Introduction

Introduction

Today’s column addresses the tenth and final item in my non-exhaustive list of the “top-ten economic challenges”, which Guyana will have to confront as it operationalises its coming petroleum sector. That challenge is none other than the contentious issue of how to effectively integrate the country’s expected petroleum revenue inflows into the existing national budgetary process.

It should be noted at this juncture that, at the time of penning this column, Guyana’s petroleum discoveries continue to mount at a remarkable pace. Exxon and partners have just announced a 14th discovery in the Stabroek block, since mid-2015! This is the first of the three additional discoveries the group had projected for the second half of 2019. Accompanying this find, Tullow and partners have also announced their second discovery at Joe 1. This follows their discovery last month at the Jethro 1 drilling site. These developments will significantly impact Guyana’s expected petroleum revenue inflows, making this challenge one of rising importance.

IMF Fiscal Transparency Code

When I had considered this challenge of integrating petroleum revenues in the national budgeting process earlier in December 2018, I had indicated my strong preference for Guyana to adopt the IMF’s Fiscal Transparency Code 2014 as its national standard to guide the manner in which it addressed this issue. Today, I remain steadfast in this conviction. I shall, therefore, indicate the key elements of the Code as they relate to the Guyana Petroleum Road Map in today’s column. This is followed by a summary indication of the ways in which the “top-10 economic challenges” as a whole, must impact on Government spending of its petroleum revenues.

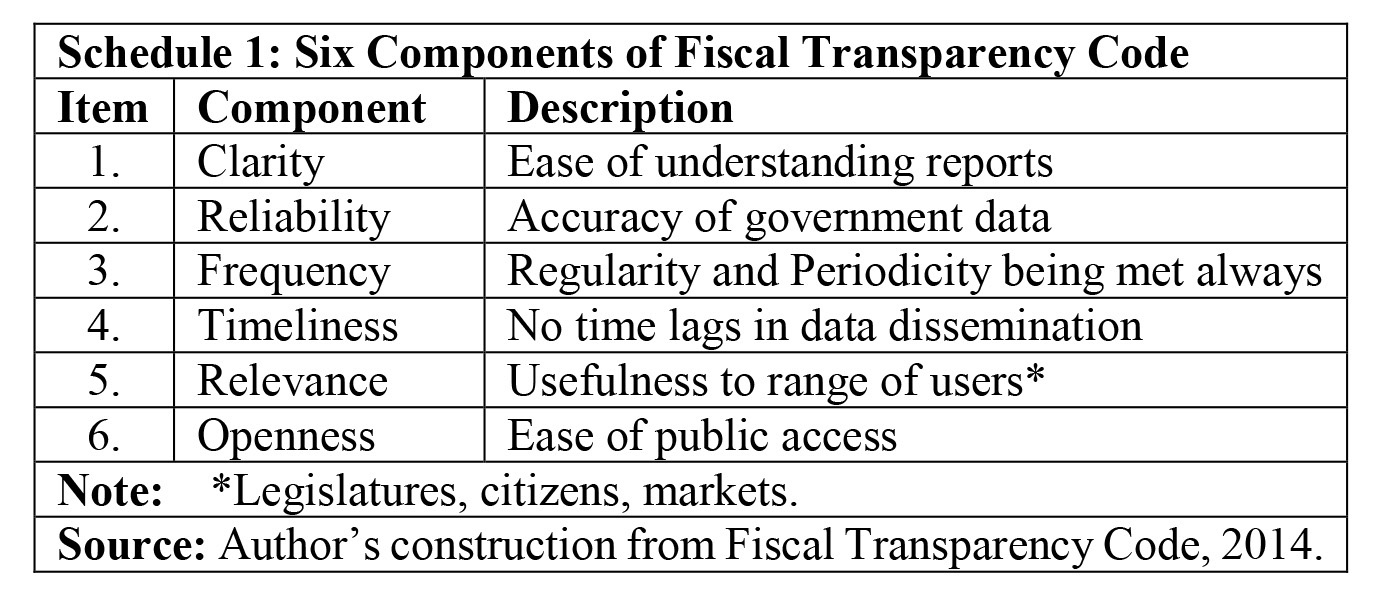

The IMF has defined “fiscal transparency” as the “information available to the public about the Government’s fiscal policy making process”. In turn this refers to the “clarity, reliability, frequency, timeliness and relevance of the public fiscal reporting and the openness of information” (IMF, 2014). For readers’ convenience, these six components are captured in Schedule 1 below.

As Schedule 1 reveals, clarity refers to the “case with which reports can be understood by users”. Reliability refers to “the extent to which reports are an accurate representation of government fiscal operations and finances”. Frequency or periodicity refers to the “regularity with which reports are published and disseminated”. Timeliness refers to the “time lag involved in the dissemination of these reports”. Relevance refers to the “extent to which reports provide users (legislature, citizens, and markets) with the information they need to make effective decisions”. And, finally, Openness refers to the “ease with which the public can find information, and influence and hold government accountable for their fiscal policy decisions”.

I do not believe the role of fiscal transparency in the effective management of Guyana’s expected petroleum and other natural resources revenues can be exaggerated or overemphasised. This is simply because, as a rule, fiscal transparency encourages the Government of Guyana (GoG) to base its decisions on an informed and (shared with the public) accurate assessments of the country’s fiscal situations. There are grave dangers in the absence of this attribute. This attribute allows for the accurate determination (based on cost-benefit analyses) of various policy options, which the Authorities face. Such analyses almost invariably result in improved government accountability. Consequently, I confidently advance the view here that this simultaneously facilitates for Guyana, not only national surveillance, but regional and international surveillance (by the IMF, World Bank, and CARICOM). The role of sectoral multilateral bodies like the EITI and the NRF (Santiago Principles) are also enhanced. This leads to higher standards at the global and regional levels, which invariably reinforce the GoG’s efforts to employ best practices, uniformly.

Taking the global and regional situation into account, I contend that, from the macroeconomic management standpoint, the Transparency Code can help Guyana to mitigate, through global and regional cooperation, adverse transmission effects; especially from price volatility, which as readers are aware, is firmly embedded in petroleum markets.

Significantly, it should be noted also that the IMF boasts its Fiscal Transparency Code is the “most widely recognised international standard for disclosure of information about public finances”. (IMF, 2014)

Conclusion for Public Spending

What are the implications of my Top-10 listed economic/developmental challenges Guyana will face as its petroleum sector is operationalised. First, it is important to recall that not all, of the economic/development challenges Guyana will face are listed in the Top-10 I have presented. As explicitly indicated, my list is non-exhaustive. Further, it displays the ten challenges in random order of importance. No ranking is intended.

Second, each listed challenge is a sub-category or component of a more general economic/ development challenge, which flows from Guyana’s expected petroleum industry. Third, all such challenges (as sub-categories or components) of one overall economic/development challenge) therefore, do not operate in isolation of each other. This is indeed understated, as in all likelihood every one of the “Top-10” challenges is expected to generate synergistic impacts on the others. Thus, for example, issues of expectations management will synergise in practice to magnify the problems posed by the Dutch Disease, or the Resource Curse, or indeed the Government curse.

Consequent to the above, therefore, all spending recommended in Part 2 of the Road Map will, in turn, synergistically interact to confront the development and economic challenges Guyana faces, going forward. Thus, spending on GoG priorities, which was considered earlier, is just as integral in confronting the Top-10 challenges, in the same way as the other proposals considered. For example, the creation of the Natural Resources Fund, NRF, proposals for the promotion of the renewable emerging sector, the avoidance of Government Investment in oil refining downstream, or even the proposed spending on cash transfers are all considered elements of an integrated and synergistic response to the also integrated and synergistic threat posed by the listed “top-10” economic/development challenges.

Conclusion

Next week, I begin discussion of Guidepost 4.