President Irfaan Ali yesterday played up his government’s impact on private sector development saying that the increase in investments from that sector over the four years he has been in office is testament to the government’s private sector focus.

The billions invested into the sector, he said, has shown rewards and his PPP/C’s manifesto plans of creating 50,000 jobs, has been already achieved, in this fastest growing economy in the region.

“And as you know, we have various comparative advantages in the region. We are the fastest growing economy. We have the ideal location to access global markets. We are a resource rich country. We have fiscal incentives for investment. We have multi-sector opportunities. We have a diverse portfolio of business opportunities. We are a very private sector focused government,” Ali said in an over 20 minutes live video he posted on his Facebook page.

Examining work done over his tenure, especially in the private sector, he noted that jobs and investment are critical for the expansion not only for the private sector but for an overall healthy and sustainable economy.

Examining work done over his tenure, especially in the private sector, he noted that jobs and investment are critical for the expansion not only for the private sector but for an overall healthy and sustainable economy.

“Government’s policies, programmes and investment must lead to economic expansion, must lead to confidence in the economy,” the President said as he examined, according to his analyses, the impacts of his government’s policies and programmes in the last four years.

“We pride ourselves on developing strategies that carry very low operational costs…, ” he said, comparing his first term in office to that of the APNU+AFC which lost the 2020 General Elections after one term following a no-confidence fall.

Ali said that one of the best indicators in terms of confidence of the economy is how the private sector and investors perceive the economy and the level of comfort and confidence people have in government and government policies.

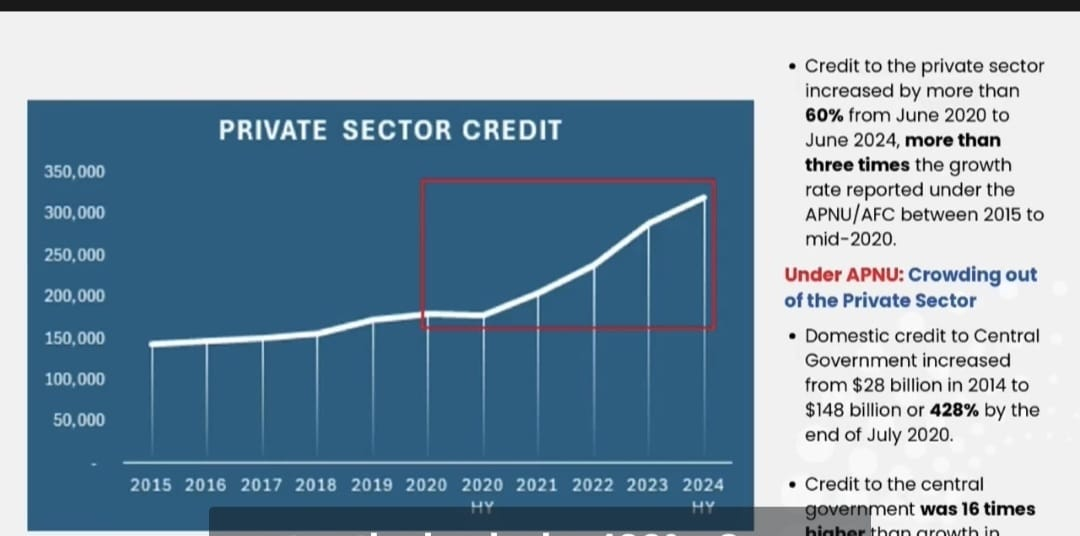

While discussing data on a graph, he said the number showed that private sector credit under the APNU+AFC was low and the reason for the sector expressing very low confidence in the policies of the past government.

“That is why you will see a very flat period, very flat private sector growth, very flat private sector credit, very flat investment or credit to the private sector. Unlike a rectangular block you see in red that demonstrates to you the period of the People’s Progressive Party Civic government. You can see every year continual expansion in private sector credit, confidence in the economy, confidence to invest. And as a result, credit to the private sector increased by more than 60% from June 2020 to June 2024. From the time we came into government, to mid of 2024, private sector credit, or credit to the private sector, grew by 60% that is more than three times the growth in the entire APNU+AFC period,” he contended.

“Unlike the private sector growth, what took place under the APNU+AFC – a crowding out of the private sector – because what they were doing, they were just borrowing and borrowing and borrowing with no end of improving productivity or increasing opportunities for the private sector of the population… Domestic credit to the central government, that is, loans to the central government from the local banking institutions, increased from $28 billion in 2014 to $148 billion. So government increased their borrowing from the private institution, the private sector, the banks, by 428%. Can you imagine that? And this was what collapsed our economy in the past,” he added.

He reasoned that the borrowing without a plan to create wealth for citizens, some 16 times higher than that of the private sector, played a factor in the private sector not wanting to support that government.

“Imagine this, that the credit from the commercial banks to the central government was 16 times higher than credit to the private sector! That is why we had the private sector regressing… persons losing their jobs, loss of productivity, loss of competitiveness and the private sector went into complete chaos. Many of the companies went into bankruptcy,” he charged.

He boasted of a broad-based economic expansion plan that his government invested in from 2020 that saw a complete turnaround.

“For the private sector to invest… they have to have confidence in the government policies. They have to see sustainability. They have to see profitability. And as a result of these investments, tens of thousands of jobs in every sector have been created,” Ali said.

Looking at investment in agriculture, he said that when he took office in 2020 to current day, “private investment in agriculture went from $12.5 billion to $24.6 billion, an increase of 97%. That is the investment we are making in DNI, the investment we are making in farm-to-market access roads, the support to our farmers, the confidence that has been instilled back in the agricultural sector.”

In manufacturing, he said, private sector investment “went from $15.1 billion to $22. 3 billion, an increase of 47%.

“The incentivizing of the manufacturing sector, creating wealth, creating new industries, expanding existing industries, creating jobs, a 47% increase in private sector credit from the time we came into government to mid-2024.”

In the area of construction, the President said, there has been a 93% increase throughout the country by the private sector.

“Private sector investment in construction went from $0.6 billion to $24.4 billion by the mid of 2024… A 93% increase in private sector investment in construction. That is the confidence people have in building their own facilities, their own commercial buildings, their own office complexes, their own apartment buildings, their own homes…,” Ali stressed.

Even mining, he said, saw private sector credit investment going from $4.2 billion to $6.9 billion “An increase of 65% from the time we came with the government to now,” he stated. “This is the positive reaction. This is the confidence that the private sector investors have in the economy.”

Real estate mortgages increased from $88.7 billion when he came into office, to $140.2 billion an increase of 58%, according to the President and “that is confidence, that is what we brought back to this country… expansion of every sector, expansion of the economy.”

Looking at foreign direct investment (FDI), he said, “the attractiveness of our country as an investment destination between 2021 and 2023 saw FDI amounting to $16.1 billion, more than three times the level reported under APNU+AFC government for the entire [five-year] period.”

“Between 2021 and 2023, Guyana reported the highest FDI inflows in the Caribbean, according to the United Nations Economic Commission for Latin America and the Caribbean. Further, in 2023 there were inflows of US$7.198 billion, a 64% increase over 2022, positioning Guyana as the sixth largest inward FDI recipient country in Latin America and the Caribbean. Imagine that, the six largest. And who are we competing with? We have Brazil, Mexico, Argentina, Chile and Colombia. Those huge economies ahead of us, and we were able to attract more FDI than all the other countries. This is the substance of our governance when we came to the people in 2020,” he said.