Corruption devastates the lives of billions of people around the world, while its deadliness has become all the more evident during the COVID-19 pandemic and the climate crisis. With only ten years left to achieve the 2030 Agenda targets, we need decisive reforms to ensure that the resources needed to pay for critical public services such as schools and hospitals are not simply misappropriated and hidden away in tax havens or property markets abroad. Centralised, public registers of beneficial ownership as a global standard is precisely that kind of change.

Corruption devastates the lives of billions of people around the world, while its deadliness has become all the more evident during the COVID-19 pandemic and the climate crisis. With only ten years left to achieve the 2030 Agenda targets, we need decisive reforms to ensure that the resources needed to pay for critical public services such as schools and hospitals are not simply misappropriated and hidden away in tax havens or property markets abroad. Centralised, public registers of beneficial ownership as a global standard is precisely that kind of change.

Extract of petition sent to the UN General Assembly

Last Wednesday, Transparency International (TI) submitted a petition, signed by more than 700 organisations and individuals from 120 countries, calling on the United Nations General Assembly Special Session on Corruption (UNGASS 2021) to put an end, once and for all, to the abuse by anonymous companies and other legal vehicles that facilitate cross-border corruption and other crimes. According to the petitioners, these companies, which exist only on paper, exploit countries’ legal systems and conceal their ultimate ownership, resulting in the diversion of critical resources needed to advance sustainable development and collective security. Accordingly, they are calling for centralized public beneficial ownership registers as a global standard.

In our article of 14 December 2020, we reported TI as having identified three key issues that UNGASS 2021 needs to address urgently. Apart from the call for transparency in company ownership, TI stated that very often national justice systems are unable or unwilling to hold the powerful to account. In such a situation, corrupt high-level officials have an upper hand and act with impunity. In addition, it is not just enough to prosecute those who have been involved in corrupt behaviour. The assets stolen must be recovered for the benefit of the community that have been robbed.

On Friday, 12 February 2021, the Minister responsible for Finance presented to the National Assembly the Estimates of Revenue and Expenditure for the fiscal year 2021. Last week, the general debate on the Estimates began, and it is expected that the Assembly will resolve itself today into the Committee of Supply to consider and approve of the proposed allocations for the programmes and activities of Ministries/ Departments/ Regions as well as subsidies and contributions to the wider public sector entities.

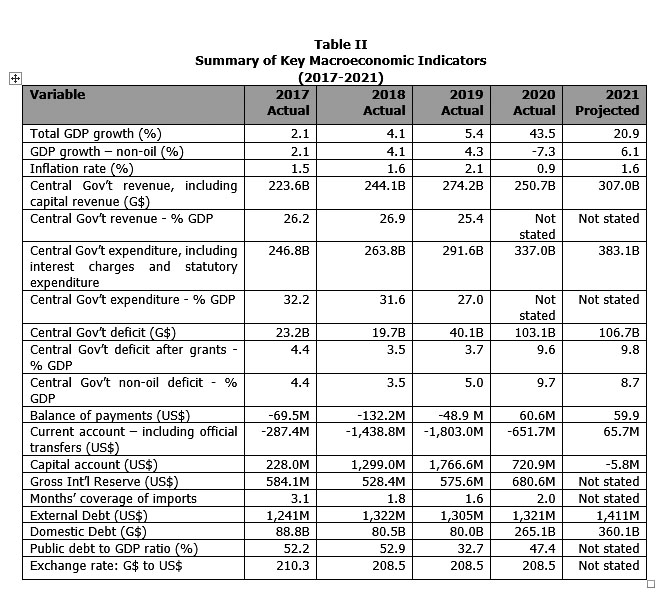

Last week, we began an examination of the performance of the economy in 2020 as contained in the Minister’s budget speech. The most important aspects are as follows:

Total real GDP growth was 43.5 percent. However, non-oil growth declined by 7.3 percent;

Inflation remained low at 0.9 percent;

Interest rate on small savings was 0.91 percent while the lending rate was 8.96 percent;

Total revenue was G$227.4 billion while total expenditure amounted to G$325.5 billion, inclusive of capital expenditure of G$76.1 million;

The fiscal deficit was G$90.5 billion, or 9.4 percent of GDP;

The balance of payments account reflected a surplus of US$60.6 million, compared with a deficit of US$48.9 million in 2019;

The current account deficit was reduced from US$1.803 billion to US$651.7 million;

The capital account surplus was reduced from US$1.766 billion to US$720.9 million;

Gross international reserve was U$680.6 million, representing two months of imports;

The total public debt (inclusive of publicly guaranteed debts and overdraft on the Consolidated Fund) was US$2.592 billion, representing a debt-to-GDP ratio of 47.4 percent; and

The exchange rate remained stable at G$208.5 = US$1.

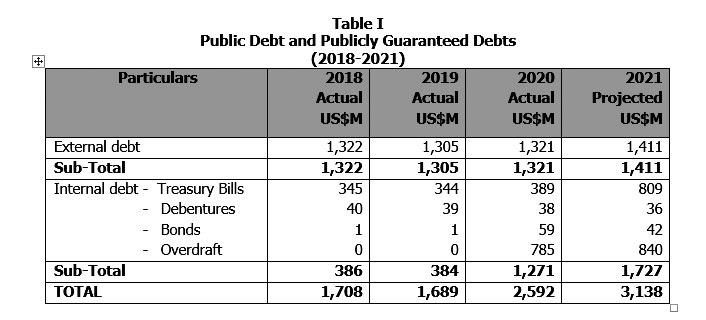

The Public Debt

We had stated that the amount of US$2.592 billion representing the total public debt as at the end of 2020, appears to have been understated when compared with the reported public debt at the end of 2019. Now that the Estimates for 2021 are on the Ministry of Finance’s website, the breakdown of US$2.592 billion has been provided, as summarized at Table I, with comparative

figures for the previous two years as well as projections at the end of 2021:

Prior to 2019, the proceeds from the issue of 182- and 364-days Treasury Bills were placed into the Monetary Sterilisation Account established in 1993 to remove excess liquidity in the financial system. According to the notes to the 2019 public accounts as well as those for the earlier years, the related liability should be exactly offset by the balance on this account, thereby creating a fully funded Liability. As of 2019, this policy had not changed, and it is not clear whether such a change took place in 2020. We therefore have to await the audited accounts for 2020 to confirm this.

Prior to 2019, the proceeds from the issue of 182- and 364-days Treasury Bills were placed into the Monetary Sterilisation Account established in 1993 to remove excess liquidity in the financial system. According to the notes to the 2019 public accounts as well as those for the earlier years, the related liability should be exactly offset by the balance on this account, thereby creating a fully funded Liability. As of 2019, this policy had not changed, and it is not clear whether such a change took place in 2020. We therefore have to await the audited accounts for 2020 to confirm this.

Despite this policy, in 2018 and 2019, the proceeds from these medium-term (182 and 364 days) Treasury Bills were deposited into the Consolidated Fund, thereby reducing the overdraft on the Consolidated Fund at the end of 2019 from an estimated G$213.006 billion to $G124.288 billion. Had the stated accounting policy been followed through, the overdraft at the end of 2020 would have been approximately G$289.9 billion, equivalent to US$1.386 million, instead of US$785 million shown in the above table. This explains our concern about the understatement of the total public debt as reflected in the Estimates.

The Ministry’s contention was that the Minister is empowered under the Fiscal Management Accountability (FMA) Act to seek funding by way of borrowing in order to reduce the overdraft on the Consolidated Fund; and the issue is more related to bridging a fiscal gap and has no relationship to monetary policy that falls under the remit of the Bank of Guyana. The Ministry cited Section 61 that stipulates that proceeds of any such borrowing by the Government shall be paid into the Consolidated Fund.

The Ministry, however, overlooked the fact that while Section 60 allows the Minister to approve of the use of advances in the form of overdraft on an official bank account to meet shortfalls during the execution of the annual budget, all such advances have to be repaid before the end of the fiscal year. That apart, contrary to the claim by the Ministry, the issuing of medium-term Treasury Bills has more to do with the monetary policy of mopping up liquidity, and not to finance budgetary shortfalls, hence the rationale for the creation of the Monetary Sterilisation Account.

It would seem necessary for the issuing of Treasury Bills, whether short-term (91 days) or medium term (182 and 364 days), to be revisited in the light of requirements of the FMA Act. The continuation of the use of the Monetary Sterilisation Account as a means of mopping up liquidity and to keep inflation in check also needs to be re-examined. Indeed, the perpetual use of Treasury Bills (as Bills mature and are redeemed, new Bills are issued) as well as access to overdraft facilities provided at the Bank of Guyana, provide every incentive for the Government to have deficit budgets instead of balanced budgets. At some stage, the bubble is likely to burst, and only oil revenue may save the day for us. For the period 2014 to 2020, the fiscal deficit totalled G$247.887 billion, giving an annual average of G$35.412 billion. The projected deficit for 2021 is G$106.7 billion

Targets for 2021

The economy is expected to grow by 20.9 percent, compared with 43.5 percent in 2020. However, non-oil growth is projected at 6.1 percent, compared with a decline of 7.3 percent in 2020. The assumption is that the economy will reopen and the COVID-19 pandemic restrictions are gradually lifted. The target rate of inflation is 1.6 percent.

The overall balance of payments is expected to reflect a positive balance US$59.9 million, slightly lower than that recorded in 2020. The current account balance is projected to move a deficit of US$651.7 million to a surplus of US$65.7 million due mainly anticipated higher export earnings. The capital account balance, however, is expected reflect a deficit of US$5.8 million, compared with a surplus of US$720.9 million in 2020. This is due to projected higher outflows from private enterprises compared with projected inflows from foreign investments.

Current revenue is expected to be G$257.9 billion, compared with G$227.4 billion in 2020, an increase of 13.4 percent. Total projected expenditure is G$366.9 billion, inclusive of capital expenditure of G$103.2 billion. In 2020, actual expenditure was G$325.5 billion. Therefore, the increase in the proposed expenditure is G$41.4 billion or 12.7 percent. The overall fiscal deficit is projected at 8.7 percent of GDP. The actual size of the budget, inclusive of interest charges as well as expenditures that are a direct charge on the Consolidated Fund, is G$383.1 billion.

Table II provides a summary of the key macroeconomic indicators for 2020, along with comparative figures for the previous three years as well as projections for 2021:

Budget measures for 2021

(a) The following are the budget measures announced by the Minister:

(b) Zero-rated VAT on basic food items and household necessities;

(c) Five percent reduction in water tariffs across the board;

(d) Zero-rated VAT on construction materials;

Five percent reduction in VAT for industrial grade cement;

(e) Increase in ceiling from $10 million to $12 million in respect of loans from commercial banks for housing;

(f) Increase in ceiling to $15 million in respect of loans from the New Building

Society for housing;

(g) Removal of VAT on ICT services for residential and individual use;

(h) Removal of VAT on ATVs for hinterland use;

(i) Introduction of cash grants of $15,000 per child attending nursery, primary and

secondary schools in the public school system;

(j) Increase in old age pension from $20,500 to $25,000 per month;

(k) Increase in public assistance payments from $9,000 to $12,000 per month;

(l) Exemption from capital gains tax for disposal of property over 25 years old; and

(m) Zero-rated VAT on imported goods/services and works by budget agencies.