If the long-term prospects for Venezuela’s oil industry remain uncertain as long as recovery and exports continue to be inhibited by a combination of United States sanctions and the reduced efficiency of the country’s oil infrastructure, recent reports suggests that a protracted period of drastic production decline has, just recently, been broken by a notable surge in production levels.

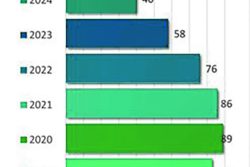

Earlier this month, S&P Global Platts, the international energy and commodities information provider, reported that Venezuela had produced 750,000 barrels per day (b/d) in December, reportedly its highest production volume in any single month since February 2020.

Venezuela’s increase in its oil recovery output last month is attributed largely to the support which the Maduro administration has been securing from Iran in the form of critical condensate necessary to dilute its ultra-heavy crude, recoverable mostly in the country’s operations in the Orinoco Belt.

Still, setting aside the US sanctions which continue to considerably inhibit the volume of Venezuela’s oil sales, steady incremental improvement in the performance of the country’s oil sector are also being affected by the reported continuing underperformance of the country’s state-run oil producer, PDVSA.

If analysts of the global oil industry do not appear to have written off the prospects for Venezuela being eventually restored to a position of being one of the world’s largest crude oil producers by 2030, the prevailing view is that in order to achieve this, the country will need to overcome significant hurdles, not least the condition of the state-run oil production infrastructure as much as it needs to find ways of dealing with the pressure of the sanctions. Both sets of circumstances are crucial to the longer-term prospects of country’s oil industry.

Analysts of the implications of Venezuela’s oil sector challenges assert that the badly-needed external investment which the Maduro administration needs in order to boost its efficiency is unlikely to be forthcoming given the risk of US sanctions that outside investors are likely to face.

Washington’s disposition towards the Maduro administration is reportedly largely determined by the pace of progress in dialogue between itself and its political opponents. Contextually, what has not helped is the relatively recent breakdown of talks between the two sides hosted by Mexico and equally importantly, what has become an aggressive oil trading arrangement between Venezuela and Washington’s arch-enemy, Iran.

Going forward, S&P Platts Analytics assessment reportedly points to Venezuelan oil production hovering around 600,000 b/d over the next year primarily as a result of indications that Washington intends to keep the existing sanctions in place.

Late last year Maduro announced that he intended to visit Iran soon to finalise new agreements and concretise existing ones in areas of cooperation which will presumably include further Iranian support for Venezuela’s oil industry, a circumstance that gives rise to speculation as to whether Washington is not likely to react badly to outcomes from the visit that appear likely to seek to further cement ties between its number one enemy in the Middle East and a country in what, geopolitically, it regards as its backyard.