Last week, we concluded our discussion of the two Supplementary Estimates totalling $40.8 million that the National Assembly approved three weeks ago. Of this amount, $9.462 billion relates to the Guyana Sugar Corporation (GUYSUCO) which has been making significant losses over the last 14 years (except for 2016) despite massive subsidies from the Central Government to assist the corporation with not only its operational costs but also its infrastructure development programme.

GUYSUCO’s revenues from the sale of sugar declined from $23.160 billion in 2014 to $8.161 billion in 2021, an almost three-fold decrease. Operational costs also decreased from a massive $41.985 billion to $12.802 billion over the same period due mainly to the closure of the four loss-making estates at Skeldon, Rose Hall, Enmore and Wales in 2016. This has resulted in a decrease in the corporation’s operating loss from $18.825 billion in 2018 to $4.637 billion in 2021. According to its Chief Executive Officer, GUYSUCO recorded a loss of $10.2 billion in 2022. The corporation’s financial performance over the years raises serious questions about the sustainability of the Treasury bailout and for how long more it would be able to produce sugar at a cost of about US$1 per pound when the world market price is around US$0.33. The re-opening of the Rose Hall Estate is likely to compound the problem.

One recalls the construction of the new factory at Skeldon Estate at a cost of US$172.8 million of which US$37.8 million represents a loan from the Exim Bank of China. This was despite the significant decline in the demand for cane sugar as well as the collapse of the European Union preferential market in the early 2000s, thereby forcing the corporation to compete on the world market for the price of its sugar. As a result, the corporation was faced with several challenges, including its ability to remain competitive in view of the high cost of production. To date, the factory remains non-operational because of construction defects. The loan from Exim Bank of China, inclusive of interest and other charges, is expected to be fully repaid by March 2025.

In today’s article, we discuss the status of financial reporting and audit of non-Central Government agencies as at the end of August 2023, as gleaned from the latest Auditor General’s report.

Financial reporting and audit of public enterprises and statutory bodies

There are 180 non-Central Government entities comprising public enterprises, statutory bodies, municipalities and Neighbourhood Democratic Councils (NDCs), as shown below:

Public enterprises 39

Statutory bodies 61

Municipalities 10

Neighbourhood Democratic Councils 70

TOTAL 180

Of the 39 entities comprising public enterprises, the Auditor General/Chartered Accountants issued 36 reports in respect of 17 entities, through a combination of in-house audits and contracting out arrangements. Similarly, of the 61 statutory bodies, a total of 69 audits were finalized in respect of 41 entities. It is unclear what was position in respect of the remaining 42 entities. Suffice it to state that most of the accounts audited relate to backlogged years although the concerned entities are required to have their audited accounts presented to the National Assembly within six months of the close of the fiscal year.

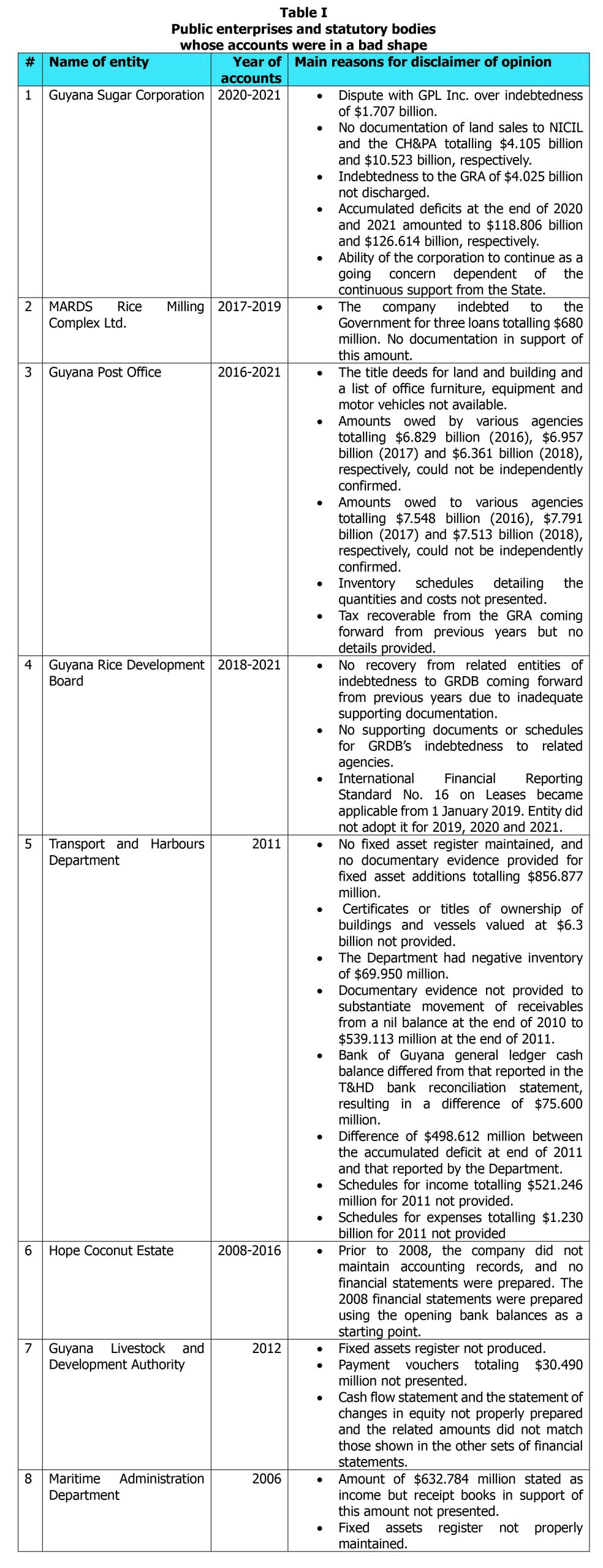

The Auditor General/Chartered Accountants have disclaimed their opinions on the financial statements of eight entities, shown at Table I. This was because the accounts were in such a bad shape that the auditors were was unable to draw conclusions on their fair presentation and compliance with applicable laws, regulations, circular instructions and contractual obligations.

In respect of the remaining entities, 11 received qualified audit opinions, while 39 received were given unqualified opinions i.e. clean bill of health.

Financial reporting and audit of municipalities

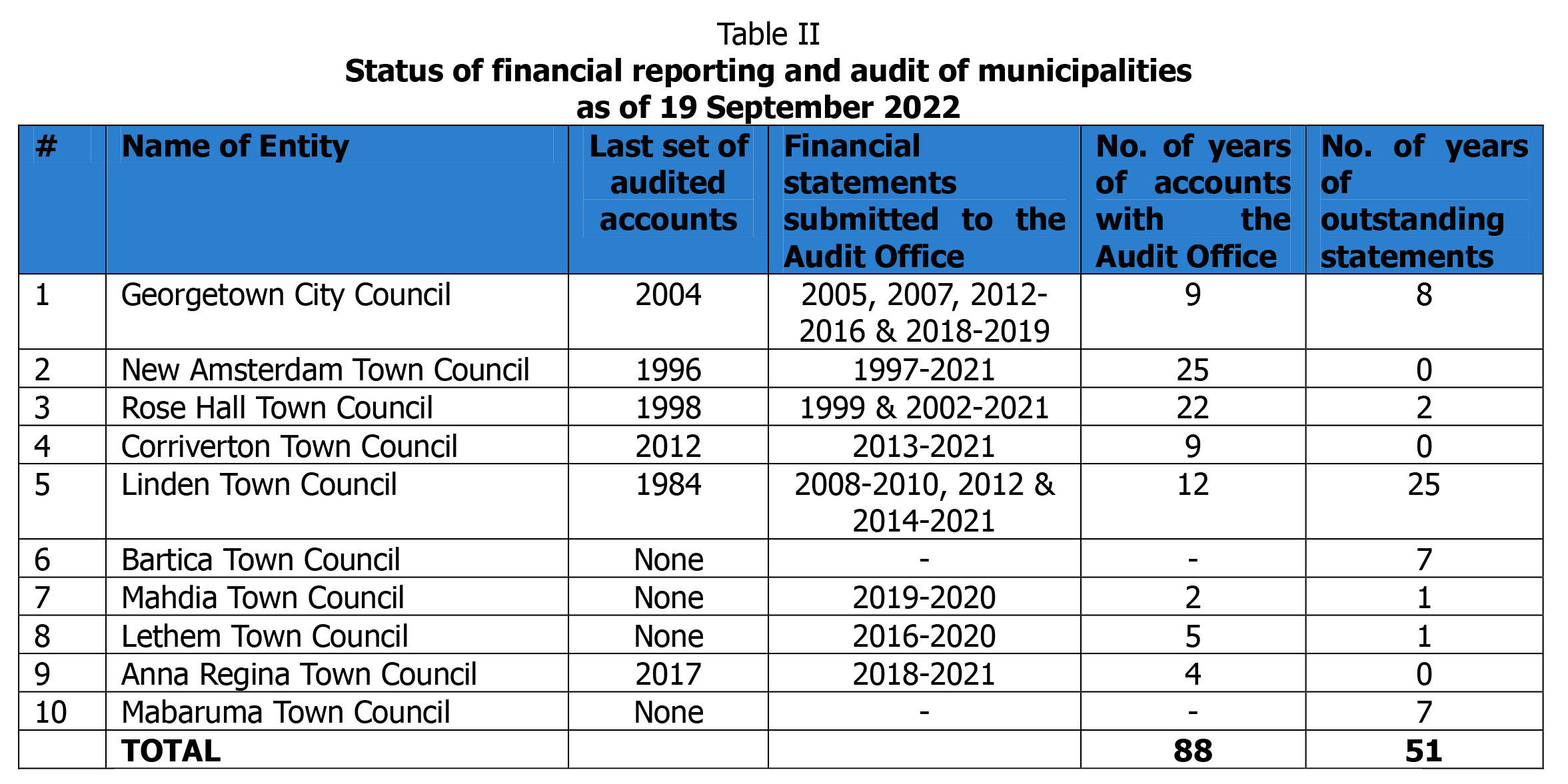

Section 177 of Chapter 28:01 of the Municipal and District Councils Act requires all treasurers to prepare and submit to the Auditor General within four months of the close of the fiscal year. The failure to do so constitutes an offence. In our articles of 18 April 2022 and 4 September 2023, we had stated that of the ten municipalities, only Anna Regina Town Council was audited in 2020 covering seven years of accounts from 2011 to 2017. The remaining nine entities had a total of 128 years of accounts still to be audited, which works out to on average 14 years in arrears, as shown in Table II.

Since then, there has been no further movement in relation to the audit of municipalities, except Corriverton Town Council which was audited to 2018. In particular, the largest municipality, Georgetown City Council, was last audited up to 2004. Linden Town Council was also last audited and reported on in 1984 and is therefore 38 years in arrears. A point to note is that as of 22 September 2022, the Audit Office had in its possession 88 sets of accounts still to be audited and reported on.

It is evident that the audit of municipalities has not been assigned the priority it deserves. The respective councils responsible for managing the affairs of these entities are also not devoid of blame for not pressuring the Auditor General to have their accounts audited in a timely manner in order to discharge their financial stewardship responsibilities. And what of the Ministry of Local Government and Regional Development in relation to monitoring the affairs of the municipalities to ensure that they discharge their accountability responsibilities? Does the Minister also not have a responsibility, considering that the Act requires the Auditor General to submit to him a copy of the audited accounts within one month of the completion of the audit?

Financial reporting and audit of Neighbourhood Democratic Councils

The Municipal and District Councils Act, Chapter 28:01 of the Laws of Guyana requires all accounts of Municipal and District Councils to be prepared not later than four months after the end of each year and for those accounts to be audited as soon as practicable thereafter. The responsibility for the preparation of the annual financial statements in the form set out in the regulations rests with the Treasurer who shall be guilty of an offence if he/she neglects to do so.

A review of the Auditor General’s reports over the years indicates that the status of financial reporting and the audit of the NDCs has been far from satisfactory. For example, no reports were issued in 2020; while for 2019 only four NDCs were audited and reported on for periods varying from 2010 to 2018. For 2018, audit reports for five NDCs were issued again for varying periods; while for 2017, audit reports for 17 NDCs were issued. In most cases, the Auditor General issued qualified opinions on the accounts.

According to the 2022 Auditor General’s report, the majority of the NDCs were significantly in arrears in submitting financial statements for audit, with 42 NDCs not submitting accounts for the years 2019, 2020 and 2021. This was despite the fact that these NDCs are in receipt of subventions through the National Budget. In 2024, the NDCs received a total of $833.9 million in subventions, giving as average of $11.912 million per NDC.

Of the 102 audits finalised in respect of 21 NDCs, Zeelust/Rosignol NDC was given disclaimers of opinion for the years 2007, and 2009-2010 because of the absence of sufficient documentation. The remaining 20 NDCs were given qualified opinions for 99 sets of accounts covering varying periods between 2006 and 2021.

Concluding remarks

While we love to boast that every year we have audited public accounts, we fail to reflect on the quality of such accounts as well as their completeness and comprehensiveness. Every year, the Auditor General issues qualified opinions and disclaimers of opinion on most of the individual statements constituting the public accounts, with little or no action taken to remedy the deficiencies identified. In this regard, we should mention that the Public Accounts Committee (PAC), whose responsibility is to scrutinize the audited public accounts, is yet to report on its examination of such accounts for the years 2019, 2020, 2021 and 2022. Regrettably, the accounts of the 180 non-Central Government entities have escaped the scrutiny of the Committee over the years.

Finally, it is desirable for the financial reporting and audit of local government bodies to run parallel with that of central government so as to ensure that funds allocated to these bodies via the national budget are properly accounted for, and in a timely manner. It follows that there should be no arrears in financial reporting and audit of local government bodies.