Your right is to perform of your prescribed duties but you are not entitled to the fruits of your actions. Never consider yourself the cause of the results of your actions, and never be attached to not doing your duties. Perform your duties equipoised, abandoning all attachment to success or failure.

Bhagavad Gita

When considering the effects of global warming and climate change, countries tend to focus mainly on carbon dioxide emissions. However, this alone cannot prevent global temperatures from rising above pre-industrial levels by 1.5°C. A new study from Duke University indicated that countries also need to focus on other greenhouse gases, such as methane, nitrous oxide, black carbon soot, low-level ozone and hydrofluorocarbons. If this is done, global warming could be halved by 2050, as these other gases contribute as much to global warming, which could potentially cause temperatures to exceed the 1.5°C level by 2035 and the 2°C by 2050. See https://nicholas.duke.edu/news/curbing-other-climate-pollutants-not-just-co2-gives-earth-chance.

Seven weeks ago, the National Assembly approved an amendment to its Standing Orders to provide for five of the nine members of the Public Accounts Committee (PAC) to form the quorum for meetings: two from the Government side, two from the Opposition and the Chairperson. Previously, three members constituted the quorum, and this was the practice since 1963. Last Tuesday, Opposition PAC member, Ganesh Mahipaul, stated that the previous day’s statutory meeting of the Committee had to be aborted because of the absence of Government members. The advisors to the Committee – Finance Secretary, Accountant General and Auditor General – were also absent; while all four Opposition members were in attendance, two virtually and two physically. Mr. Mahipaul further stated that the Clerk of the Committee informed the members in attendance that the Government members asked to be excused due to the flood situation in Region 9.

The fact that the Opposition members turned up for the meeting would suggest that they were not aware of the unavailability of the Government members. If this is the case, was it an oversight by the Clerk not to have informed those members prior to the meeting? Or, could be that the information was not conveyed to the Clerk in time to enable him to inform the Opposition members? And how did the Audit Office, an independent constitutional agency, know that there was not going to be any meeting? We hope that the Clerk would provide some clarification as to what really happened.

Mr. Mahipaul claimed that the meeting could have been held since three of the five Government members are not Ministers and are in no way involved in the work of the Civil Defence Commission which was responsible for assessing of the flood situation in Region 9. The claim was, however, disputed by a Government member who indicated that, apart from the flood situation, there were other reasons for the non-attendance of Government members. The last report of the PAC was in respect of the years 2012-2014 and was issued some five years ago. The Committee is currently examining the public accounts for the combined years of 2015-2018. It is not clear when such examination will be concluded and the related report issued. This should be viewed against the background that the 2019 and 2020 public accounts are awaiting the PAC’s examination, and at the end of September, the accounts for 2021 will be ready for presentation to the Assembly. Therefore, another year will be added to the Committee’s backlogged work.

In last week’s article, we began a discussion of Guyana’s public debt at the end of 2020 which stood at G$415.153 billion, compared with G$388.698 billion at the end of 2019, a net increase of G$26.698 billion. Today, we conclude our discussion on the subject.

External debt

The external debt increased from US$1.287 billion to US$1.303 billion. This was mainly due to: (i) re-statement of the opening balances on two loans; (ii) repayments on balances on existing loans amounting to US$52.918 million. (iii) disbursements on existing loan agreements totalling US$48.535 million; and (iv) accrued interest on Non-Paris Club loans of US$765 million.

During 2020, four new loan agreements valued at US$71.073 million were entered into, one of which was from the Islamic Development Bank for US$14.630 million for the construction of a small hydro project. The agreement was entered into on 8 June 2020 but no disbursement had been made as at the end of 2020. We had stated on several occasions that in principle no new agreement that had the effect of binding the State should have been entered into between the date of the no confidence vote and the announcement of the results of the elections, due to the caretaker status of the Government. The agreement was nevertheless tabled in the Assembly on 23 December 2020. However, in view of the present Administration’s decision to resuscitate the Amaila Falls Hydro Project, it is unclear whether the project will proceed.

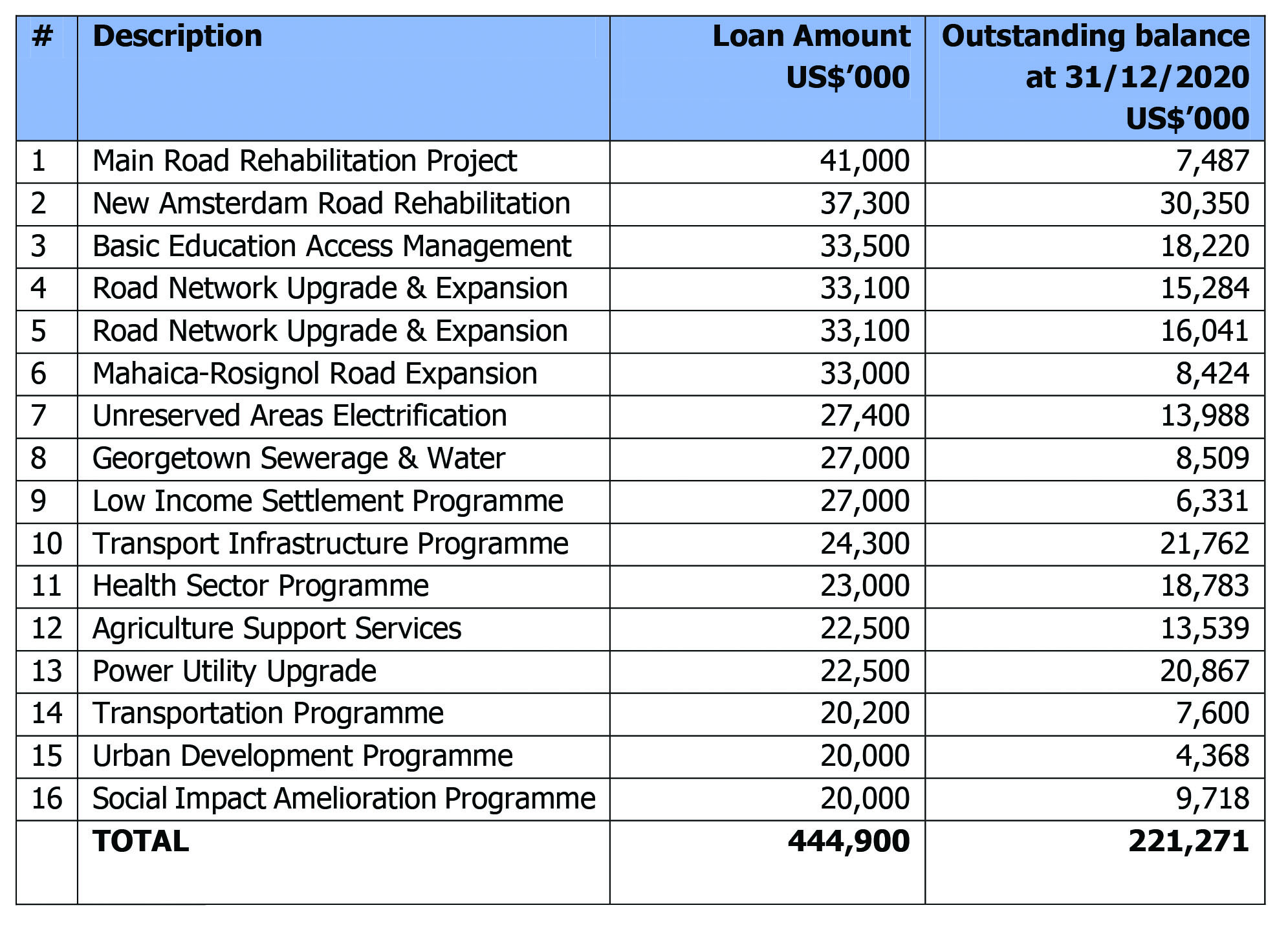

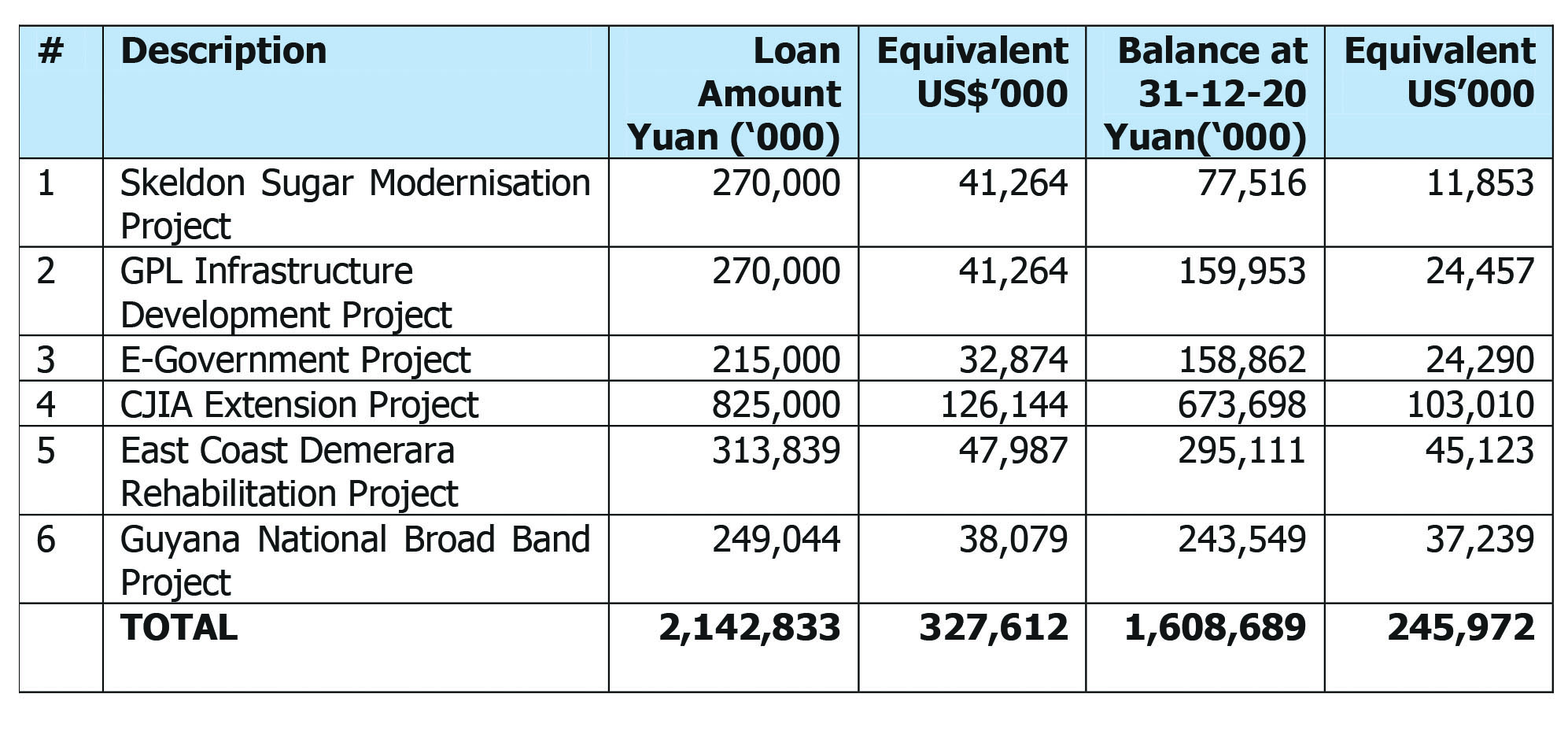

Guyana’s largest external creditor is the Inter-American Development Bank (IDB) with 77 loans with outstanding balances totalling US$552.1 million or 42.4 percent of the external loan portfolio. Table I provides a list of 16 of the largest loans from the IDB. The China Exim Bank is the second largest creditor with six loan loans with outstanding balances totalling US$245.972 million, or 18.9 percent of the external loan portfolio. These loans, which were the subject of discussion in a previous article, are shown at Table II.

Table I

List of IDB loans

(US$20 million and over)

Table II

Table II

List of loans from the Exim Bank of China

Last week, the Government entered into a contract for the design and construction of the new Demerara Harbour Bridge in the sum of US$260 million. The contract was awarded to China Railway Construction Company Ltd (CRCCL) in a joint venture with two other Chinese companies. The agreement, however, does not have implications for the public debt as the Government is financing the cost of the project. In this regard, an amount of G$21.1 billion has been allocated in the 2022 Estimates for the project.

The original proposal was for the bridge to be constructed either under Design, Finance and Build (DFB) model or under the Build, Owned, Operated and Transfer (BOOT) arrangement. The latter involves the contractor providing the funding for not only the construction costs but also for those relating to operations, maintenance and financing over a 20-year period after which the bridge is transferred to the Government free of cost. The contractor then recoups its costs plus profit via the charging of tolls to commuters using the bridge. We had stated on several occasions that the BOOT arrangement is significantly more expensive, compared with government funding. It is therefore good decision for the Government to fund the cost of the bridge, considering the mistake it had made in relation to the Berbice River Bridge.

In November 2020, the Ministry of Public Works invited Expressions of Interest (EOIs) for the construction of the bridge based on the DFB or the BOOT arrangements. However, given that the financing is now being met from government resources, it has been argued that the EOIs should have been re-advertised as this was likely to attract a wider pool of contractors from which the selection of the lowest evaluated bid is made. It was subsequently learnt that the Government ended negotiations with CRCCL whose a bid was US$256.6 million, on the ground that the financing cost was too high. The Government then entered into negotiations with a consortium of Chinese companies, the final outcome being the award of the contract in the sum of US$260 million.

Section 31 of the Procurement Act provides for the application of a two-stage tendering approach where it is not feasible to formulate detailed specifications due to the complex nature of the contract. During the first stage, suppliers/contractors are invited to submit technical proposals based on a conceptual design or performance-based specifications, without submitting prices. During the second stage, they are invited to submit final technical proposals with prices on the basis of the tender documents, as revised following the first stage. It is not clear whether these procedures were followed. Section 41, however, prohibits negotiation between the procuring entity and any of the bidders, except in the case of consulting services, as provided for by Section 51.

Of interest also, is the proposal to engage another Chinese company, China Railway First Group, to construct the Amaila Falls Hydro Project using the BOOT arrangement. It was the same company that was earmarked for the construction before the APNU+AFC Administration aborted the project. We hope that the present Administration will reconsider its decision to use the BOOT model for this project, considering the large inflow of oil revenues in the coming years that could be used to finance the project.

There are three other external loans with outstanding balances that are worthy of mention: Caribbean Development Bank (CDB) – US$149.470 million; Venezuela (Petro Carib) – US$104.933 million; and Republic Bank of Trinidad & Tobago – US$14.999 million. The CDB loans are mainly in relation to road rehabilitation and sea defence works; while the loans from Venezuela relate to the purchase of fuel, part of which is offset by shipments of rice to that country. The liability to the Republic Bank is in relation to the loan that Atlantic Hotel Inc. had taken for the construction of the Marriott Hotel and for which the Government has since assumed responsibility.

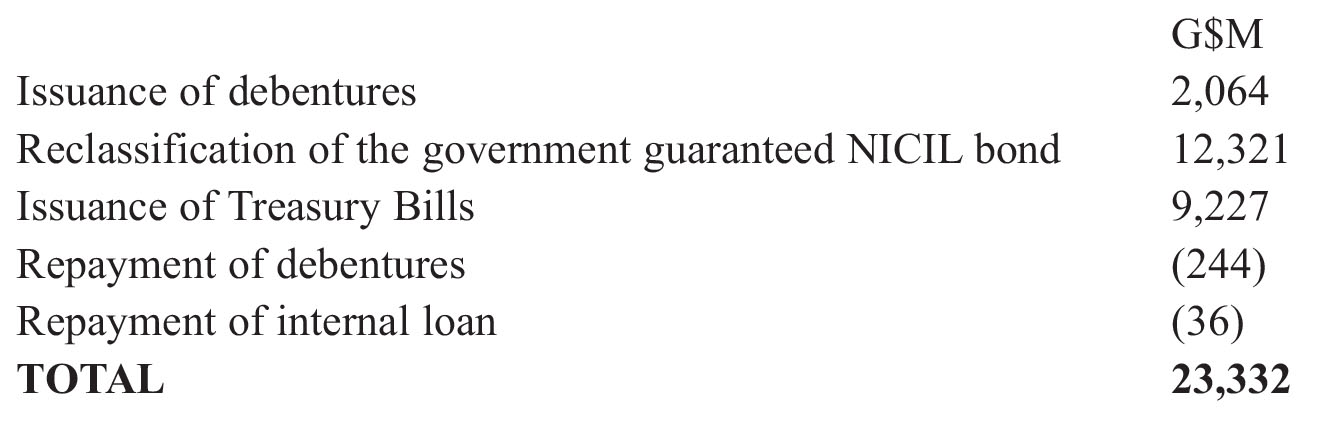

Internal Debt

The Internal Debt at the end of 2020 was G$143.428 billion, compared with G$120.096 billion at the end of 2019, an increase of G$23.332 billion. This was due mainly to the following:

In relation to (b), in view of NICIL’s inability to repay the debt incurred for the restructuring of the GUYSUCO, the Government has taken over the liability.

Debt servicing costs

The debt servicing costs for 2020 by way of interest charges amounted to G$6.243 billion, compared with G$5.870 billion for 2019. Interest charges relating to the external loan portfolio amounted to G$4.925 billion, equivalent to US$23.622 million. Given the expected large flow of oil revenues, consideration should be given to liquidating some of the debts, as there will be a reduction in debt servicing costs.

Debt-to-GDP ratio

A standard measure of debt sustainability is the debt-to-GDP ratio. A high ratio is undesirable, as a higher ratio indicates a higher risk of default in servicing the public debt. A World Bank study indicates that a ratio that exceeds 77 percent for an extended period of time may result in an adverse impact on economic growth.

At the end of 2020, the debt-to-GDP ratio, inclusive of publicly guaranteed debts, was 47.3 percent, compared with 32.6 percent at the end 2019, an increase of 14.7 percent. The non-oil debt-to-GDP ratio was 56.2 percent, compared with 33.2 percent at the end of 2019, an increase of 23.0 percent. These increases were due mainly to the inclusion of the overdraft on the Consolidated Fund as part of domestic debt as well as the transfer of NICIL bonds as a Government debt. (Source: Public Debt Annual Report 2020 found at https://finance.gov.gy/wp-content/uploads/2021/05/Public-Debt-Annual-Report-2020-The-Cooperative-Republic-of-Guyana.pdf.) According to a note to Appendix 22 of the report, the GDP rebased series at 2012 prices was used to calculate the ratios.