The future of sugar in Guyana

Introduction The process of consolidating and centralizing capital and other productive assets in Guyana’s sugar industry reached its apogee with the establishment of GuySuCo in 1976.

Introduction The process of consolidating and centralizing capital and other productive assets in Guyana’s sugar industry reached its apogee with the establishment of GuySuCo in 1976.

In last Sunday’s column I sought to portray what I termed as the fundamental economic illogic or contradiction which underlines GuySuCo operations.

While, as the saying goes, there is very little to be gained from crying over spilt milk, the fact of the matter is that the large income transfers made by the EU to Guyana (averaging over 8 per cent of Guyana’s GDP at its peak in the 1990s) when the Sugar Protocol was in force until 2006, have left few positive economic legacies.

Shifting the goalpost In most cases of deliberate political and intellectual deception or expediency, persons and organisations would, as the saying goes, seek to shift the goalpost during the debate, in order to defeat the opposing point of view.

Introduction In an effort to encourage ACP countries to embrace the Sugar Protocol (SP) in the mid-1970s, European officials were at pains to stress that, when fixing the annual price for sugar, account would be taken to ensure a “reasonable rate of return for a reasonably efficient sugar enterprise, over the long run.”

Introduction The gravamen of last week’s discussion of the technological developments pursued by Booker Tate and GuySuCo in the area of cane cultivation is that these were expected to proceed hand-in-hand with technological improvements in the factories.

Last week’s column carried a schedule listing the key specifications for the new Skeldon factory.

Introduction The columns I have written so far on the sugar industry, starting on May 29, 2011 are intended to conclude with a broad appraisal of its prospects and suggestions for the way forward.

As planned, last week I completed the examination of GuySuCo’s key performance indicators.

Necessary questions Today’s column begins with my response to two questions, which several readers have raised with me, privately.

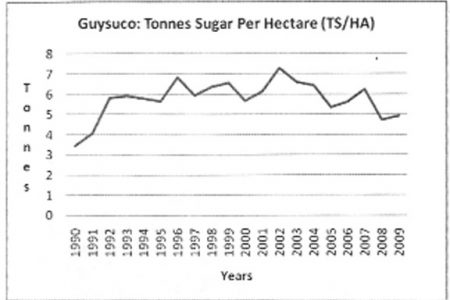

Introduction In last week’s column I had presented time series information pertaining to GuySuCo’s factory performance for the two decades of the 1990s and 2000s.

In last week’s column I continued the discussion of GuySuCo’s performance indicators and also dealt with several other items related to the pattern of yields of sugar cane on GuySuCo’s estates.

In last week’s column I had indicated that GuySuCo’s Report for 2009 stated that there was no payment of dividends for that year, as in many previous years.

Introduction In last week’s column on the sugar industry I had ended with the presentation of a table on GuySuCo’s expenditure on two key items, namely, “employment costs” and “materials and services” for the years, 1990, 1995 and the decade of the 2000s.

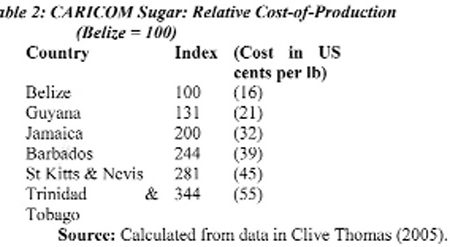

Introduction In last week’s column I had indicated that Guyana’s sugar production, similar to the situation in the rest of Caricom, has been so high cost that it could not survive commercially without the special external marketing arrangements which the region had negotiated under the Commonwealth Sugar Agreement (CSA) and its successor the European Commission – African, Caribbean, Pacific (EC-ACP) Sugar Protocol.

Introduction The detailed figures presented in last Sunday’s column on Guyana’s sugar production for the years 1961 to 2010 (on the basis of 3-year averages) and the accompanying chart reveal three notable features.

Per unit cost/price of gold As we saw last week, despite Guyana’s long historical association with gold discovery and exploration it is ironic to name as an upside potential/achievement that is facing the economy over the near-to-medium term, the prospects of large-scale gold production coming on-stream by 2014.

In the present series of columns I had introduced oil and natural gas exploration and development as the first upside potential/achievement for consideration.

Features This week I start a discussion on the upside potential/opportunities facing the Guyana economy.

This week I shall consider the remainder of the downside risks facing the economy over the short-to-medium term.

The ePaper edition, on the Web & in stores for Android, iPhone & iPad.

Included free with your web subscription. Learn more.