Dear Editor,

Guyana Goldfields in January 2016 declared that it had commenced commercial operations at its Aurora Mine on January 1, 2016. The mine plan announced at that time incorporated an initial five years of open pit gradually replaced with underground mining. Mine closure was provisionally planned for 2030 should the Company not find other reserves.

Both the PPP and the APNU+AFC facilitated this venture and ensured that they were given the necessary permits and duty-free concessions. The estimated average production was stated at 215,000 ounces annually.

A quick review of the following chart will show that the company not only failed to meet its stated objectives but a serious worrying trend seems to be developing and surprisingly not a report is emanating from the present government, the press or the economic gurus that pronounce so readily on Guyana’s economic performance.

1. Aurora Mine Annual Production (published by Guyana Goldfields)

If one checked the technical report filed on December 31, 2018 the company revised the average gram/tonne from open pit sources down to 2,6 grams/ton and surface stockpiles at 1.2 grams /tonne. On October 31st the company’s 3rd quarter reported that about 50% of the mill throughput came from surface stockpiles. What is really going on at Aurora? Whatever the reason it does not bode well since Guyana Goldfields was a major contributor to the country’s GDP. See table showing the grams/tonne mined over the years

2, Aurora average gram /tonne mined over the years.

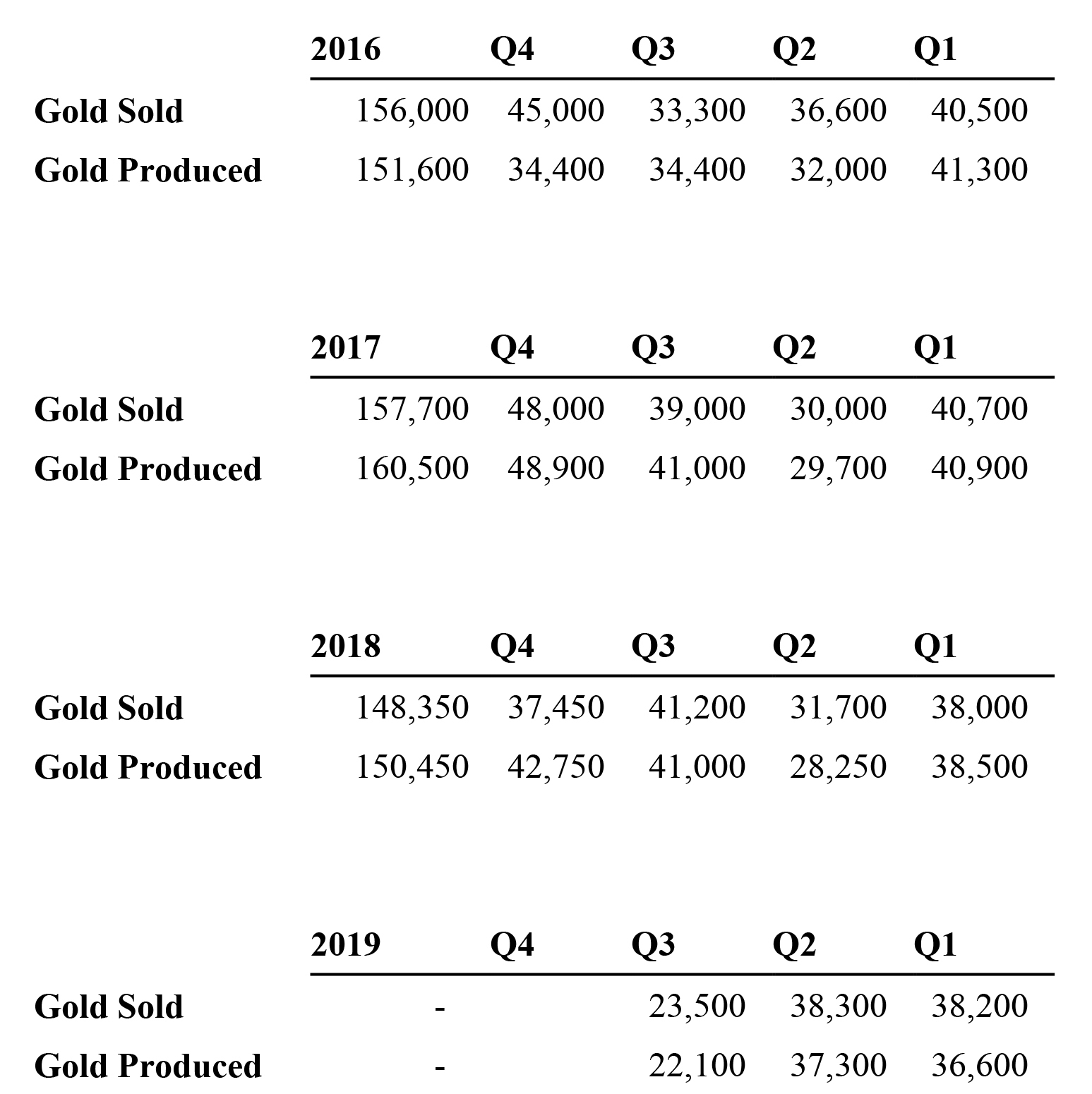

2015: 35,000oz at 3.16g/t

2016: 151,200oz at 2.74g/t

2017: 160,700oz at 2.49g/t

2018: 150,500oz at 1.99g/t

2019: 1st and 2nd Q =

74,000ozat 1.55g/t. 3rd Q =

22,100oz at 1.01g/

Guyana Goldfields stock has hit its lowest in 10 years since 2009 and it is time that the GGMC, the Minister responsible for this sector as well as the Finance Minister call this group in for fitness. Several groups had been warning about this decline over a year ago and it appeared that the hiring of window dressers and PR specialists had obscured the facts from emerging and had convinced the press et al to withhold the information and the main players from acting now the chickens have indeed come home to roost.

3. See Below the October 31,2019 article from Mining.Com

“The problem seems to be that they cannot seem to make money on their open pit operations on a cash-flow basis (inclusive of capex). Cost just keep going up the deeper they go in the pit due to the rising strip-ratio (ore-to-waste ratio). Next year the strip ratio is modeled to be 21 based on 2019 technical report so if they cannot make money at a strip ratio of 10 then perhaps they should just stop open pit operations. Based on the 2019Q3 report, it sounds like that is what they may be planning.

In which case, they could transition to underground operations but the capex to build that out is over $100m based on the 2019 technical report. Obviously they would need to debt finance that in order to get to that point though. Then there is management which has thus far not executed their plans very well. This puts a big question mark on how well they will perform going forward. If they continue to burn through their cash position and destroy value, they could be better off just selling company………..

The large discount is largely due to the lack of confidence in the management team. Can they execute without further destroying value of the company? If they come to the conclusion that the pit is no longer economic, perhaps they put the entire mine on care-and-maintenance to preserve cash burn while they build out the underground.”

Stock closed today at under .050 cents.

Yours faithfully,

Eustace Naughton