Introduction and Definition

Introduction and Definition

Today’s column develops further the discussion of the IMF’s Fiscal Transparency Code. I had proposed Guyana’s unqualified adoption of this Code, as the most effective means for forging a seamless integration of spending the expected Government Take from the petroleum sector and the national fiscal and budgetary systems. The column elaborates on the Code and its contents in, hopefully, an easily digestible manner, given its technical and operational bias.

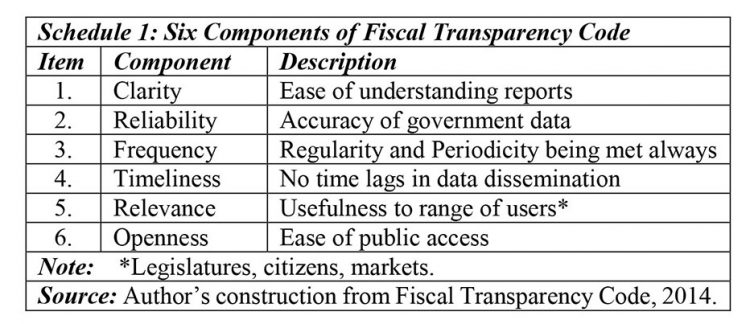

A useful starting point for this discussion is the query: how does the IMF interpret fiscal transparency. For starters, its’ Handbook on the subject states: “Fiscal transparency refers to the information available to the public about the government’s fiscal policy making process”. The Handbook goes on to elaborate on this in some detail. It famously interprets the quote as referring to: “the clarity, reliability, frequency, timeliness and relevance of public fiscal reporting and the openness of such information”.

These six listed features are captured in Schedule 1, where a brief description of each feature is also provided. Thus clarity refers to the “case with which reports can be understood by users”. Reliability refers to “the extent to which reports are an accurate representation of government fiscal operations and finances”. Frequency or periodicity refers to the “regularity with which reports are published and disseminated”. Timeliness refers to the “time lag involved in the dissemination of these reports”. Relevance refers to the “extent to which reports provide users (legislature, citizens, and markets) with the information they need to make effective decisions”. And, finally, openness refers to the “ease with which the public can find information, and influence and hold government accountable for their fiscal policy decisions”.

The role of fiscal transparency in the effective management of Guyana’s expected petroleum and other natural resources revenues cannot be exaggerated or overemphasized. As a rule, fiscal transparency encourages Governments to base their decisions on an informed and shared accurate assessment of the country’s fiscal situations. In this manner, it also allows for the accurate determination (cost-benefit analysis) of various policy options, which the Authorities face. Such analysis invariably results in improved government accountability. Consequently, we may therefore advance that, the above simultaneously facilitates for Guyana, national, regional and international surveillance by the IMF, World Bank, CARICOM. There is also the role of sectoral multilateral bodies like the EITI and the NRF (Santiago Principles). In other words, higher standards at the global and regional levels invariably supports Guyana’s efforts at best practices.

Taking the global and regional situation into account one can argue that, from the macroeconomic management standpoint the Transparency Code can help Guyana to mitigate, through global and regional cooperation, adverse transmission effects; especially from price volatility, which as readers are aware, is deeply embedded in petroleum markets for crude oil.

Recognition

To add to the above considerations, it is widely admitted that, as the Code itself proclaims: “The IMF’s Fiscal Transparency Code is the most widely recognized international standard for disclosure of information about public finances” (my emphasis). It is for this reason, it has become a leading edge in IMF’s efforts 1) to improve surveillance 2) to support policy making and 3) improve fiscal accountability.

The IMF’s review of global shortcomings after the 2007/8 global financial crisis revealed that “even among advanced economies, reporting by governments of their fiscal operations and finances was incomplete”. Indeed, the IMF points out that the global crisis had revealed several instances of “unrecorded deficits and debts in these countries”. Those countries’ underestimation and under-reporting of risks is now revealed to be quite notorious! Indeed it might be argued that it was because of this notoriety the IMF took action to galvanize globally to arrive at improved standards for global public finances. As noted earlier, there were several similar global efforts at the time, but I remain firmly of the opinion that, the IMF’s effort represents the most advanced, which the IMF itself has asserted. To quote: “The Transparency Code (2014) comprises a set of principles built around four pillars”. Each pillar “contains three to four dimensions, and each dimension two to four principles”. These will be addressed fully in next week’s column.

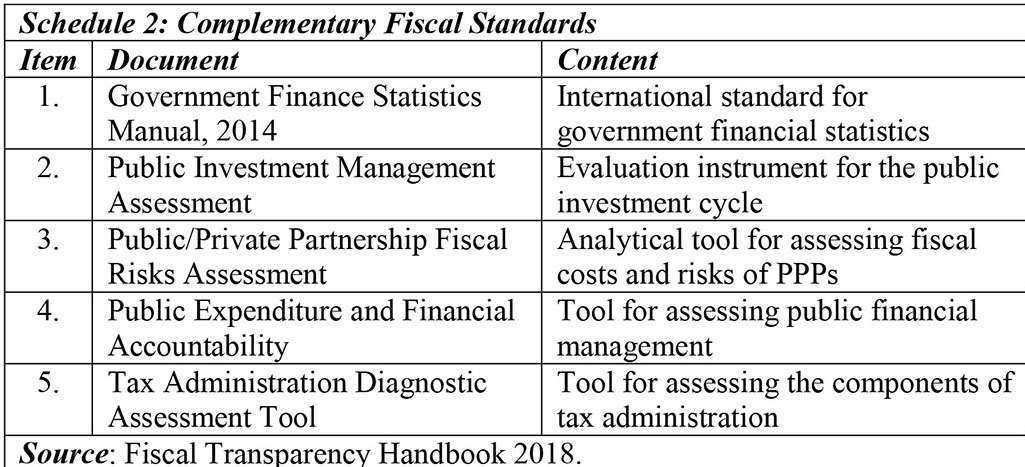

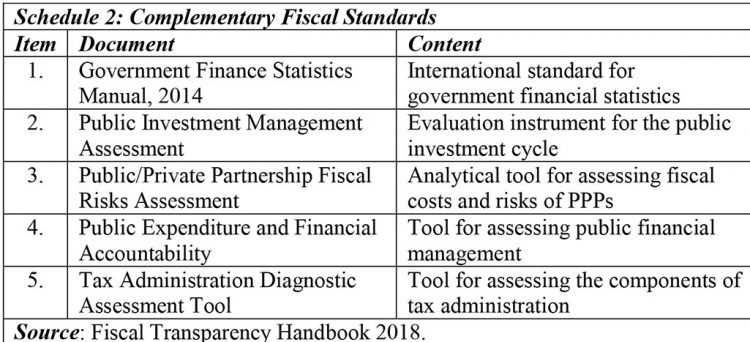

Meanwhile, I refer readers to some useful complementary data on fiscal standards and assessments. For convenience these are summarized in Schedule 2. The items identified in the Schedule are: Government Finance Statistics Manual, GFSM; Public Investment Management Assessment, PIMA; Public-Private Partnership Risk Assessment Model, PPRAM; Public Expenditure and Financial Accountability, PEFA; Tax Administration Diagnostic Assessment Tool, TADAT. To the above should be added (and of special relevance to Guyana) the Fiscal Analysis of Resource Industries, FARI. This last item is not listed in the Schedule. It contains a methodology for the fiscal analysis of extractive industries.

Conclusion

Next week I wrap-up discussion on this topic. I shall afterwards treat with fiscal stabilization, as earlier indicated in order to conclude the discussion on the top-10 development challenges posed for the spending Guyana’s expected petroleum revenues.