This is our first attempt to provide readers with a summary of the main issues discussed in our weekly Accountability Watch column during the course of the year. These issues relate mainly to budgetary matters, public procurement, natural resource management, and other related issues.

Budgetary matters

2024 Estimates of Revenue and Expenditure

On 15 January, the Minister of Finance presented to the National Assembly the Estimates of Revenue and Expenditure for the fiscal year 2024. The size of the budget was $1.146 trillion, compared with $828.640 billion actual expenditure incurred in 2023, a 38.3 percent increase, and a 46.6 percent increase compared with the Estimates for that year.

Fiscal deficits

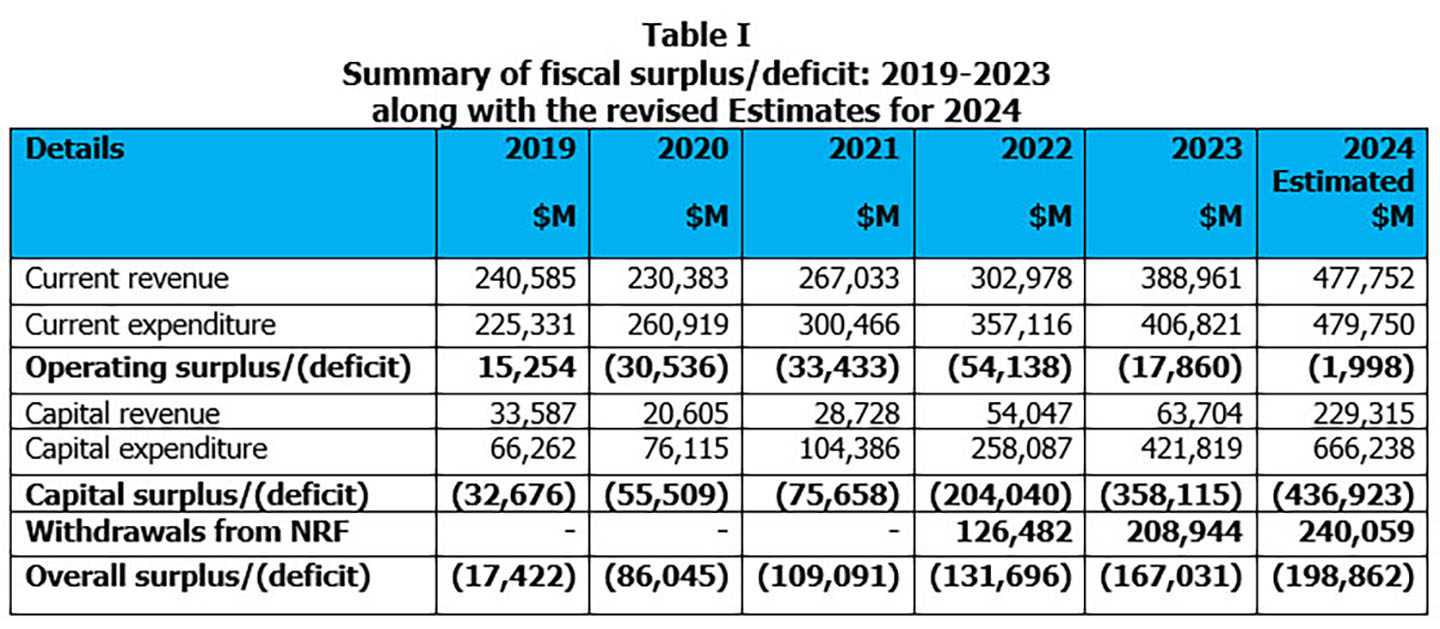

Fiscal deficits have been recorded every year since 1992 and perhaps earlier years, except for 1994, 2006, 2010 and 2011, with no end in sight when a balanced budget will be in place, despite the receipt of oil revenues over the past four years. Table I provides a summary of the fiscal deficit over the period 2019 to 2023, along with the revised Estimates for 2024.

As can be noted, the fiscal deficit increased over ten-fold from $17.422 billion in 2019 to an estimated $198.861 billion in 2024. It is disappointing that the Estimates continue to be crafted in isolation of any medium-term budget and fiscal frameworks. In other words, there are no strategic plans against which the Estimates can be anchored. In the private sector, it will be surprising if an organization prepares its annual budget without reference to a strategic framework.

International Monetary Fund assessment

In its Article IV Consultation reports for 2022 and 2023, the International Monetary Fund (IMF) advised that the overall fiscal deficit should not exceed the amount withdrawn from the NRF. Accordingly, it recommended the following:

Given the sheer size of the expected oil transfers and fiscal spending, the policy priorities should be to avoid overheating and `Dutch disease’’.

There is a need to closely monitor macroeconomic and financial indicators and further tighten monetary policy stance.

A comprehensive fiscal policy framework should be developed to guide spending decisions based on a Medium-Term Fiscal Framework, along with further enhancements of the public financial management framework, including public investment.

The Fund noted that transitioning to a zero overall fiscal balance over the medium term will allow the Government to meet its ambitious investment goals, while ensuring fiscal sustainability and intergenerational equity without creating macroeconomic imbalances.

Financing of fiscal deficits

Over the years, the fiscal deficits were financed mainly from local borrowings in the form of an overdraft on the Consolidated Fund as well as the issuance of Treasury Bills and debentures. At the end of 2023, the internal debt was $609.757 billion, compared with $478.258 billion, an increase of $131.499 billion. This does not include the overdraft on the Consolidated Fund which moved from $90.695 billion at the end of 2022 to $112.461 billion. At the end of 2020, the overdraft was $163.340 billion which attracted no interest charges from the Bank of Guyana. It was, however, cleared in June 2021 through the issuance of 85 variable interest debentures valued at $200 billion. Treasury Bills outstanding also increased from $226.542 billion to $372.596 billion.

Natural Resource Fund withdrawals

Section 16(2) of the NRF Act is clear that withdrawals are only to be used to fund: (i) national development priorities, including any initiative aimed at realizing an inclusive green economy; and (ii) essential projects that are directly related to ameliorating the effects of a major natural disaster. The word “only” suggests that the proposed expenditure needs to be clearly identified. It also implies that such withdrawals should not be treated as current revenue to be commingled with internally generated revenue to meet operational costs.

Despite this requirement, NRF withdrawals have so far been treated as current revenue in the Estimates and the public accounts. This practice not only allows the Authorities complete discretion as to how the withdrawals are to be expended but also has the effect of giving a distorted view of the Government’s results of operation. For example, for 2022, the Estimates showed an operating surplus of $72.344 billion. However, if one were to exclude the NRF withdrawals, an operating deficit of $54.138 billion would have been recorded, as shown in the above table. The same applies to the fiscal year 2023 where an operating deficit of $17.860 billion would have been recorded, instead of a surplus of $191.084 billion.

The solution to the problem is to consider NRF withdrawals as capital revenue to be matched with corresponding capital expenditure. Volume III of the Estimates lists all capital expenditure projects showing, among others: (i) name and description of the project as well as its location; (ii) responsible executing agency; (iii) benefits to be derived; (iv) total estimated project cost (v) expenditure to date; (vi) proposed amount to be spent in the fiscal year; and (vii) sources of financing. If this course were to be adopted, it would satisfy the requirements of Section 16(2) and would enhance transparency and proper accountability for the use of oil revenues.

2024 Mid-Year report

On 28 August, the Minister issued the 2024 Mid-Year Report on the execution of the annual budget and the performance of the economy. The report was prepared in accordance with Section 67 of the Fiscal Management and Accountability (FMA) Act that requires the Minister to present to the Assembly within 60 days of the end of the first half-year of each fiscal year, a report on the year-to-date execution of the annual budget and the prospects for the remainder of that fiscal year. The report is to include:

An update on the current macroeconomic and fiscal situation, a revised economic outlook for the remainder of the fiscal year, and a statement of the projected impact that these trends are likely to have on the annual budget for the current fiscal year.

A comparison report on the out-turned current and capital expenditures and revenues with the estimates originally approved by the Assembly with explanations of any significant variances.

A list of major fiscal risks for the remainder of the fiscal year, together with likely policy responses that the Government proposes to take to meet the expected circumstances.

The report was issued at the time the Assembly was in a two-month recess and when it was reconvened in October, there was no discussion or debate on the report. In any event, it would have been too late for the Assembly to take any action as regards to (a) to (c).

As of 30 June, amounts totalling $375.6 billion were expended, representing an overall 32.8 percent achievement on the original budget. Current expenditure was 42.8 percent, with amounts totalling $205.4 billion expended out of the original budgetary allocation of $479.7 billion; while capital expenditure was $162.9 billion, representing 24.5 percent of the allocation of $666.2 billion. At this rate, by the end of the year, only two-thirds of the total budget will be executed unless measures are put in place to accelerate the execution of programmes and activities, especially as regards infrastructure development, without breaching the FMA Act.

In the past, contracts were executed close to year-end; cash books were kept open well into the new year; and cheques drawn and backdated to 31 December to exhaust budgetary allocations although value was not received as of this date. This was in clear breach of Section 26 which requires all unspent balances at the end of the year to be surrendered to the Consolidated Fund. Because of this and other violations, all sorts of breaches and irregularities occurred, including significant breaches in the tendering procedures relating to the procurement of goods/services and the execution of works; defective work performed; overpayments to suppliers/contractors; and goods/services not delivered for which payments have been made.

According to the 2023 Auditor General’s report, there were 3,134 cheques valued at $2.463 billion still on hand as of September 2024, suggesting that these cheques might have been drawn close to year-end, or early in the new year and backdated to 31 December 2023, in order to exhaust budgetary allocations. As a result, expenditure has been overstated by the above amount since no value was received. It is not clear what follow-up action the Auditor General has taken with respect to these payments to ensure no irregularities have occurred.

Public procurement

Public Procurement Commission

Amid widespread concerns about the basis of the award of contracts for the procurement of goods and services and the execution of works as well as the extent of leakages in the Government’s procurement systems, the Constitution was amended in 2001 to provide for the establishment of the Public Procurement Commission to monitor public procurement and the related procedures to ensure that the procurement of goods and services and the execution of works are conducted in a fair, equitable, transparent, competitive and cost-effective manner in accordance with law and policy guidelines as determined by the National Assembly.

The Commission comprises five members appointed by the President after their nomination by the Public Accounts Committee (PAC) and the approval of at least two-thirds of the elected Members of the Assembly. It must function independently and impartially and discharge its responsibilities fairly. The commissioners are required to have expertise and experience in procurement, legal, financial, and administrative matters to enable them to discharge their responsibilities effectively. It is particularly important for the Commission to be viewed as independent of the political process. In principle, no one should be appointed a commissioner if he/she is a member of a political party or is closely associated with that party. It is the duty of the PAC to ensure that these requirements are scrupulously followed.

At the time the first commissioners were appointed, the Chairman of the PAC was President Irfaan Ali. Instead of following a rigorous process involving public advertisement, shortlisting of eligible candidates, interviewing, and selecting the best candidates for consideration by the Assembly, the PAC took the least line of resistance by requesting the two major political parties to nominate their candidates – three from the People’s Progressive Party/Civic; and two from the APNU+AFC. This practice was repeated in relation to the appointment of the current commissioners.

National Procurement and Tender Administration Board

As regards the functioning of the National Procurement and Tender Administration Board NPTAB) established under the Procurement Act 2003, there was evidence of contracts not being awarded to the lowest evaluated bids while some contractors did not meet the qualification requirements set out in the Act, yet they were awarded large contracts.

With reporting relationship to the Minister of Finance, the Board is to comprise of seven members among persons of unquestioned integrity with backgrounds in business, the professions, law, audit, finance and administration: not more than five from the Public Service; and not more than three from the private sector after consultation with their representative organizations. Two members are to serve on a full-time basis while the remainder are to function on a part-time basis. The Minister appoints the Chairman from one of the two full-time members.

Members of the NPTAB are to serve for two years. However, the Act is silent as to whether appointments can be renewed. This is a significant shortcoming, considering the sensitive nature of the position and the need to avoid conflicts of interest, cozy relationships with suppliers and contractors, and other undesirable practices. Since September 2020, the present members of the Board have been in place, with the Chairperson also holding a senior position at the Ministry of Finance responsible for monitoring the execution of contracts for infrastructure development works. The Minister of Public Infrastructure had stated that his appointment was a temporary one, clearly indicating the undesirability of the person holding two full-time positions at the same time.

When the Procurement Act was promulgated, the assumption was that a politically neutral Public Service existed at the time and would continue to exist. In the circumstances, it was appropriate for public servants to be involved in a very significant way in the adjudication of the award of contracts, with some input from the private sector in the case of the NPTAB. Since 1968, the Public Service is no longer viewed as politically independent. As a result, the tendency is for members of the various tender boards to be appointed based on political considerations, and for the award of contracts to be skewed in favour of those suppliers and suppliers who are supportive and/or closely associated with the ruling party. These and other undesirable practices in turn lead to significant breaches in the Procurement Act, defective work performed, cost and time overruns, overpayments to suppliers and contractors, the absence of good value for money, and indeed corruption and mismanagement of public resources. In all of this, it is the taxpayer that has to foot the bill.

To be continued –