Dear Editor,

Despite the major acts of fiscal mismanagement of the Guyanese economy by members of Team Granger, when one reflects at the manner in which the Bank of Guyana continues to manage the monetary sector, one is pleasantly surprised. Dr. Gobind Ganga and his Team at the Central Bank continue to carefully manage our monetary policy in a financial landscape where all the key financial indicators are reflecting gross levels of executive negligence and massive acts of fiscal policy inconsistencies.

One only has to reflect on the deterioration in the productive sector, the state of aggregate demand, the runaway public expenditure and the increasing lack of investor confidence and one has enough evidence that the smooth economic expansion associated with a newborn oil economy is absent. The reality today is a struggle for survival by many, so much so that some 30,000 families have now joined the army of the poor since Christmas 2019. This is to the detriment of enhanced productivity in this nation. So much for the good life!

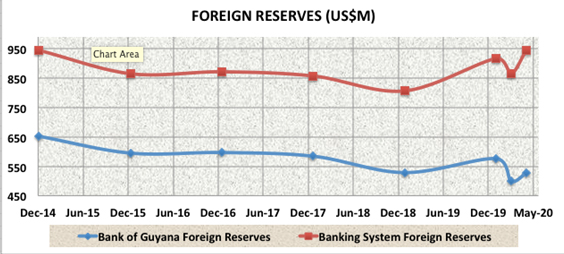

Central banks around the world accumulate reserves for a wide variety of reasons and the Bank of Guyana is no different. A typical explanation for holding these reserves highlights the fact that we must have the ability to pay our bills on time overseas. Reserves are also accumulated as a by-product of other factors, including the pursuit of price and financial stability, and even export competitiveness.

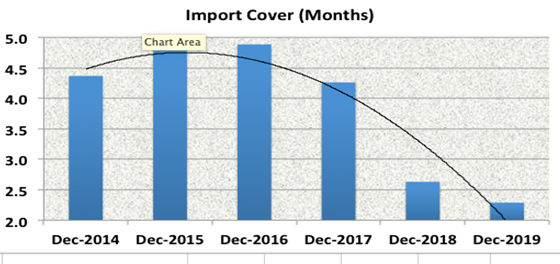

So the evidence is clear as to why Guyana should meet the international best practice as encouraged by the IMF, of having enough foreign reserves to honour 3 months’ supply of imports. Unfortunately, as the graph that follows highlights, our import cover has moved from a decent place at the end of 2016 when the nation had almost 5 months of import cover to 2.3 months at the end of December 2019. I was just provided with the evidence that at the end of March 2020, the import coverage has further declined to an annualized rate of under 2 months. This is a perilous place for any country to be situated; but this is Guyana’s tribulation in 2020 thanks to the mismanagement of the economy by Team Granger.

In a crude oil-exporting economy, imports usually expand rapidly in order to purchase massive amounts of capital equipment to support this sector. But the foreign reserves ought to have been bolstered by oil sales but this is not to be as a result of Guyana having a de-facto Government that cannot access these oil funds. Further, Guyana is also facing a real possibility of incoming international sanctions which will seal these earned oil revenue and all other export revenues. The outcome; another Venezuela.

From the graph that follows, the empirical evidence as sourced from Bank of Guyana, tells a story that is at variance to the one coming out of the Ministry of Finance. When Guyana did not have oil and a smaller economy in 2014, it had more foreign reserves available to the economic players. At the end of 2014, the banking system had access to US$945 million in foreign reserves, while at the end of May 2020, after experiencing some US$500 million in crude oil exports, Guyana only has access to US$944 million. The fact remains, despite being an oil economy with vast amount of oil exports, our foreign currency situation is no better today than it was in December 2014 when we had no oil exports.

With the kind consideration of your letter pages, I rest my case as I conclude, this Granger experiment was a colossal disaster and I am convinced that Mr. Granger and his team never had the expertise to provide the required real expansion needed to transform this economy. All the evidence today shows that there is no good life to be had with Team Granger and definite not any decade of development.

Yours faithfully,

Sasenarine Singh