Two Fridays ago, the National Assembly approved two financial papers presented by the Minister of Finance seeking Supplementary Estimates in the sum of $40.8 billion. This was one day before the Assembly was expected to proceed on a two-month recess. Financial Paper No. 1 relates to two advances made from the Contingencies Fund amounting to $8.6 billion covering the period 1 April to 30 July 2024 to meet additional operational costs of Guyana Power and Light (GPL) Inc. – $4.0 billion); Guyana Rice Development Board (GRDB) – $534 million); and Guyana Sugar Corporation (Guysuco) – $4.043 billion. Financial Paper No. 2 covers a Supplementary Estimate of $32.2 billion for both capital and current expenditure in the amounts of $11.7 billion and $20.5 billion, respectively.

Two Fridays ago, the National Assembly approved two financial papers presented by the Minister of Finance seeking Supplementary Estimates in the sum of $40.8 billion. This was one day before the Assembly was expected to proceed on a two-month recess. Financial Paper No. 1 relates to two advances made from the Contingencies Fund amounting to $8.6 billion covering the period 1 April to 30 July 2024 to meet additional operational costs of Guyana Power and Light (GPL) Inc. – $4.0 billion); Guyana Rice Development Board (GRDB) – $534 million); and Guyana Sugar Corporation (Guysuco) – $4.043 billion. Financial Paper No. 2 covers a Supplementary Estimate of $32.2 billion for both capital and current expenditure in the amounts of $11.7 billion and $20.5 billion, respectively.

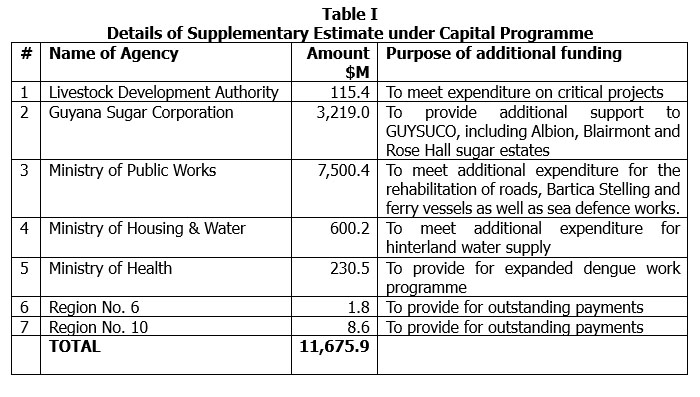

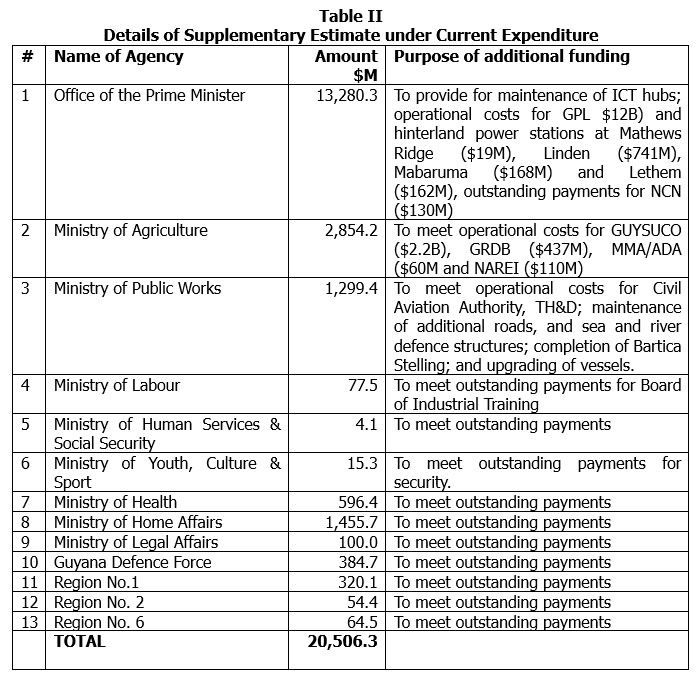

In our last week’s article, we stated that when introducing a supplementary appropriation Bill in the Assembly, the Minister must give reasons for the proposed variations and provide a supplementary document describing the impact that the variations, if approved, will have on the financial plan outlined in the annual budget. This is provided for under Section 24 of the Fiscal Management and Accountability (FMA) Act. However, the reasons given for the request for increased funds were somewhat brief, as shown in Tables I and II, necessitating legislators requesting clarification from the relevant Ministers.

Additionally, the package of documents submitted to the Assembly did not include the supplementary document referred to above to enable legislators and the public at large to ascertain what effect the additional funds will have on the overall budgetary allocations for 2024. For example, there was no information as to: how much was expended as of 30 June in respect of the entities for which additional funds were sought; what effect these additional funds will have on the entities’ annual work programs; and whether there will be variations in the work programmes of these entities.

Additionally, the package of documents submitted to the Assembly did not include the supplementary document referred to above to enable legislators and the public at large to ascertain what effect the additional funds will have on the overall budgetary allocations for 2024. For example, there was no information as to: how much was expended as of 30 June in respect of the entities for which additional funds were sought; what effect these additional funds will have on the entities’ annual work programs; and whether there will be variations in the work programmes of these entities.

Guyana Power and Light Inc.

The last set of audited financial statements of GPL Inc. was in respect of 2022 which shows a net loss of $10.684 billion, compared with a loss of $6.593 billion in 2021. In fact, for the period 2015 -2022, it was only in 2015 and 2016 that the power company turned in profits of $3.342 billion and $623 million, respectively. The auditors have also emphasized in their reports that GUYSUCO was indebted to GPL Inc. in the sum of $2.283 billion. This amount has been coming forward since 2016 and perhaps earlier.

The 2024 Estimates of Revenue and Expenditure showed an amount of $6.2 billion was budgeted as contribution to power generation. Taking into account the Supplementary Estimates of $4 billion and $13.1 billion reflected in Financial Papers No. 1 and 2, respectively, the revised budgetary allocation for power generation in terms of subsidies amounts to $23.3 billion.

Guyana Rice Development Board

The last set of audited financial statements of the Guyana Rice Development Board (GRDB) was in respect of 2021, according to the Board’s website. These statements were given a “disclaimer of opinion”, meaning that the accounts were in such a bad shape that the auditors were unable to express an opinion on them in terms of their fair presentation and compliance with applicable laws, regulations, circular instructions and contractual obligations. In that year, GRDB recorded a net loss of $118.5 million. Similar disclaimers of opinion were issued for the years 2019 and 2020, and perhaps earlier years. It boggles the mind how legislators are able to approve not only original budgetary allocations but also Supplementary Estimate for entities whose accounts were in such a bad shape, without seeking answers for their proper accountability and stewardship responsibilities.

Guyana Sugar Corporation

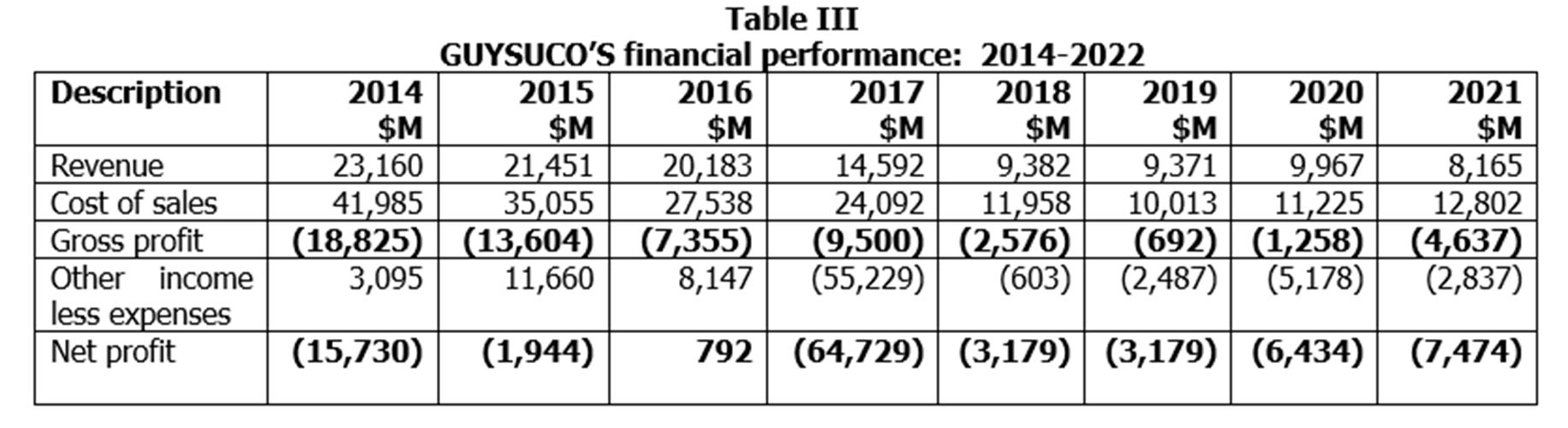

Guysuco’s Chief Executive Officer was reported as having stated that the corporation recorded losses of $7.8 billion and $10.2 billion in 2021 and 2022, respectively, and the accounts for 2023 are currently being audited. This has prompted us to examine the audited accounts of Guysuco over the years. However, the 2022 accounts are yet to be posted on Guysuco’s website. Shown in Table III is Guysuco’s financial performance for the years 2014 to 2021.

The above financial performance was despite the large subsidies granted by the Central Government over the years. For example, 2024 Estimates of Revenue and Expenditure showed a subsidy of $4.0 billion provided to Guysuco. Taking into account the Supplementary Estimates of $2.2 billion and $4.0 billion as reflected in Financial Papers Nos 1 and 2, respectively, the revised budgetary allocation for the corporation in terms of subsidies and contributions amounts to $10.2 billion.

As in the case of the GRDB, the accounts of the corporation were in a bad shape resulting in the auditors giving disclaimers of opinion for the years 2020 and 2021. For the years 2014 to 2019, the auditors have issued qualified opinions and/or “emphases of matter”. A qualified opinion is one is which the matters giving rise to the qualification are material but do not affect the overall presentation of the financial statements. On the other hand, an emphasis of matter is one in which the auditors express concerns about certain items in the financial statements which, if not addressed urgently, can give rise to a deterioration in the financial performance of the concerned entity.

The year 2009 was a turning point in the history of Guysuco after it was forced to compete on the world market for the price of its sugar, following the collapse of the European Union preferential market in the early 2000s. As a result, the corporation was faced with several challenges, including its ability to remain competitive in view of the high cost of production, necessitating significant financial bailout from the Central Government.

To address the plight of Guysuco and to reduce its financial dependence on the Treasury, the previous Administration in 2016 closed the four loss-making sugar estates – Skeldon, Rose Hall, Enmore and Wales – resulting in the corporation turning in a profit for the first time since 2007. One of the mistakes it had made, however, in its decision to close these estates was that due consideration was not given to, among others, the plight of sugar workers who were affected by the closure. Perhaps some of the lands that the present Administration took over for its housing programme could have been allocated to the displaced workers for agricultural purposes, thereby providing them with a source of income. We had spoken to some of the displaced workers from Wales Estate who indicated that they would have been happy if they were provided with 3-5 acres plots for farming, with the Central Government providing drainage and irrigation facilities as well as farm-to-market access. However, this was not to be.

In 2017, GUYSUCO recorded a loss of $64.729 billion, of which amounts totalling $55.693 billion relate to the write-off of value of fixed assets and inventories of the closed estates. These assets were transferred to the National Industrial and Commercial Investments Ltd. (NICIL) at no cost. In 2019, the assets of Skeldon, Rose Hall and Enmore estates were re-transferred to Guysuco, but the relevant instrument of re-transfer was not issued to enable ownership rights and recording in the books of the Guysuco. Because of this as well as other matters, the auditors issued a disclaimer of opinion on the financial statements of the corporation for that year.

National Industrial and Commercial Investments Ltd.

The last set of audited accounts of NICIL was in respect of 2013. Given the absence of audited accounts for 2017, it is unclear how the assets of the closed estates have been accounted for in the books of NICIL.

In our article of 23 November 2020, we had stated that as of June 2012, NICIL was eleven years in arrears in financial reporting and audit. The last set of audited accounts was in respect of 2001.

Concerned about the state of accountability of NICIL in general, and the lack of transparency and accountability associated with the disposal of State assets in particular, the Assembly passed Resolution No. 14 dated 27 June 2012 calling on the relevant Ministers to, among others:

(a) Provide the Assembly with a report on the disposal by sale or otherwise of all State lands during the period 2000-2011, including the terms on which they were disposed of, and the criteria used.

(b) Make financial provision for the urgent commissioning of an independent financial audit of NICIL and the Privatisation Unit.

(c) Provide a detailed report on the disposal by sale or otherwise of all State assets entrusted to NICIL and the Privatisation Unit, the terms on which they were disposed of, and the criteria used.

(d) Provide the outstanding bi-annual reports and annual audited accounts required of NICIL and the Privatisation Unit under the relevant legislation.

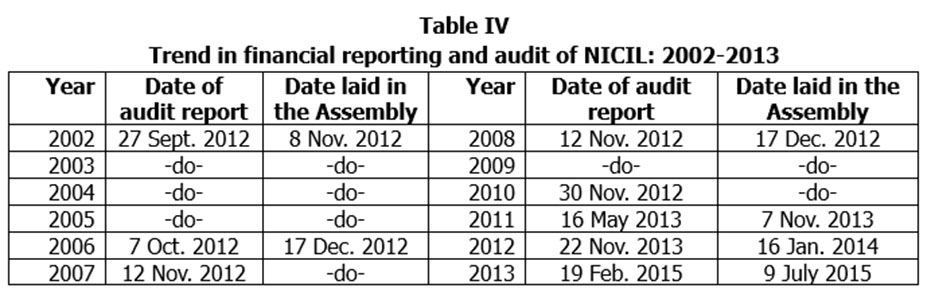

Three months later, on 27 September 2012, the Auditor General issued his reports on the financial statements of NICIL for the years 2002, 2003, 2004 and 2005. Within the next 14 months, he issued further reports covering the period 2006 to 2012. These accounts were given a “clean bill of health”, despite the concerns expressed by the Assembly as regards the entity’s state of accountability. Table IV shows the trend of financial reporting and audit of NICIL for the period 2002 to 2013: Next week, we will continue our discussion on the status accountability for entities, especially those that are in receipt of subsidies from the Central Government.

Next week, we will continue our discussion on the status accountability for entities, especially those that are in receipt of subsidies from the Central Government.