Before proceeding with today’s article, we would like to comment on the exchanges between Chartered Accountant and Attorney-at-law Christopher Ram, and the Attorney General in relation to the apparent overstatement of the balance on the Natural Resource Fund (NRF) account. We have had detailed discussions with Mr. Ram, and we have revisited the Article 15 (4) of the 2016 Petroleum Sharing Agreement between the Government of Guyana and ExxonMobil’s subsidiaries. That sub-article clearly states that the Government’s share of Profit Oil delivered to the Government includes Exxon’s tax liabilities which are required to be paid over to the Guyana Revenue Authority (GRA). During the discussions, we floated the idea of preparing flow charts to explain the process involved. Mr. Ram was kind enough to do so and agreed for us to share them with our readers.

Before proceeding with today’s article, we would like to comment on the exchanges between Chartered Accountant and Attorney-at-law Christopher Ram, and the Attorney General in relation to the apparent overstatement of the balance on the Natural Resource Fund (NRF) account. We have had detailed discussions with Mr. Ram, and we have revisited the Article 15 (4) of the 2016 Petroleum Sharing Agreement between the Government of Guyana and ExxonMobil’s subsidiaries. That sub-article clearly states that the Government’s share of Profit Oil delivered to the Government includes Exxon’s tax liabilities which are required to be paid over to the Guyana Revenue Authority (GRA). During the discussions, we floated the idea of preparing flow charts to explain the process involved. Mr. Ram was kind enough to do so and agreed for us to share them with our readers.

There is no doubt that the balance on the NRF account includes Exxon’s income and corporation tax liabilities since there is no evidence that payments were made to the GRA. The NRF Act 2021 specifically states that all withdrawals from the NRF must be paid over to the Consolidated Fund to be used only to finance: (i) national development priorities, including any initiative aimed at realizing an inclusive green economy; and (ii) essential projects that are directly related to ameliorating the effects of a major disaster. The Attorney General has asserted that the NRF Act supersedes the PSA. This would mean that the Government is not prepared to honour Article 15 (4) in which case the sanctity of the contract would have been affected.

It has been argued that the net effect would have been the same had payments been made to the GRA which, in keeping with requirements of the constitution and the Fiscal Management and Accountability (FMA) Act, is required to transfer all tax collections to the Consolidated Fund. As Mr. Ram and I discussed, there are no short cuts in accounting; no netting off of transactions which is a fundamental principle in accounting; and one must be prepared to “take the long road” in the interest of transparency and proper accountability. That apart, the NRF and the Consolidated Fund are separate and distinct, and they serve different purposes. One also wonders whether the GRA has issued any official receipts to Exxon although it is yet to receive funds from the NRF to do so.

The solution to the problem lies perhaps in the amendment to the NRF Act to provide for a third category of payments, that is, to discharge Exxon’s liabilities to the GRA which unfortunately must be met from Guyana’s share of profit oil. However, apart from the absence of ring-fencing provisions, how does one seek to amend legislation to cater for one of the most egregious and dishonorable aspects of the PSA? Alternatively, if it can be argued that payment to the GRA falls within the category of “national development priorities” then there is no need to amend the Act.

Considering the Government’s responsibility to pay Exxon’s tax liability out of Guyana’s share of profit oil, Guyana is getting less than 50 percent of profit oil to the extent of Exxon’s tax liabilities to the GRA. It also means that we are getting less than 12.5 percent of the value of production of crude oil. On another matter, as shown in the 2022 audited public accounts, the NRF transfers to the Consolidated Fund were used to meet operating expenditure instead of “national development priorities”. In our view, the transfers should have been treated as capital revenue to finance clearly identified projects in the capital expenditure budget.

Last week, we began our review of the audited public accounts for the fiscal year ended 31 December 2022. So far, we have looked at the certification of the accounts and noted that of the eleven statements constituting the consolidated financial statements, the Auditor General has issued a qualified opinion on two of them. In other words, nine statements received a “clean bill of health”. In 2020, he had issued unqualified opinions on five statements, qualified opinions on three, and a disclaimer of opinion for one statement. Strange enough, in that same year, the Auditor General had not issued opinions on three important statements in his overall certification of the public accounts, namely, Receipts and Payments of the Consolidated Fund; Statement of Expenditure from the Consolidated Fund as compared with the Estimates of Expenditure; and Expenditure in respect of those services which by Law are directly charged upon the Consolidated Fund. It is also important to note that the Auditor General’s findings were substantially the same for both 2020 and 2022 as well as earlier years.

As regards the Statement of Current Assets and Liabilities, there was a net liability of $267.131 billion as at the end of 2022, mainly due to due to the issuance of additional Treasury Bills to finance the National Budget. The net liability also included an overdraft on the Consolidated Fund which has increased from $4.425 billion to $90.695 billion at the end of 2022. These liabilities resulted mainly from expenditure exceeding revenue, which over the period 2020-2022, amounted to $326.572 billion, or an average of $125.524 billion for each of the three years. The 2024 budget outcome is expected to yield another fiscal deficit of $92.049 billion.

In today’s article, we continue our review and analysis of the audited public accounts for 2022.

Schedule of Issuance and Extinguishment of all Loans

The Schedule of Issuance and Extinguishment of all Loans reflected a balance of $81.759 billion as at 31 December 2022, of which Guyana Sugar Corporation (GUYSUCO) accounted for $28.784 billion and $52.669 billion, respectively. GUYSUCO’s latest audited accounts to be posted on its website were in respect of 2021. They showed a long-term indebtedness to the Government of $17.240 billion while debts due for repayment within one year amounted $15.146 billion, giving a total indebted to the Government of $32.386 billion. It is unclear whether the Auditor General carried out a reconciliation between the records of GUYSUCO and the Government’s books. The amounts involved were mainly in relation to the Skeldon Sugar Modernisation Project and were based on outstanding loans from the Exim Bank of China and the Caribbean Development Bank as well as counterpart funding from the Government. We have, however, not been able to access the latest accounts of Guyana Power and Light.

Schedule of Government Guarantees

The FMA Act defines a government guarantee as a contingent liability that is an obligation undertaken by the Government to pay the debt of a third party should that party defaults on its obligation. The Act also defines a contingent liability as a future commitment, usually to spend public moneys, which is dependent upon the happening of a specified event or the materialisation of a specified circumstance.

Section 3(1) of the Guarantee of Loans (Public Corporations and Companies) Act authorizes the Government to guarantee the discharge by a corporation or a company of its obligations under any agreement which may be entered into by the corporation with a lending agency in respect of any borrowing by that corporation which is authorized by the Government. The aggregate amount of the liability of the Government in respect of guarantees is not to exceed $1 billion. On 7 August 2013, the National Assembly approved of the limit to $50 billion to facilitate the Power Purchase Agreement between the Guyana Power and Light and Amaila Falls Hydro Inc. However, since 2015 the Amaila Falls Project has been put on hold. The present Administration plans to resuscitate it.

The Schedule of Government Guarantees at the end of 2022 shows one guarantee in the sum of $500 million relating to the Bank of Guyana’s contribution to the Deposit Insurance Fund.

Schedule of Contingent Liabilities

The general principle for the recording of a contingent liability relates to the probability of occurrence of an event. If such probability is remote, then the transaction is a contingent liability. If there is a possibility that the event will crystallise out, then financial prudence will dictate that the transaction be recorded as an actual liability.

The Schedule of Contingent Liabilities is the same as that reflected in the Schedule of Government Guarantees.

The Public Debt

The public debt is debt contracted by the Government to finance public expenditure. There are two categories involved: (i) external debt arising from disbursements of loans from international financial institutions such as the World Bank and the Inter-American Development Bank as well as bilateral debts; and (ii) domestic debt arising from local borrowings in the form of Treasury Bills and debentures.

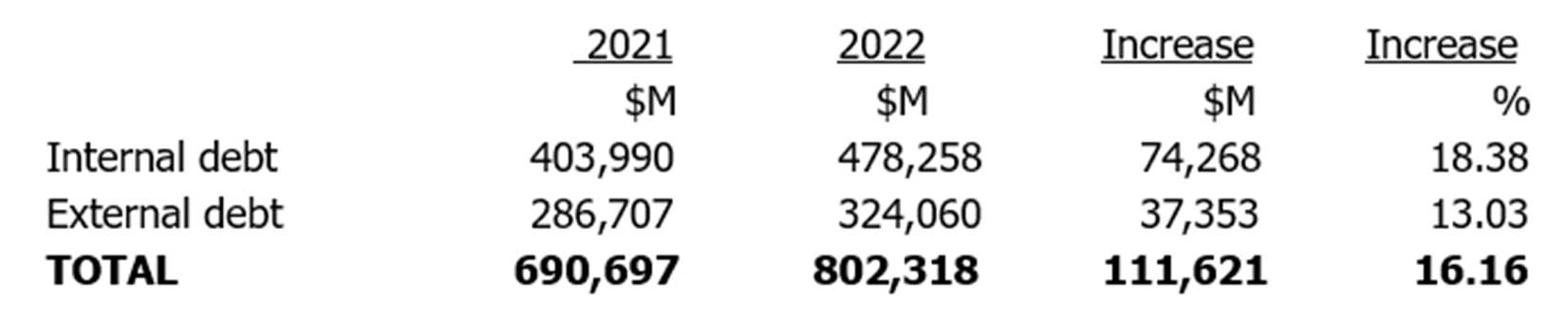

At the end of 2022, the public debt stood at G$802.318 billion, compared with G$690.697 billion at the end of 2021, an overall increase of G$111.621 billion, or 16.16 percent. This increase was mainly due to a significant increase in the internal debt that moved from $403.990 billion in 2021 to $487,258 billion in 2022, representing an 18.13 percent increase, as shown below:

Treasury Bills outstanding at the 2022 amounted to $228.977 billion, compared with $146.507 billion, an increase of $82.47 billion. Debentures totalled $245.292 billion, mainly due to the issuance in 2021 of five sets of variable interest rate debentures totalling $200 billion, with repayment periods ranging from one year to 20 years. These debentures were issued to liquidate the overdraft on the Consolidated Fund.

In equivalent United States dollars, the external debt was US$1.554 billion, compared with US$1.375 billion at the end of 2021. This net increase was due mainly to: (i) disbursements totalling US$261.284 million in respect of loans contracted; and (ii) repayments of principal amounting to US$60.710 million.

Conclusion

While the Auditor General is up to date in the auditing of central government activities, the quality of his audit and reporting of the results can be improved significantly if comprehensive quality assurance procedures are adopted.

These procedures ensure that: (i) the audits are conducted in accordance with approved audit plans and detailed audit procedures based on risk assessments, are carefully followed; (ii) the findings are supported by adequate audit evidence and are properly formulated; (iii) the recommendations are concise and precise, and follow the SMART ( simple, measurable, achievable, relevant and time-bound) approach; and (iv) the overall conclusions in the form of certification of the accounts are carefully crafted in accordance with the International Standards of Auditing.

The Auditor General needs to reflect on the impact of his reports which are unwieldy in terms of size and content and are substantially a copy and paste of the contents of the previous report, with appropriate amendments.

Some of the findings are also not material to the proper presentation of the public accounts and are essentially in realm of internal audit. Additionally, consideration should also be given to a revised reporting format. The present reporting template has been in place since 1992.