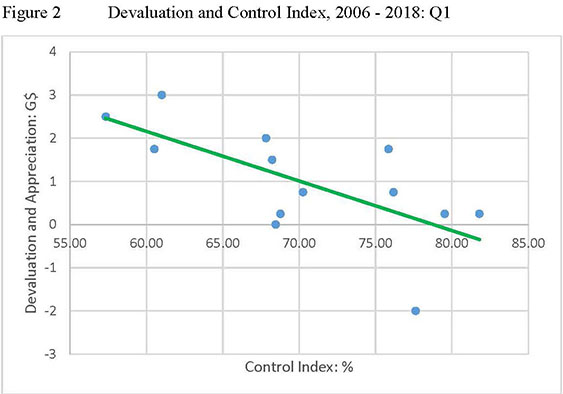

The main monetary policy target of the country’s central bank, Bank of Guyana, is the exchange rate. The central bank fine-tunes its sales of Treasury bills and at times uses some form of moral suasion to achieve its desired exchange rate target. Since 2004 the central bank has done a remarkable job stabilizing the exchange rate in spite of the political climate. The monetary policy makers can only do so much to achieve the goal of macroeconomic stability, of which the exchange rate with respect to the US$ is the primary target.

The main monetary policy target of the country’s central bank, Bank of Guyana, is the exchange rate. The central bank fine-tunes its sales of Treasury bills and at times uses some form of moral suasion to achieve its desired exchange rate target. Since 2004 the central bank has done a remarkable job stabilizing the exchange rate in spite of the political climate. The monetary policy makers can only do so much to achieve the goal of macroeconomic stability, of which the exchange rate with respect to the US$ is the primary target.

Last week a main commercial bank was selling one US$ for 217 Guyana dollars. This is just one observation, however. The Bank of Guyana would usually take the average of all the cambios and commercial banks. The average, from my cursory observation, is closer to G$213 to one US$. This represents a devaluation from the relative stability of earlier years. The average rate was exactly G$199.99 to one US$ in 2004. Since then there has been a creeping devaluation of the Guyana dollar. The intensity of the devaluation seems to have picked up since mid-2016.

The government claims that Caribbean nationals are busy taking out US$ from Guyana. The unwinding of the narco-economy is given as another reason. I find neither of these convincing explanation for the creeping devaluation. It is not that the government has done nothing to clamp down on narco trafficking. The Granger administration certainly has. However, this has nothing to do with the pressure evident in the foreign exchange market these days.