Introduction

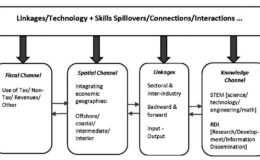

My aim has been in recent columns to lay out carefully the economic rationale in support of the proposition that, if Guyana’s coming oil and gas extraction industry is to play a transformative role in its economic development, then the dynamic integration of whatever economic benefits are derived from the industry into other economic sectors is essential.

Introduction

In last week’s discussion of Guyana’s proposed local content requirements (LCRs) policy for its coming oil and gas extraction industry, I had introduced three key concepts, which require further elaboration.

Introduction

In my New Year’s Day column this year I had indicated there are three policy priorities which seemingly guide government’s preparations for the development of its impending oil and gas-based extraction sector.

Introduction

At the conclusion of last week’s column, I had indicated the intention to wrap up in today’s column my discussion concerning the institutional architecture and governance in preparation for Guyana’s coming gas and oil industry.

Introduction

Last week’s column advanced the view that Guyana’s membership of the Extractive Industries Transparency Initiative (EITI) is a crucial plank in the institutional governance architecture being designed for managing its impending oil and gas extraction industry.

Introduction

Today’s article brings to a conclusion the three-part series of columns that have been reviewing Guyana’s proposed membership of the Extractive Industries Transparency Initiative (EITI).

Today’s column continues the discussion of Guyana’s long declared policy option of seeking membership of the Extractive Industries Transparency Initiative (EITI) as a cornerstone of its approach to governance of the fast approaching time of oil and gas production and export.

Introduction

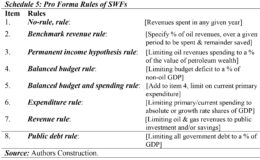

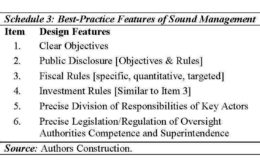

Last Sunday’s column completed my presentation of ten lessons which I have argued the Guyanese authorities can profitably learn from a studied appraisal of worldwide experiences with oil-based sovereign wealth funds (SWFs) over the past six decades.

This week I propose to conclude for the time being, my portrayal of lessons that can be learnt from worldwide experiences with SWFs over the past six decades.

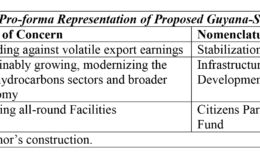

Following last week’s discussion of Sovereign Wealth Funds (SWF) as a mechanism for avoiding and/or controlling the triad of crises typically associated with booms in oil and gas export revenues, I describe below the Government of Guyana’s declared intention with regards to its own SWF.

Introduction

In last week’s column I had advanced the opinion that there were three policy priorities seemingly driving government’s approach to the development of the oil and gas sector.

Introduction

Under Section 31 of the Petroleum Act, official notification was given last month, by ExxonMobil and its partners (Nexen Energy and Hess Corporation), to the Government of Guyana confirming the find (discovery) of commercial quantities of oil and gas in the Stabroek Block.

Introduction

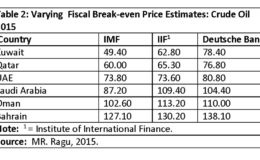

In this ongoing series discussion of Guyana’s prospect during its coming time of oil and gas production and export (that is circa 2025), I had introduced in last week’s column the notion of the break-even price.