Former Pakistani Prime Minister Imran Khan was sentenced to three years’ imprisonment on corruption charges. He was found guilty of not declaring money earned from selling gifts he received while in office. The gifts, reportedly worth more than US$635,000, included Rolex watches, a ring and a pair of cuff links. As a result of the verdict, Mr. Khan has been barred from running for political office for the next five years. He is expected to appeal his conviction. A former Pakistani test cricketer and captain, Mr. Khan was elected in 2018, but was ousted in a no-confidence vote last year after a falling-out with Pakistan’s military. He is currently facing more than 100 charges since his removal from office, charges which he considers to be politically motivated. See https://www.bbc.com/news/world-asia-66414696.

Last week, we began a discussion of the main points of the 2020 annual report of the Guyana Extractive Industries Transparency Initiative (EITI), the fourth report of its kind since Guyana became a member of the EITI in October 2017. One of the requirements of EITI Standard is the publication of an annual report indicating, among others, how licences are allocated; how much tax and social contributions are being paid and where they end up in the government; and how much revenue is being generated, where it ends up and who it benefits.

As in the case of the previous reports, the 2020 report is a very lengthy one, with 196 pages of narrative, inclusive of 110 tables, 50 lists of figures, and 14 annexes. It consists of seven chapters: (i) Executive Summary; (ii) Approach and methodology; (iii) Contextual information on the extractive sector; (iv) Defining the reconciliation scope; (v) Revenues collected from in-scope companies; (vi) Analysis of reported data; and (vii) Implementation status of EITI recommendations.

So far, we have covered three key areas, namely revenues generated from the extractive sector; production data; and completeness and reliability of data. In today’s article, we conclude our discussion of the remaining parts of the report.

Reconciliation of cashflows

The total amount of revenues generated from the extractive industries was $93.77 billion. After adjustments and reconciliation, a net amount of G$1.53 billion remained unreconciled, representing 1.90 percent of revenues. In 2019, the unreconciled difference was $2.95 billion, or 7.04 percent of revenues.

The unreconciled revenues were mainly due to: (i) companies declaring payments totalling $1.05 billion that were not reported by government agencies, including the Guyana Geology and Mines Commission (GGMC) and Guyana Revenue Authority (GRA) for the amounts of $490 million and $470 million, respectively; and (ii) companies not reporting taxes amounting to $2.58 billion that were received by the GRA. These payments could not be reconciled with the government records for various reasons, including: (i) the absence of receipt numbers and lack of disaggregated amounts; (ii) the use of accrual accounting by companies; and (iii) the deadlines for submission of the required data being too short for some companies.

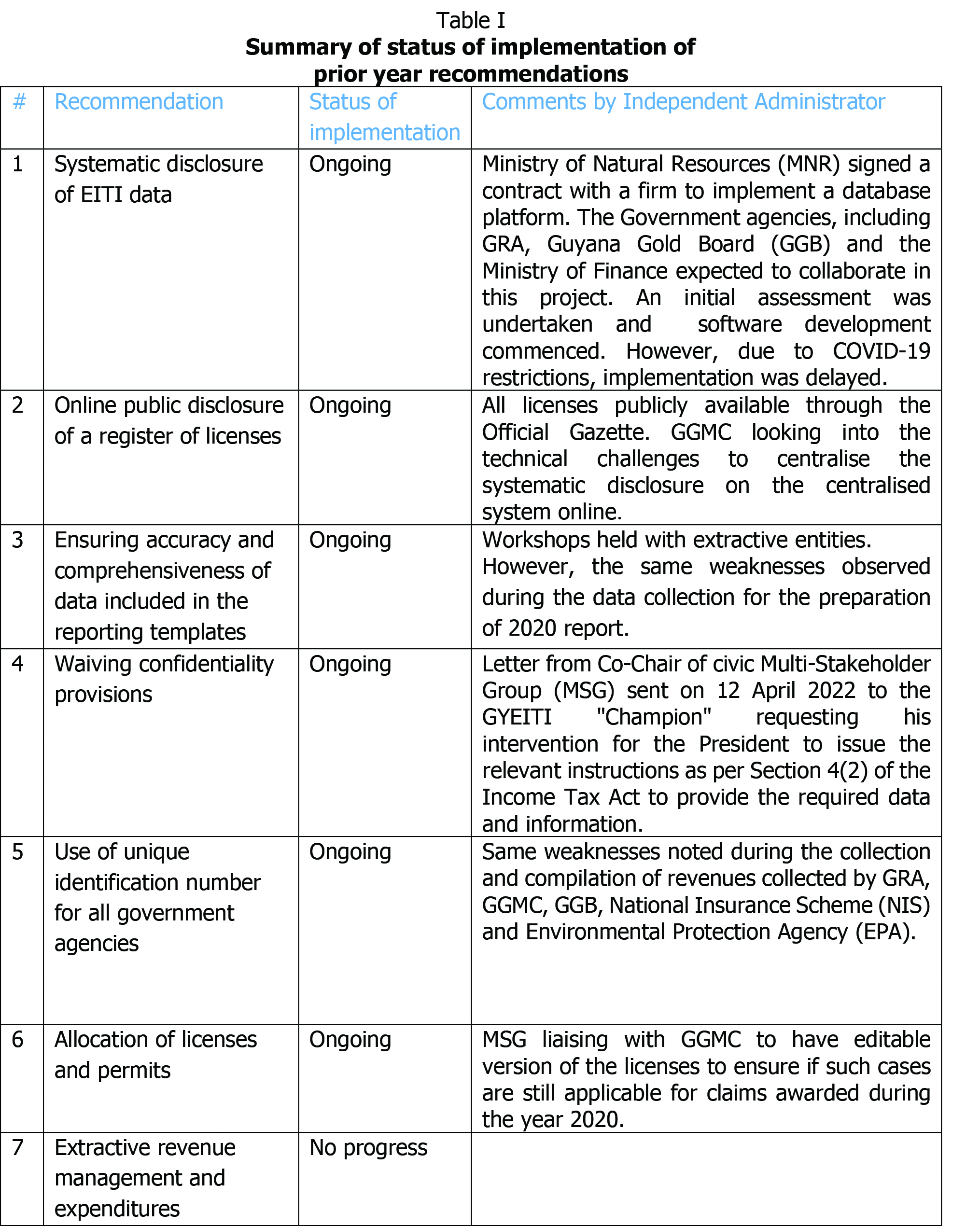

There were 14 specific recommendations made under the above categories. These are as follows:

Systematic disclosure of EITI data

(a) Set up a roadmap on the implementation of an open data that centralises all EITI data;

(b) Implement and upgrade a cadastral system with adequate details such as data about the legal ownership, the beneficial owners of the companies, corresponding export and production details of companies;

(c) Enhance the current management information systems of the Government agencies involved in the EITI process in order to allow, among other benefits, systematic publication of the required EITI data.

Public disclosure of register of licences

(d) GGMC to ensure that the link to the online cadastre is kept functional and up to date, and all data on licenses to be systematically recorded therein;

(e) The register of licenses and permits to include Taxpayers Identification Numbers (TINs) of current license holders to facilitate corroboration of data on payment as well as communication between Government agencies.

Reporting templates

(f) Build capacity of the reporting entities to raise their awareness on the importance of the EITI data they provide and ensure that due care and attention is paid during the preparation of reporting templates;

(g) Distribute reporting templates well in advance to allow reporting entities to prepare, sign and certify them.

Waiving confidentiality provisions

(h) The MSG to set out a roadmap with the relevant Government agencies to amend the Revenue Authority Act (1996) and the Income Tax Act (1929) to remove any confidentiality constraints and to allow the public disclosure of data relevant for EITI reporting;

Unique identification numbers

(i) Government agencies, in particular, GGMC, GGB, NIS and EPA to keep records of the TINs as required by the Income Tax Act (2019) rather than using names or different reference numbers for identifying taxpayers.

(j) The MSG to study existing revenue collection system and recommend to the MNR the use of a unique identification numbering order for all Government agencies;

Allocation of licences and permits

(k) Develop policy for GGMC to conduct an inventory of the active permits and licenses in order to include the clear definition and distinction between large scale licenses and medium scale permits. The policy should consider whether the combined acreage of the permits when awarding them to the same applicant, especially when these relate to continuous plots;

(l) GGMC to apply a tendering process for awarding mineral agreements to ensure that any risks of failure by the investor is mitigated and that the Government benefits from the most advantageous offers. This will also assist in addressing the under-exploitation of mining licenses covering large plots by investors who may not have the required technical and financial capacities;

Revenue management and expenditures

(m) Government agencies, in particular, Ministry of Amerindian Affairs and the GGMC to implement automated controls to ensure the comprehensiveness of extractive revenues earmarked to be transferred to Amerindian Development Fund; and

(n) The MSG to set up a work plan with the GGMC, Guyana Forestry Commission and the Department of Fisheries to consider any extractive revenues that should be earmarked for specific programmes or geographic regions.

The 2019 report had included another prior year category of recommendations relating to the public disclosure of mineral licences for which no progress had been made. The specific recommendation requires the MSG to set out a short term work plan for the electronic publication of all mineral agreements in the mining sector. The work plan is to include: (i) defining how the electronic publication of mineral agreements can be undertaken; (ii) the steps required for all mineral agreements to be published electronically and how to make these accessible to the public; (iii) a realistic short-term timeline as to when such data could be available; and (iv) performing a review of the institutional or practical barriers that may prevent such electronic publication.

Recommendations made in the 2020 report

The 2020 report contains three additional recommendations: These are:

(a) The MSG to review all data/reporting templates to allow for data reporting by companies/agencies at the disaggregated levels and ultimately to present up-to-date reporting;

(b) Data templates to be modified to incorporate the payment/revenue collection system, to be included in the proposed terms of reference for the 2021 report; and

(c) The MSG to engage the Bureau of Statistics and other relevant agencies to address data classification and coding of employment by gender, sector, and the declassification of agriculture, fisheries and forestry.

Conclusion

The first three annual reports highlighted significant deficiencies and instances of non-compliance with the EITI Standard. These had led the Independent Administrator to conclude that he was unable to determine that: (i) all significant contributions made by extractive entity to the revenues of Guyana were included in the reports; and (ii) the financial data submitted by reporting entities and included in the report, were subject to audits that have been performed in accordance with international standards. However, although the findings contained in the 2020 report were substantially the same as those contained in the three previous reports, the conclusions drawn were significantly different from those of the previous years. In particular, the Independent Administrator has now stated that he was able to conclude that the 2020 report covers all significant revenues made by extractive entities to the revenues of Guyana and that the significant revenues declared by reporting entities were subject to audits that have been performed in accordance with international standards.

Most of the prior year recommendations could be traced to the first annual report. It is therefore disappointing that after four years little or no progress has been made to ensure their full implementation. In fact, the 2019 report had concluded that continued inaction on some of the recommendations previously made: (i) stymies progress in meeting the requirements of the EITI Standard; (ii) impedes preventative actions to correct and address discrepancies between declarations by government agencies and the extractive entities; (iii) adversely affects the data quality and comprehensiveness of the disclosures, which may reduce the public’s confidence in the report’s data; and (iv) compromises the fundamental purpose of EITI open data as a tool for government to improve policy making and sector management. However, the 2020 report did not draw any conclusions in this regard.