Every Man, Woman and Child in Guyana Must Become Oil-Minded – Column 129

Every Man, Woman and Child in Guyana Must Become Oil-Minded – Column 129

Introduction

On 29th December 2023, in a letter to the press, I argued that the Natural Resource Fund was overstated by G$274 BN., the amount of the Corporation Taxes paid by the Government on behalf of the oil companies required under Article 15.4 of the 2016 Petroleum Agreement. Attorney General, Mr. Anil Nandlall, S.C., disputed my assertion in a direct, unnamed tirade against me.

Mr. Nandlall wrote that the supremacy provision (section 45) of the Natural Resource Fund Act overrode the provisions of the 2016 Petroleum Agreement, boldly asserting that the provisions in the Agreement on taxation have “obviously been overtaken by the Natural Resource Fund Act”. In the process he completely ignored the Stability Clause of the Agreement, which requires the Government to pay the taxes of the Oil Companies out of its share of oil revenues. What is indisputable is that despite the so-called supremacy clause, the Government continues to pay the taxes for the oil companies.

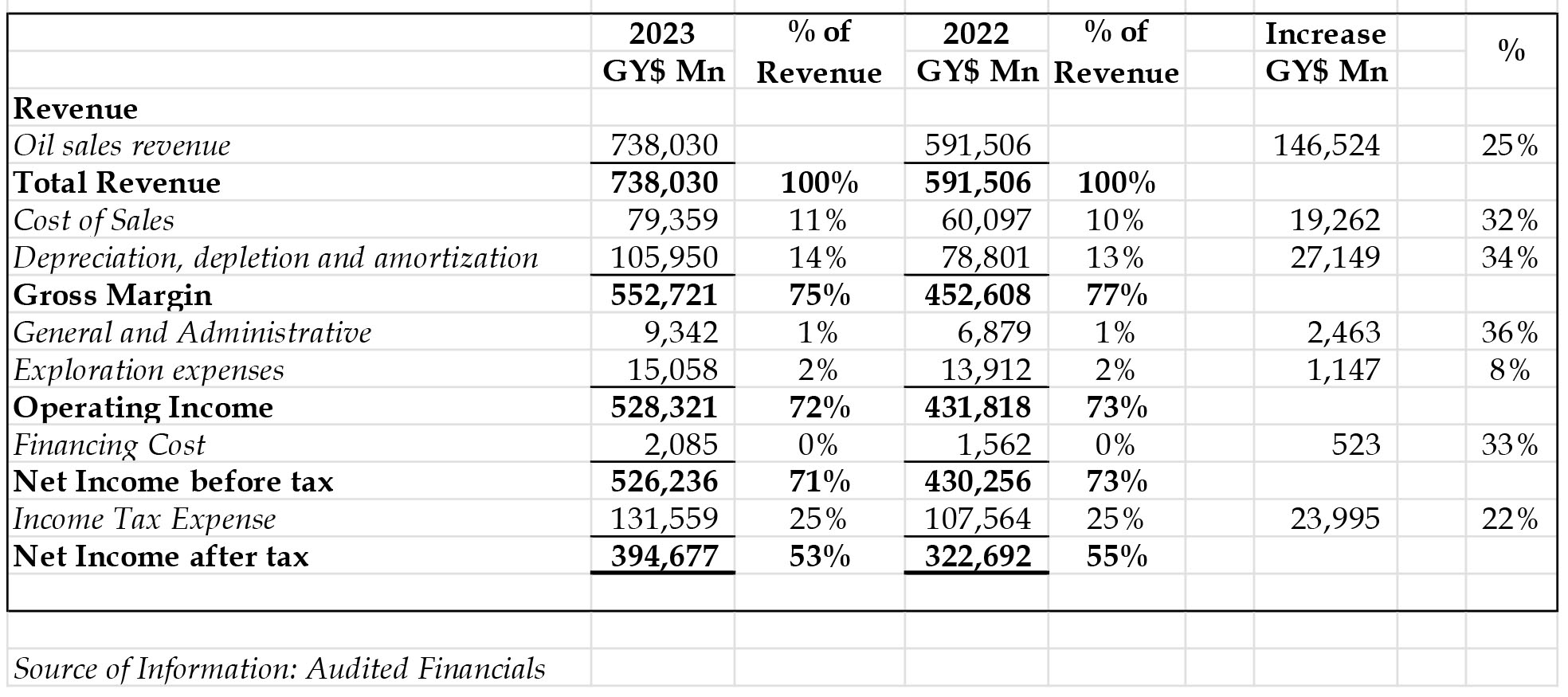

The 2023 financial statements of Hess, a 30% partner in the Exxon-led joint venture show a tax charge of G$131,559 million, or approximately 22% more than 2022. The Note to the financial statements shows that the charge includes Deferred Tax of $40,920 million. More significant than the 22% increase is how the tax charge measures up against the profit oil earned by Guyana for the whole of 2023. From figures available on the BoG website, the total tax charge is about 45% of the country’s earnings from profit oil earned by Guyana for the whole of 2023.

The 2023 financial statements of Hess, a 30% partner in the Exxon-led joint venture show a tax charge of G$131,559 million, or approximately 22% more than 2022. The Note to the financial statements shows that the charge includes Deferred Tax of $40,920 million. More significant than the 22% increase is how the tax charge measures up against the profit oil earned by Guyana for the whole of 2023. From figures available on the BoG website, the total tax charge is about 45% of the country’s earnings from profit oil earned by Guyana for the whole of 2023.

Let us have a look at how Hess performed. Its oil revenues grew to $738, 030 million, an increase of 25%, compared with an 8% decline in the Hess International group as a whole. In fact, all the key financial indicators for Hess in 2023 were down, compared with 2022. No wonder then that Guyana is likened to the Indo/British Kohinoor, the jewel of the Hess’ crown. It would be surprising if that comparability is significantly different in the case of Exxon and CNOOC.

Cost of Sales for the Guyana branch grew by 32% over 2022 but remained constant as a percentage of revenue. Cost of sales is made up principally of Operating Cost and expenses and Royalties and whether and how useful this is as a predictive value is uncertain. Oil companies are generally expert at aggressive tax planning and even now, the financial statements disclose depreciation, depletion and amortisation at some 163 per cent of operating costs and expenses. This latter group of expenses in 2023 (13% of revenue), but a 34% increase over the preceding year. Because there is no ringfencing, exploration expenses are charged against income, but at 2% of revenue, even the dollar amount is not particularly significant.

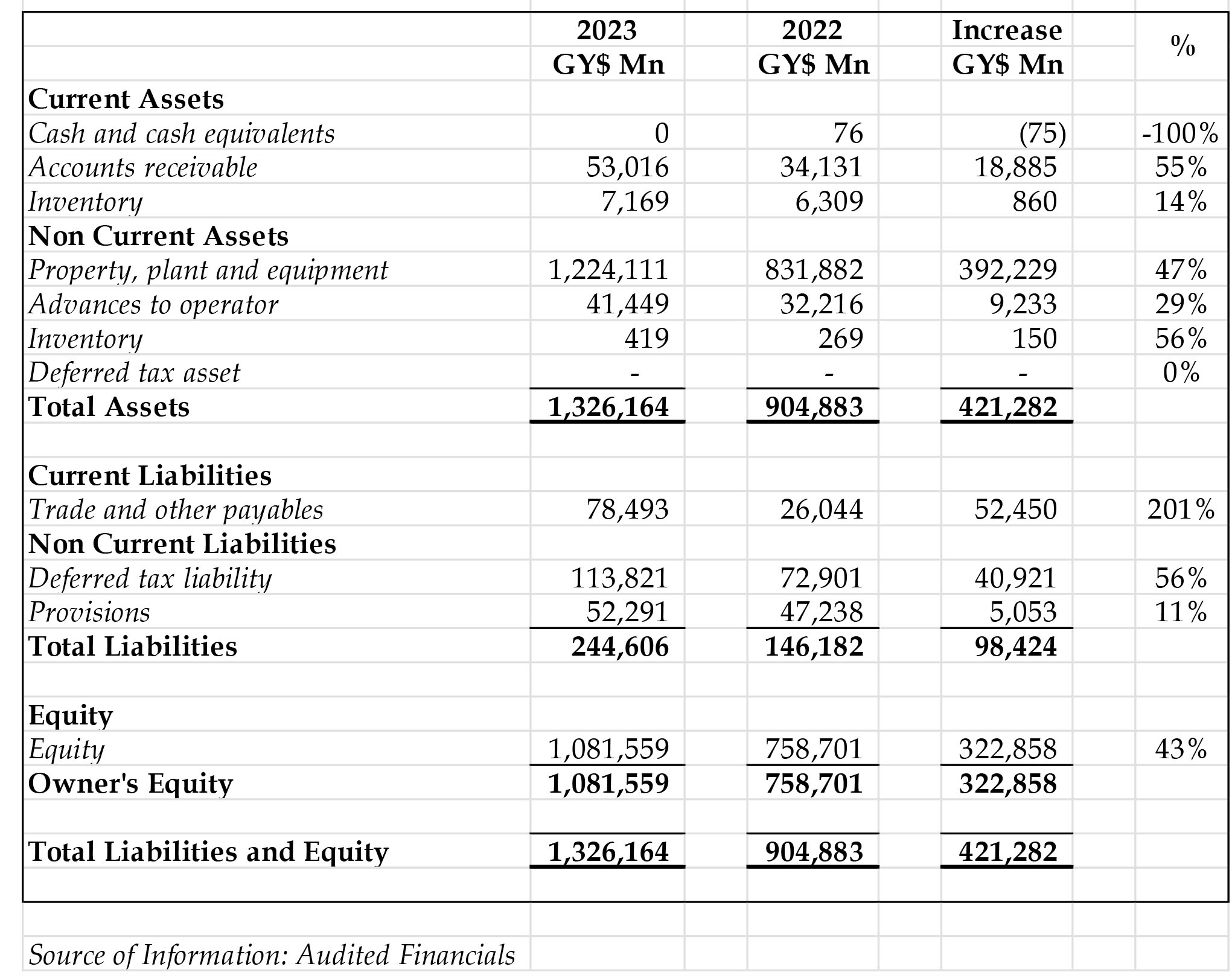

The Balance sheet

The growth in the total assets over 2022 is a significant 47% which is identical to the growth in Property, Plant and Equipment, shared between Exploration and Evaluation Assets (21%) and Development Assets (79%). Because of the uncertainty associated with such expenditure, Exploration and Evaluation Assets are not depreciated. Depreciation expenditure on Development Assets account for 99.9% of Depreciation charge for the year.

Exxon

Maybe it is purely by coincidence, ExxonMobil Guyana invited the domestic press for a briefing on its own 2023 audited financial statements and apparently to offer some guidance on how the press should report on financial matters. Whatever its motives, the company should be complimented on this display of accountability even as it has refused to answer questions concerning its own suspect accounting for moneys received from various entities.

Next week’s Road to First Oil will review the company’s 2023 financial statements which reflect a bonanza year for the company.