Introduction

Last week’s column addressed two of five topics singled out earlier for comment in order to highlight their significance from an economic perspective; namely 1) Government take/developmental benefits/economic profit; and 2) accounting for costs.

Introduction

Today’s column along with the next portrays selected aspects of my recent discussion of the fiscal regime in Guyana’s 2016 Production Sharing Agreement (PSA), from the perspective of basic economic principles.

Introduction

Today’s column expands on last week’s discussion of the government take, as it relates to Guyana’s 2016, Production Sharing Agreement (PSA).

Rational incentive

Based on the economics Nobel Prize winning theory of “incomplete markets”, my previous column posited that, the Parties to Guyana’s 2016 PSA have a rational incentive to re-negotiate the contract, if underlying conditions of the country’s petroleum sector drastically change.

Introduction

Last week’s column, sought to reinforce the critical importance of two features of the fiscal regime embedded in Guyana’s 2016 Production Sharing Agreement (PSA).

Introduction

The observation was made much earlier in the series and repeated for emphasis last week: Guyana’s present petroleum fiscal regime encompasses both 1) its basic constitutional, economic, financial, and accounting legislation, as well as 2) the specific terms and conditions enshrined in the 2016 Production Sharing Agreement (PSA).

Introduction

As far as I can determine, a standard formulation of Guyana’s fiscal regime for its petroleum sector would describe this as ‘The Terms and Conditions that are applied to both the Owner (State) and Contractor (Exxon and its partners) for conducting their business within an integrated framework; from exploration activities, right through the production chain (upstream to downstream), as well as trading’.

Introduction

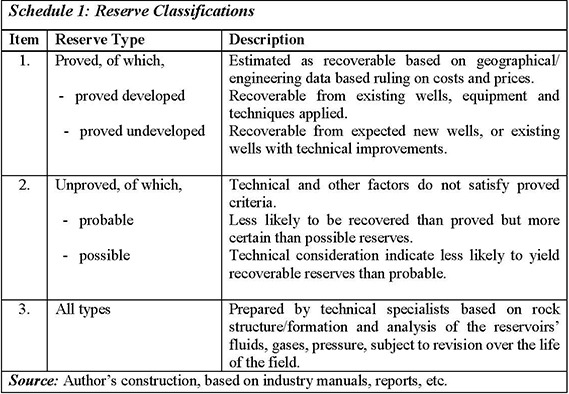

Last week’s column established that the mechanism of ring-fencing for determining recoverable cost is not, unambiguously, to Guyana’s benefit.

Introduction

In the absence of the explicit ring-fencing of costs, the Guyana 2016 Production Sharing Agreement (2016) has provoked unqualified and perhaps even one-sided condemnation.

Introduction

Following on several readers’ queries, perhaps I should indicate that I am by no means singular when treating cost recovery as a central component of the fiscal regime of petroleum producing countries.

Introduction: Catalogue

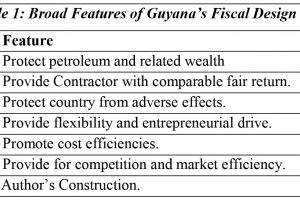

The catalogue of desirable features energy economists promote for effective PSAs are that 1) ownership of the petroleum wealth should remain within the domain of the country in which it is discovered; 2) the State/Principal should maintain managerial control of this wealth, but 3) the Contractor/Agent (in Guyana’s case Exxon and its Partners) should maintain operational control of contract-assigned petroleum activities.

Introduction

Last Sunday’s column introduced a simple basic ‘Setting’ (as energy analysts label it) or more commonly, analytical framework drawn from energy economics, under which the Guyana 2016 Production Sharing Agreement (PSA) will be appraised in coming columns.

Introduction

From their very inception, oil agreements/contracts have embodied dynamic processes between states, as sovereign owners or guarantors/regulators of rights to a country’s petroleum wealth, and individuals/oil-companies that contract to develop this wealth.

Introduction

Production sharing agreements or contracts (PSAs), have been, from the time of their earliest introduction to the oil and gas sector, subjected to in-depth critical analyses and/or evaluations from economic, legal, and institutional perspectives.

Introduction

At the time of writing this column media reports indicate that a signature bonus of US$18 million has been paid to the Government of Guyana (GoG) by Exxon and its partners.