Dear Editor,

The U.S. Foreign Tax Credit (FTC) is designed to prevent double taxation by allowing individuals and corporations to offset taxes paid to foreign governments against their U.S. tax obligations. However, there is compelling evidence that ExxonMobil and its affiliates obtain tax certificates issued by the Guyana Revenue Authority (GRA) without actually paying taxes in Guyana. The Oil and Gas Governance Network Guyana (OGGN) is concerned that these tax certificates may be used to claim illegitimate FTCs from the U.S. Internal Revenue Service (IRS), potentially depriving the U.S. Treasury of billions of dollars in tax revenues.

Guyana’s Taxation Arrangement with ExxonMobil

Under the 2016 Petroleum Agreement (PA) between the Government of Guyana and ExxonMobil Guyana Limited (EMGL), a subsidiary of ExxonMobil, Hess Corporation, and China National Offshore Oil Company (CNOOC), the government agreed to pay the oil companies’ taxes from Guyana’s share of oil revenue. Specifically:

Article 15.4 of the PA states that the Minister responsible for Petroleum will pay taxes on behalf of the Contractor (ExxonMobil and affiliates) and that this sum will be considered the Contractor’s income.

Article 15.5 specifies that the Minister will ensure that the GRA issues tax receipts and certificates confirming these payments.

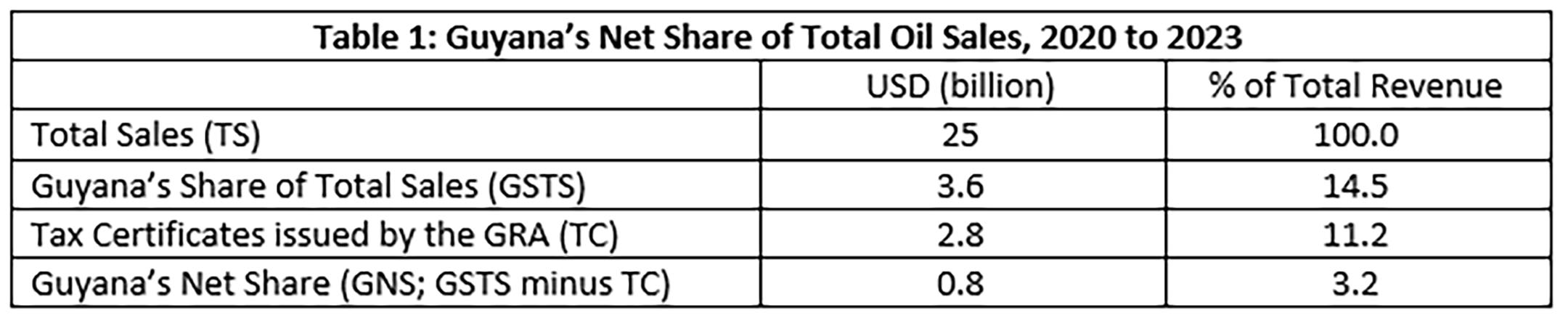

As a result, rather than paying corporate income taxes directly, ExxonMobil and its affiliates, benefit from Guyana’s tax payments, amounting to Tax Certificates issued to the value of approximately USD 2.8 billion from 2020 to 2023 (Table 1; adapted from Ref. 3, 1 USD = 208.5 GYD). This practice means that 78% of Guyana’s total oil revenues (USD 3.6 billion) were earmarked to cover taxes on behalf of foreign corporations. This leaves Guyana’s net share of total oil sales in real terms at a meagre USD 0.8 billion (3.2% of Total Oil Revenue).

Legal and Financial Concerns

The central issue is whether ExxonMobil and its affiliates use these tax certificates to claim U.S. FTCs without actually paying foreign taxes. If so, this practice could violate U.S. tax laws, particularly:

26 U.S. Code §901: Credit for taxes paid to foreign countries – This provision requires that foreign taxes be “actually paid or accrued” to qualify for U.S. tax credits.

IRS regulations on economic substance (26 U.S. Code §701(o)) – Transactions must have economic substance beyond tax benefits.

Given that ExxonMobil and its affiliates do not in effect remit taxes to the Guyanese government, their ability to claim FTCs under these statutes is highly questionable.

It could be argued that the tax arrangement is legal under Guyana’s 2016 PA and that it is standard practice in the oil and gas industry. However, the IRS has strict guidelines requiring that tax payments be actual and compulsory, rather than merely recorded in agreements. Furthermore, there are no public records confirming that the Government of Guyana has remitted these tax payments to the GRA, making the tax certificates issued to ExxonMobil and its affiliates potentially misleading.

Conclusions and recommendations

The tax arrangement for ExxonMobil and its affiliates as outlined in the 2016 PSA is an outlier; other companies in Guyana do not receive similar benefits. Given these facts, OGGN, a registered 501(c)(3) non-profit organization in New York, United States, urges the US authorities to:

Initiate a formal investigation into ExxonMobil’s use of tax certificates issued under Guyana’s 2016 PSA.

Request IRS review of whether ExxonMobil’s claimed FTCs comply with U.S. tax laws.

Hold hearings or introduce legislation to prevent similar arrangements from depriving the U.S. Treasury of revenue in the future.

The potential loss to U.S. taxpayers over the 40-year duration of the PSA could amount to tens of billions of dollars. Ensuring tax fairness is critical to upholding transparency and corporate accountability.

Yours faithfully,

Andre Brandli

Kenrick Hunte

Alfred Bhulai

Janette Bulkan

Darshanand Khusial

Joe Persaud

for the

Oil & Gas Governance Network Guyana (OGGN; www.oggn.org)