Dear Editor,

Former Finance Minister, Winston Jordan, has presented his analysis about the country’s economic performance and economic policies. Jordan is contending that the economy did not grow in 2021, despite the mid-year report for 2021 revealing that the economy grew for the first half of the year by an estimated 14.5% while the non-oil economy grew by an estimated 4.8%. Jordan went on to justify his argument by stating that in 2020 there were many problems which were compounded by the Covid-19 pandemic and that “if you notice carefully the non-oil GDP of 4.8 at half-year, is same as the non-oil GDP in 2019.” Hence, according to Jordan, there was zero growth. This is a deliberate falsehood intended to mislead the nation. He also posited that the accounting system for the balance of payment transactions is flawed and therefore, the GDP growth rates are skewed. One should not have to remind Mr. Jordan that he presided at the Ministry of Finance and used the same GDP metric he now condemns to pomp up his performance, which was marred by high taxes and mismanagement of the economy. The former minister said that the GDP growth is also zero because inflation for the period was 5.6%, greater than the non-oil GDP growth. However, the inflation rate is owing to the effects of rising shipping costs and the global supply chain disruption, which we do not have any control over domestically. Further, the GDP growth rate reported is the real GDP versus nominal GDP. Jordan did not explain, which he ought to know as an economist, that real GDP is adjusted for inflation so the statement he made about inflation resulting in zero GDP is disingenuous.

Now, let’s dissect the midyear performance from another angle to test Jordan’s argument where he said that from the viewpoint position of 2019 to 2021, because of the contraction in 2020, there was no growth of the non-oil economy in 2021. In so doing, let’s look at the growth of the money supply for these periods. The reason why we are looking at the money supply is that the GDP metric essentially measures increased spending in the economy which includes government expenditure, consumption or household expenditure, private and foreign investments, and the country’s net export position. Increased spending is therefore measured by an increase in the country’s total money supply. As such, this will indicate if the statement Jordan made is indeed true.

Source: Midyear Reports, 2019 & 2021

From looking at the data illustrated in the table above, total money supply for half of 2019 grew by 9.51% compared to the half-year period in 2018, while total money supply for a similar period in 2021 only grew by 13.23% or by 3.79 percentage points higher, relative to the corresponding period in 2020. Net credit to the private sector grew by 5.75% in the 2019 half-year period relative to 2018, while net private sector credit grew by 4.86% in 2021 HY relative to 2020. However, when comparing the change in growth obtained in the 2021 half-year relative to the 2019 half-year position, net credit to the private sector grew 12.39% or by 6.64 percentage points. This is almost more than double the growth from 2019 during Jordan’s tenure. Put differently, if Jordan’s argument was true that there was zero growth (from 2019 to 2021), then the growth in the money supply from the 2019 period to 2021 would have been less than 5% or remained unchanged. But this was not the case. Henceforth, with these findings, it has been proven that Jordan’s argument is grossly false and misleading and should be put to rest.

Let’s examine the performance of the non-oil sectors as of June 2020, versus June 2021: The Agriculture, Forestry and Fishing industries contracted by 2.4%, compared with a decline of 4.1% during the same period (2021). This contraction was attributed to lower output from the other crops, sugar, forestry, and fishing sectors. Let’s recall we had a flood in Guyana that affected agricultural output and created significant damages to farmers and property. On the other hand, the rice and livestock sub-sectors grew by an estimated 7.8%, and 10.6% respectively. The Mining and Quarrying industries are estimated to have grown by 23.1%. This outturn was largely the result of higher output from petroleum and other mining activities, even though unexpected contraction was recorded for gold and bauxite. The manufacturing sector is estimated to have grown by 13.1% when compared to the corresponding (half-year) period.

The Services and Construction industries are estimated to have grown by 9.4% (2021) when compared to the corresponding period in 2020. This outturn was driven by increased output in wholesale and trade, administrative and support services, transport and storage, and financial and insurance activities. These sub-sectors grew by 34.3%, 9.1%, 16.2% and 7.3%, respectively. The construction sector also grew substantially by 25.5% when compared to the corresponding period in 2020. This was attributed to strong performance in both the public and private sectors.

GDP (2020) US$5.5b

Non-Oil GDP (2020) US$4.6b

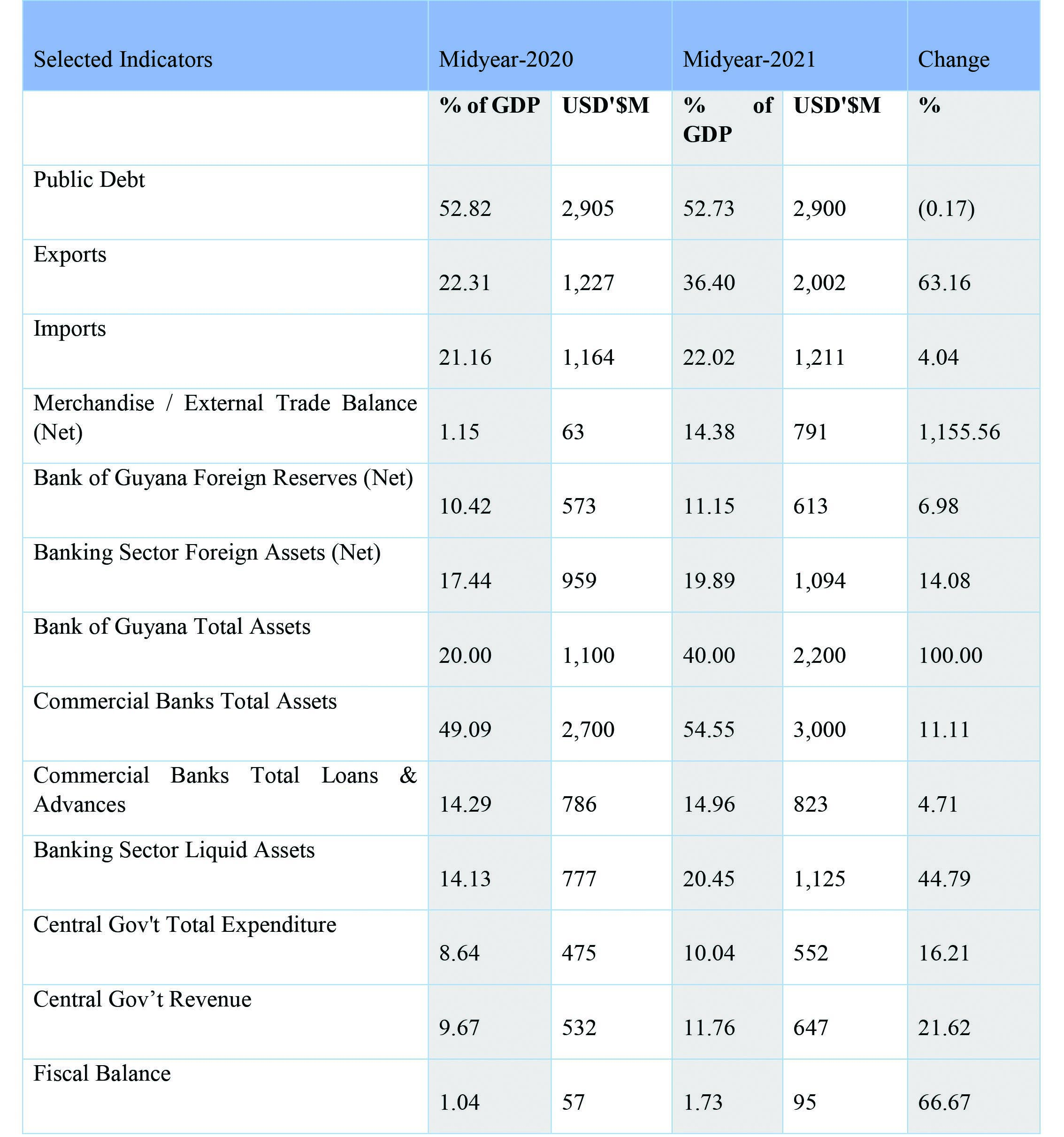

Explanation of the selected indicators illustrated in the above table:

● The total stock of public debt for the period under review represents 53% of GDP.

● Total exports for the mid-year 2021 period represent 36% of GDP which increased by 63% in comparison to the corresponding period in 2020.

● Total imports represent 22% of GDP and increased by 4% in comparison to the corresponding period in 2020.

● The trade balance surplus for the period ended June 2021 represents 14% of GDP and increased by 1,156% in comparison to the corresponding period in 2020. This is largely due to increased sales of the country’s share of crude oil.

● The International Foreign Reserves at the Bank of Guyana stood at US$613 million at the end of June 2021, representing 11% of GDP and increased by 7% when compared to the corresponding period.

● The net foreign assets in the banking system stood at US$1.01 billion which represents 20% of GDP and increased by 14% relative to the corresponding period in 2020.

● Bank of Guyana’s total assets stood at US$2.0 billion at the end of June 2021 representing 40% of GDP an increase by 100% relative to the corresponding period.

● Commercial banks’ total loans and advances stood at US$823 million, representing 15% of GDP an increased by 5% relative to the corresponding period in 2020.

● The liquid asset position in the banking sector stood at US$1.12 billion, representing 20% of GDP and which increased by 45% relative to the corresponding period in 2020.

● Central Government total expenditure at the end of June 2021 stood at US$552 million, representing 10% of GDP and increased by 16.2% relative to the corresponding period in 2020.

● Central Government revenue stood at US$647 million at the end of June 2021, representing 12% of GDP and which increased by 22% relative to the corresponding period in 2020.

● The fiscal balance for the period ended June 2021 stood at a surplus position of US$95 million, representing 2% of GDP and increased by 67% relative to the corresponding period in 2020.

For the 2021-year, expenditure in the agricultural sector increased to $22.6 billion from $18.4 billion in 2020. This went into supporting the growth of the industries, modernized facilities, drainage, irrigation, infrastructure, planting materials, production, equipment’s, to combat the damages done by the unprecedented rainfall and flooding that would have affected these industries along with those who are involved in the agricultural production. Some $350 million was allocated to support the ailing Forestry Commission, which was in financial ruin when the PPPC took office in August 2020; this institution is climbing out of its problems under our government’S intervention.

The 2021 half-year growth in the service sector was largely driven by increases in wholesale and retail trade, administrative and support services, transport and storage, and financial and insurance activities, which was a result of the relaxation of the COVID-19 measures that was put in place, such as the gradual reopening of the economy along with $535 million in support of the small business development, infrastructure, procurement and the cash grant initiative. In the manufacturing sector, the removal of VAT on machinery and equipment, exports and the amendment of the export policy has contributed to the growth. $53.5 billion was provisioned for the health sector to boost the capabilities, services, drugs, medical supplies and infrastructure to better serve the people. This included; supporting the rolling out of COVID-19 vaccines, critical medical equipment, remodeling, upgrading and operationalization of SMART hospital and strengthening emergency services.

The infrastructural development in new housing and existing housing schemes, low-income earners and young professionals were allocated house lots and homes across the country, underpinning the growth in the construction sector. Overall, the positive double-digit growth in GDP for 2020 and 2021 as well as non-oil GDP which contracted in the corresponding period, can be attributed to the fiscal and monetary measures in the National Budgets of 2020 and 2021 that were designed to help rebuild the traditional sectors and the economy at large, as well as to drive and stimulate new investment opportunities.

From a macro-prudential standpoint, the selected indicators as illustrated in the foregoing analysis, demonstrate a relatively sound and healthy economy. To this end, the country’s debt-to-GDP ratio is well below the universal benchmark, thus, indicating that Guyana has sufficient fiscal space to advance the country’s development agenda. The banking sector is also healthy from the indicators above and the international reserve position of the Bank of Guyana which is equivalent of three months import cover is also well within the minimum requirement from a macroprudential perspective. These outturns, altogether, are therefore suggestive that the monetary and fiscal policies and public investment programs administered through the respective national budgets yielded positive results in achieving a relatively healthy and stable economy. Finally, the former Finance Minister’s assertions on the mid-year performance are as usual indicative of his inability to comprehend elementary economics much less to venture into any real policy analysis.

Sincerely,

Deodat Indar

Minister (within the Ministry of Public Works)