parties?

5. Were details of the pre-contract costs, together with supporting documentation, provided to the Government for verification and for its records?

6. Had this line item not been specifically inserted in the 2016 Agreement, would the expenditure qualify as recoverable under the criteria set out in 1999 Agreement?

7. Was a reconciliation between the amount stated in Annex C and the separate financial statements provided to the auditors?

8. Would the three companies constituting the Contractor be willing to submit the pre-contract costs to an independent audit?

Conclusion

Pre-contract cost ranks with royalty, stability clause, no tax and secrecy as the more egregiously objectionable features of the 2016 Agreement. It would be good if at least this one is put to rest to the satisfaction of Guyanese. On the other hand, the oil companies must know that they ignore these questions at the risk of their reputation. Guyanese are not gullible or without options.