Last week, we concluded our discussion on the 2021 Report of the Auditor General as it relates to central government activities. Article 223 of the Constitution defines the public accounts to include not only central government entities but also local government bodies and entities; bodies in which controlling interest vests in the State; and all projects funded by way of loans and grants from a foreign State or organization.

Last week, we concluded our discussion on the 2021 Report of the Auditor General as it relates to central government activities. Article 223 of the Constitution defines the public accounts to include not only central government entities but also local government bodies and entities; bodies in which controlling interest vests in the State; and all projects funded by way of loans and grants from a foreign State or organization.

Non-central government activities are perhaps in greater need of scrutiny, considering the vast amounts of financial resources allocated to these entities via the national budget, coupled with the fact that the accountability framework is not as comprehensive as that of central government. In the case of the latter, the National Assembly goes through a rigorous process before approving the budgets of Ministries, Departments and Regions on a programmatic basis and by line items. Additionally, there are strong constitutional provisions, elaborated on by the Fiscal Management and Accountability (FMA) Act as well as detailed rules, regulations and procedures to be followed in the incurrence of public expenditure. In particular, all budget agencies are required to adhere to the requirements of the Public Procurement Act in the award of contracts for the acquisition of goods, services and the execution of works. Further, the Public Accounts Committee scrutinises the audited public accounts.

Admittedly, all is not well in relation to the activities of Central Government, as major violations and deviations have occurred over the years, as successive reports of by the Auditor General will attest, without sanctions being imposed on the culpable officials.

In today’s article, we discuss our latest assessment of the state of financial reporting and audit of these other bodies that comprise the wider public sector. We will consider them under the following classifications: municipalities; neighbourhood democratic councils (NDCs); public enterprises; statutory bodies; and foreign-funded projects.

Municipalities

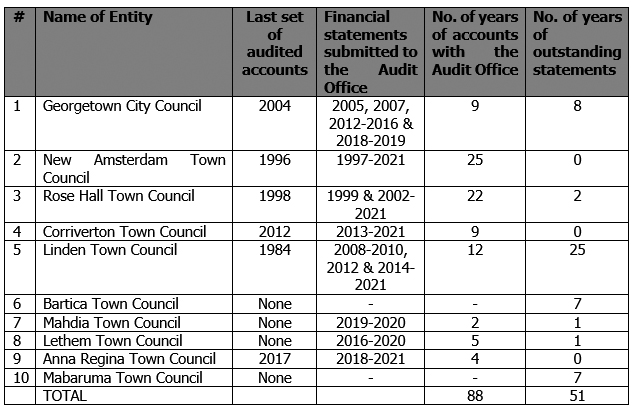

The Municipal and District Councils Act, Chapter 28:01, requires the Treasurer of a municipality to prepare and submit to the Auditor General annual financial statements within four months of the close of the year and for those accounts to be audited as soon as practicable. In 2021, the ten municipalities received amounts totalling $111 million as subventions from the national budget through the Ministry of Local Government and Regional Development. However, they continue to be in significant arrears not only in financial reporting but also in relation to their audits, as shown at Table I:

Table I

Status of financial reporting and audit of municipalities

as of September 2022

Only three municipalities are up to date in their submission of financial statements to the Auditor General. Of the remaining seven, a total of 51 sets of financial statements were outstanding as of September 2022, with the Linden Town Council topping the list with 25 years outstanding.

Only three municipalities are up to date in their submission of financial statements to the Auditor General. Of the remaining seven, a total of 51 sets of financial statements were outstanding as of September 2022, with the Linden Town Council topping the list with 25 years outstanding.

A total of 88 sets of financial statements were with the Audit Office waiting to be audited and reported on, which is a most unfortunate situation. In his 2005 report, the Auditor General stated that the Audit Office received financial statements for the Georgetown City Council and Rose Hall Town Council for the years 2005-2006 and 1990-2006, respectively. Although the accounts for subsequent years for these two municipalities were submitted, the audits have not progressed since then. A similar observation, in varying degrees, is made in respect of the six other municipalities. In 2021, the audit of the accounts of Corriverton Town Council was finalized for the years 2002-2012 and for which disclaimers of opinion were issued.

It is evident that the audit of municipalities has not been assigned the priority it deserves. The respective councils responsible for managing the affairs of these entities are also not devoid of blame for not pressuring the Auditor General to have their accounts audited in a timely manner in order to discharge their financial stewardship responsibilities. And what of the Ministry of Local Government and Regional Development in relation to monitoring the affairs of the municipalities to ensure that they discharge their accountability responsibilities? Does the Minister also not have a responsibility, considering that the Act requires the Auditor General to submit to him a copy of the audited accounts within one month of the completion of the audit? The Minister’s responsibility also extends to situations where appeals are made against any surcharge made by the Auditor General.

On several occasions, we raised the matter of the Auditor General receiving several years of financial statements together for a particular entity. The normal practice is for one year’s accounts to be submitted, audited and reported on before the submission of the following year’s accounts. The reason for this is that following the audit, the closing balances of one year are carried forward as the opening balances for the next year, and in many cases these closing balances have to be adjusted.

Neighbourhood Democratic Councils

In 2021, the 70 NDCs received amounts totalling $418.288 million from the national budget as subventions, giving an average of $5.976 million per NDC. These entities are governed by the Local Government Act which has financial reporting and audit requirements similar to those of municipalities. However, a review of the Auditor General’s reports over the years indicates most of these entities are also significantly in arrears in terms of financial reporting and audit. According to the Auditor General, 40 NDCs did not submit financial statements for the years 2017-2020.

In 2021, the Auditor General issued 29 audit reports for eight NDCs. However, no reports were issued in 2020; while for 2019 only four NDCs were audited and reported on for periods varying from 2010 to 2018. For 2018, audit reports for five NDCs were issued again for varying periods; while for 2017, audit reports for 17 NDCs were issued. In most cases, the Auditor General issued qualified opinions on the accounts.

The following can be gleaned from the 2021 Auditor General report:

(a) Eight NDCs did not submit financial statements for audit since they were established;

(b) Two NDCs were last audited up to 1994. Financial statements were not submitted for audit for 1995-2021 for one NDC, while for the other, the Audit Office received financial statements for the years 2008-2014 only;

(c) All the other NDCs submitted financial statements for audit for varying periods, some of which contained gaps in financial reporting; and

(d) As in the case of municipalities, several years of financial statements were with the Audit Office either waiting to be audited, or the audits were yet to be finalized and the related reports issued.

(e) Given the above, our comments on the state of financial reporting and audit of municipalities are also relevant to the NDCs.

Public enterprises

There are 39 entities that comprise public enterprises. These entities are required to have their audited accounts presented to their subject Ministers for laying in the Assembly within nine months of the close of the fiscal year. However, only three entities were up to date in terms of financial reporting and audit: Guyana Power and Light, GUYOIL and GUYOIL Aviation Services Inc.

According to the 2021 Auditor General’s report, of the 19 audits that were finalised for 14 entities, 17 were executed under a contracting out arrangement with Chartered Accountants in public practice. Four were given disclaimers of opinion, while the accounts of five entities were qualified. The Auditor General did not identify the entities that failed to have their accounts audited in a timely manner. Nor was there any mention as to how many draft accounts were still with the Audit Office and what was the status of these audits.

Recently, the Government announced its intention to sell the Marriott Hotel which is owned by Atlantic Hotel Inc. (AHI). The National Industrial and Commercial Investments Limited (NICIL) is the parent company of AHI. In response to a Stabroek News enquiry, the Auditor General had stated that the audits of AHI’s accounts for the last five years, i.e. 2016 to 2021, were on-going and that the process was delayed because the relevant documents requested from NICIL were not presented. Several stakeholders have called for the release of the audited accounts of the Hotel in the light of the recent advertisement inviting expressions of interest to purchase the Hotel.

Sections 107, 154 and 346 of the Companies Act require: (i) the audited accounts of companies to be presented to the shareholders at the annual general meeting at least once every calendar year but not later than 15 months after the holding of the last meeting; (ii) annual returns to be submitted to the Registrar of Companies within 42 days of the holding of such meetings; and (iii) in the case of government companies, the audited accounts to be presented to the Minister within six months of the close of the financial year and for those audited accounts to be laid in the Assembly within nine of the close of the financial year. There are also penalties for non-compliance with these requirements, in addition to the risk of being struck off the Register of Companies for failure to submit annual returns.

In May 2018, NICIL issued bonds in the sum of G$30 billion to assist in the restructuring of the Guyana Sugar Corporation (GUYSUCO), of which G$16.5 billion was drawn down. The duration of the bonds was for five years, with the Government guaranteeing repayment, and eventually assuming the debt. Additionally, the assets of the Skeldon Sugar Modernisation Project, along with other assets of the closed sugar estates, have since been transferred to NICIL in keeping with a Vesting Order signed by the then Minister of Finance. However, an examination of the Auditor General’s reports indicates no evidence of NICIL’s accounts being audited beyond 2013.

According to GUYSUCO’s website, the Corporation was last audited to 2018, and the related report was issued in June 2021. As of September 2022, it was three years in arrears in having audited accounts. The Corporation has been in receipt of massive sums from the Treasury to assist in the financing of its operations. Despite incurring significant losses over the years, all indications are that it will continue to receive funding from Central Government for the continuation of its operations. In contrast, Barbados has recently decided to begin the privatization of its sugar industry which has become a financial burden on the country’s Treasury, with some US$30 million in subsidies annually. See https://www.plenglish.com/news/2023/01/05/barbados-will-begin-privatization-of-sugar-industry/.

Statutory bodies

A total of 61 entities comprise statutory bodies which are entities created under special acts of Parliament. These entities are also required to have their audited accounts presented to their subject Ministers and laid in the Assembly within nine months of the close of the fiscal year. In 2021, a total of 53 audits were finalized in respect of 35 entities, 12 of which were undertaken by Chartered Accountants in public practice. However, only seven entities were up to date in terms of having audited accounts.

Foreign-funded projects

Foreign-funded projects that require separate financial reporting and audit include those funded by the Inter-American Development Bank, International Development Agency, Caribbean Development Bank and the United Nations Development Programme. The financial reporting and audit of these projects are up-to-date mainly because one of the conditionalities is for audited accounts to be produced within a specified timeframe. There is also rigorous monitoring by the funding agencies to ensure compliance. In 2021, the Auditor General issued 29 audit reports in respect of foreign-funded projects. These did not include loans from the Exim Bank of China and the Exim Bank of India since there are no contractual arrangements for separate financial reporting and audit of the related projects. Several of the related projects financed from these loans had significant cost and time overruns and failed to deliver in terms of their objectives, outputs, outcomes and impacts.

Conclusion

As stated in previous articles, financial reporting and auditing of non-central entities have been badly neglected over the years. In this regard, heads of budget agencies, subject Ministers and the PAC have a role to play in ensuring that the entities involved are fully accountable and in a timely manner for the use of public resources. For his part, the Auditor General should consider utilizing more of the services of Chartered Accountants in public practice with the aim of bringing financial reporting and audit of non-central government entities to some measure of respectability.

It should not be over-emphasised that public accountability cannot be considered as having been fully discharged unless all entities comprising the public accounts are up to date in terms of financial reporting and audit. When are we going to see this happening is anyone’s guess!