Introduction

As promised last week, today’s column starts my review of Rystad Energy’s widely circulated results obtained from its modelling of the cost of delay for the Payara project. This project is based on the January 2017 crude oil discovery by ExxonMobil and its partners in the Stabroek Block. As reported, this is a high quality oil-bearing reservoir encountering more than 29 meters of oil bearing sandstone, drilled to 5,512 meters in 2030 meters of water. Based on ExxonMobil’s announcement, the Payara project will constitute the third producing reservoir; operating from a floating offshore production, storage and offloading vessel (FPSO). Crude oil production at Payara is targeted at 220,000 barrels of oil per day, at full ramp up, utilizing 45 supporting wells, including for production, water injection and gas injection.

This project follows on the already operational Liza 1 and Liza 2 projects, which as readers know are targeted to produce 120,000 barrels of oil per day at full ramp up. ExxonMobil’s original aim was to obtain approval for the Payara project last year, and to reach First Oil in 2023. At present the Payara project has not yet had governmental approval and the expectation is that First Oil from the project is now shifted to 2024!

Background

Readers need to remember that the focus of the present topic is to appraise the likely impact of the 2020 general crisis on Guyana’s infant oil and gas sector. That general crisis (as I have detailed it) has at least four core elements. First, there is a public health crisis — the COVID-19 global pandemic — starting in 2020, which has led to the collapse of global demand for crude oil and severe downward pressures on the market price for crude. Second, and independent of this health factor, analysts had, back in H2 2019, predicted a crude oil market contraction in 2020. Third, this expected market situation, had actually worsened this year, because of the OPEC (Saudi Arabia) “oil war” with primarily US shale oil producers.

Fourth, added to these three largely externally-induced events is the internal electoral and political crisis. This has delayed decision-making/approval for the Payara project. Decision-making has been also complicated, because the Liza 1 and Liza 2 projects had encountered regulatory, environmental and other problems associated with the start-up of crude oil production. These problems are concretized in the notorious failure of ExxonMobil’s compression system and its resort to the compensatory flaring of natural gas. The latter has led to strong public protestations over the adverse environmental consequences.

Risks and Uncertainty

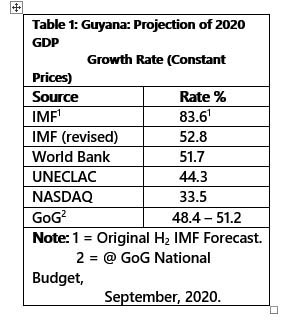

The negative outcomes indicated above have added to the risks and uncertainty, which confront Guyana’s infant oil and gas sector. I have argued before that, the cumulative effect of these negative outcomes, are broadly covered/captured in the forced downward revisions of Guyana’s GDP growth rate estimates for 2020, when compared to that originally predicted by the IMF/Guyanese authorities back in H2 2019. That rate, as readers have already been informed, was a whopping 83.6%. However, as 2020 has progressed that growth rate has been revised downwards by several other bodies. The most recent revision is provided in Guyana’s 2020 Budget. Here, the rate has been revised downward to a range of 48.4% to 51.2%. For convenience, I have updated an earlier Table carrying the several revised estimates of Guyana’s 2020 GDP growth.

The updated Table is presented below:

Rystad Model

In this Section, I introduce the results obtained from Rystad Energy’s modelling of the Cost of Delay at Payara. To begin with, two months ago (mid July 2020) Rystad Energy had claimed the Payara – Pacora “delays have already removed more than 50 million barrels of production that could have been achieved by 2030 if the project had been sanctioned in 2019”. The Rystad Energy modelling exercise confirms: “ExxonMobil has identified Payara as the third potential development prospect within the Stabroek block.”

As matters stand, ExxonMobil hopes the project is approved this year (2020), if not this month! Rystad Energy’s model assumes approval is given in H1, 2021 latest, and First Oil is then shifted to 2024, and is no longer 2023. For its modelling exercise, Rystad Energy calculates the cost of delay for four potential scenarios: a 3-month delay, a 6-month delay, a 12-month delay, and a 24-month delay.

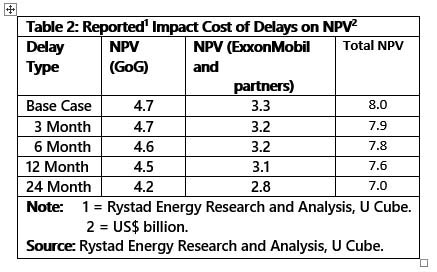

The results that I focus on, are Rystad Energy’s calculations of the Net Present Value (NPV) of the project and, separately, the NPV for Government revenue (income to the government) and the Company. Here, NPV is used standardly, as is done in capital budgeting and investment planning, in order to determine the profitability of an investment project. NPV is the difference between the present value of future cash inflows into the project and the present value of similar cash outflows from the project, over a specified period of time. In the case of crude oil, the time period used is the lifecycle of the project; that is, the five stages of oil projects, from exploration to abandonment/decommissioning.

Table 2 summarizes the NPV results, obtained by Rystad Energy in its modelling exercise:

Conclusion

Next week, I’ll evaluate these results pointing out both their strengths and limitations. As we shall observe, these outcomes centre on the central features of NPV analysis, namely: 1) the determination of the chosen scenarios; 2) the time value of money; and 3) the determination of private/social costs in a joint venture project, that is, a project that blends private and public enterprise.